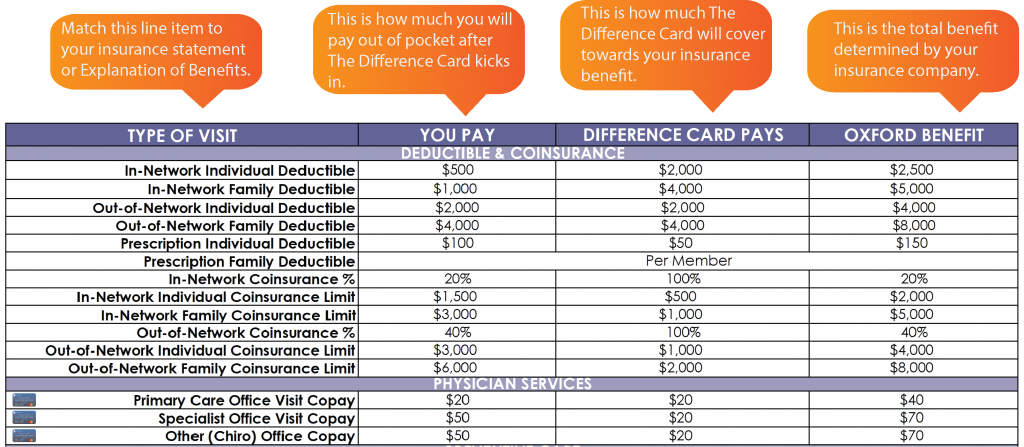

Helpful Tips for Reading Your Difference Card Summary of Benefits Charts

When you enroll in The Difference Card, you will receive your Summary of Benefits, a document that looks very similar to this one.

This document breaks down your benefits into how much you pay and how much The Difference Card will pay.

On the right, you will see the total benefit determined by your insurance. In the middle column, this is how much The Difference Card will cover towards your insurance benefit. Unless stated otherwise, you must meet your portion of deductible and coinsurance expenses before The Difference Card will begin to reimburse you.

GLOSSARY OF HEALTH INSURANCE TERMS

Coinsurance: A form of cost sharing. A percent you pay after you have met your deductible.

Copay: A fixed amount that you pay for a covered health care service.

Deductible: The amount you pay for covered health care services before your insurance plan starts to pay.

Dependent Care Account: A DCA is a type of Flexible Spending Account where the pre-taxed funds are set aside to be used for childcare expenses for children age 13 and under. It can also be used to pay for the care of adult dependents.

Difference Card: An employer funded benefit that goes hand-in-hand with your medical insurance provider. It works by paying portions of copays and deductibles you may incur through your insurance plan.

Explanation of Benefits: An EOB is generated by your insurance provider after a medical visit. An EOB explains what was paid by your health insurance and the payment you owe to the medical provider.

Flexible Spending Account: An FSA is an employer-sponsored benefit that allows you to set aside pre-tax dollars into an account to be used for eligible medical expenses.

Health Savings Account: An HSA is a type of savings account for people with High Deductible Health Plans (HDHP) that lets you set aside money on a pre-tax basis to pay for qualified medical expenses.

In-Network: This means that your doctor or facility providing your care has negotiated a contracted rate with your health insurance company.

Out-of-Network: This means that the doctor or facility providing your care does not have a contract with your health insurance company.

Out-of-Pocket Maximum: The absolute most you would have to spend for in-network costs throughout the year. This includes your copays, your deductible, and your coinsurance.