Who Is Eligible for an Individual Coverage HRA?

Table of Contents

In 2023, about 60% of people under 65 years old had employer-sponsored health insurance (ESI). However, even though ESI has been the largest source of health benefits for younger Americans, there is still uneven coverage that employers and brokers need to address. Through an individual coverage health reimbursement arrangement (ICHRA), employers can help provide more appropriate healthcare benefits to their employees without sacrificing the company's budget.

There are a few ICHRA eligibility rules for employers and employees. If you're a broker looking to pitch ICHRA to your clients or an employer seeking to understand if you can offer the account, this article details everything you need to know.

What Is an ICHRA?

An ICHRA is an employer-funded health benefit that works as an alternative to a traditional health insurance plan. With an ICHRA, employees choose their individual health plans and submit proof of expenses for reimbursement. Qualified healthcare expenses include out-of-pocket and monthly payments. ICHRA reimbursements are also tax-free, benefiting both employers and employees.

Keep in mind that an ICHRA is not a health insurance plan. While a traditional group plan involves employers purchasing health insurance for their employees, an ICHRA provides more flexibility regarding costs and coverage.

ICHRA Contribution Limits

Employers can decide how much they will contribute annually. There are no minimum or maximum requirements. That said, if the ICHRA is considered "affordable," which is impacted by the employer's contributions, then the employee will not be eligible for the premium tax credit. Premium tax credits can help individuals lower their monthly premiums in the Marketplace, which is why employees need to decide which type of benefit will give them more savings.

In 2025, an ICHRA is considered affordable if the monthly premium of the most affordable Silver plan in the self-only Marketplace coverage, subtracted by the HRA contribution, is equal to or less than 9.02% of 1/12 of the employee's household income. In this case, employees cannot combine an ICHRA with a premium tax credit.

What Companies Can Offer ICHRA?

Businesses of all sizes can offer an ICHRA, provided they have at least one employee who is not self-employed or the spouse of the business owner. This employee needs to be a W-2 employee, which is a formally recognized individual working with a company in the U.S. A self-employed person does not qualify for an HRA. This also means that the following individuals do not qualify:

- Sole-proprietors

- Partners in a partnership

- S-corporation owners, spouses, and dependents owning more than 2% of the business

C corporation owners can opt for an ICHRA because C corporations are considered legal entities distinct from the owners. This ICHRA eligibility also includes the owner's family members. Additionally, if a company has at least 50 full-time employees, also known as an applicable large employer (ALE), they are subject to the employer mandate. ICHRA can help satisfy this mandate, as long as the employer offers an affordable HRA.

According to the HRA Council, ICHRA adoption has increased 34% among applicable large employers. Additionally, 83% of companies that offer an ICHRA or a qualified small employer health reimbursement arrangement (QSEHRA) — which is an HRA offered by smaller employers — in 2025 previously did not offer health coverage. Around 17% have transitioned from a traditional group health plan. This shows that there's a growing trend and that the account is helpful in bridging the gap in health benefits needed by employees.

Ideal Businesses for ICHRA

Although an ICHRA is not limited to specific companies, some businesses may benefit more from it than others:

- New businesses: Traditional group health plans may not always be affordable for all businesses, especially for those just starting out. Some employers may also struggle to meet the participation requirements with a small number of employees. With an ICHRA, these companies can still offer healthcare benefits without having to worry about the budget or size requirements.

- Nonprofit organizations: Nonprofits typically work on tight budgets, which means a traditional health plan might not always be feasible. However, with an ICHRA's flexibility, they can still offer healthcare benefits without breaking the bank.

- Construction firms: The construction industry can be physically taxing, making health benefits essential. What's more, projects can be delayed if part of their workforce gets sick. An ICHRA can help companies provide the necessary care their team members might need to keep them safe and keep the projects going.

Employer Responsibilities

Employers will not have a responsibility for the chosen health insurance of the employee as long as:

- The employee purchases the health insurance voluntarily.

- The employer did not endorse a particular insurance carrier or coverage.

- The employer did not receive any cash or gifts regarding the employee's chosen insurance.

- Each employee is informed every year that the individual health insurance is not subject to the federal law on employer-sponsored health coverage, also known as the Employee Retirement Income Security Act (ERISA).

Employers can choose to offer an ICHRA at any time, but employees should also be given the chance to decline. If an employee opts in, employers should provide a letter to help them understand the coverage terms. The letter should inform employees that they should enroll in individual market health insurance or Medicare. Employers should send this letter at least 90 days before the start of the HRA's plan year.

New employees should receive the letter on the first day their ICHRA starts. The letter should include the following information:

- If the ICHRA covers the employee's household members

- How much the employer is willing to reimburse

- The start and end dates of the ICHRA

- The rules for enrollment in other health coverage and how an HRA impacts this coverage

The Department of Labor has a model letter employers can follow. Employees can enroll for qualified health insurance through the Marketplace or through a private plan no later than the start date of the ICHRA. Employers can specify that the open enrollment period is usually November 1 to January 15. However, the specific dates can depend on each state. Outside of these dates, employees can only opt for a plan if they qualify for special enrollment, usually if they experience a significant life event. For instance, they could be newly hired or have just gotten married.

How Does ICHRA Work for Employees?

Employees will also need to follow the ICHRA rules to ensure their claims won't be denied. An employee's chosen individual health insurance coverage can't be short-term or have a limited duration, and it cannot solely cover dental, vision, or similar benefits.

Additionally, employers should offer an ICHRA to all employees under the same class. For instance, if you offer one full-time employee an ICHRA, all other full-time employees should also be able to have one. The classes of employees include:

- Full-time employees

- Part-time employees

- Seasonal employees

- Salaried workers

- Nonsalaried workers

- Employees in the same geographic location

- Employees covered by a collective bargaining agreement

- Temporary employees

- Nonresident aliens

Note that employers cannot make up their own classes. Additionally, while the same ICHRA terms should apply to all employees within a specific class, the offered amounts can be increased for older employees and employees with more dependents. As a special rule, employers can offer new hires an ICHRA even if existing employees have a traditional group health plan.

That said, employers cannot combine an ICHRA with a traditional group health plan. If employers decide to offer an ICHRA with a specific class and a traditional health plan with another class, certain size requirements apply to the classes getting an ICHRA offer:

- Less than 100 employees: At least 10 employees get an ICHRA offer.

- 100-200 employees: At least 10% of the total number of employees get an ICHRA offer.

- 200+ employees: At least 20 employees get an ICHRA offer.

These size requirements don't apply if an employer doesn't offer a traditional group health plan.

ICHRA Health Insurance Requirements

Employees who want to opt for an ICHRA need to enroll in either individual health insurance coverage or a qualified Medicare program.

Individual Health Insurance Coverage

Individual health insurance coverage can be for individuals or families, as long as it is not purchased through an employer or through a government-run program, like Medicaid, Medicare, or CHIP. It's available through the Marketplace — 31 states currently use HealthCare.gov as their healthcare marketplace, while DC and 19 states run their own platforms. State-based exchanges include:

| State | State-Based Exchange |

|---|---|

| California | Covered California |

| Colorado | Connect for Health Colorado |

| Connecticut | Access Health CT |

| District of Columbia | DC Health Link |

| Georgia | Georgia Access |

| Idaho | Your Health Idaho |

| Kentucky | Kynect |

| Maine | CoverME |

| Maryland | Maryland Health Connection |

| Massachusetts | Massachusetts Health Connector |

| Minnesota | MNsure |

| Nevada | Nevada Health Link |

| New Jersey | Get Covered New Jersey |

| New Mexico | BeWellNM |

| New York | New York State of Health |

| Pennsylvania | Pennie |

| Rhode Island | HealthSource RI |

| Vermont | Vermont Health Connect |

| Virginia | Virginia’s Insurance Marketplace |

| Washington | Washington Health Plan Finder |

Employees can also purchase individual health insurance through an off-exchange (outside the Marketplace) and through private plan providers. This is unless a company resides in the District of Columbia, in which case, employees are required to enroll in health insurance through the Marketplace.

Wherever employees purchase their insurance, they need to make sure the insurance offers Minimum Essential Coverage (MEC). This type of insurance meets the requirements of the Affordable Care Act (ACA). Agents and brokers can help employers and employees alike identify whether a plan is qualified. It's important to note that, without a qualifying life event, employees may not be able to enroll in them outside of special enrollment periods.

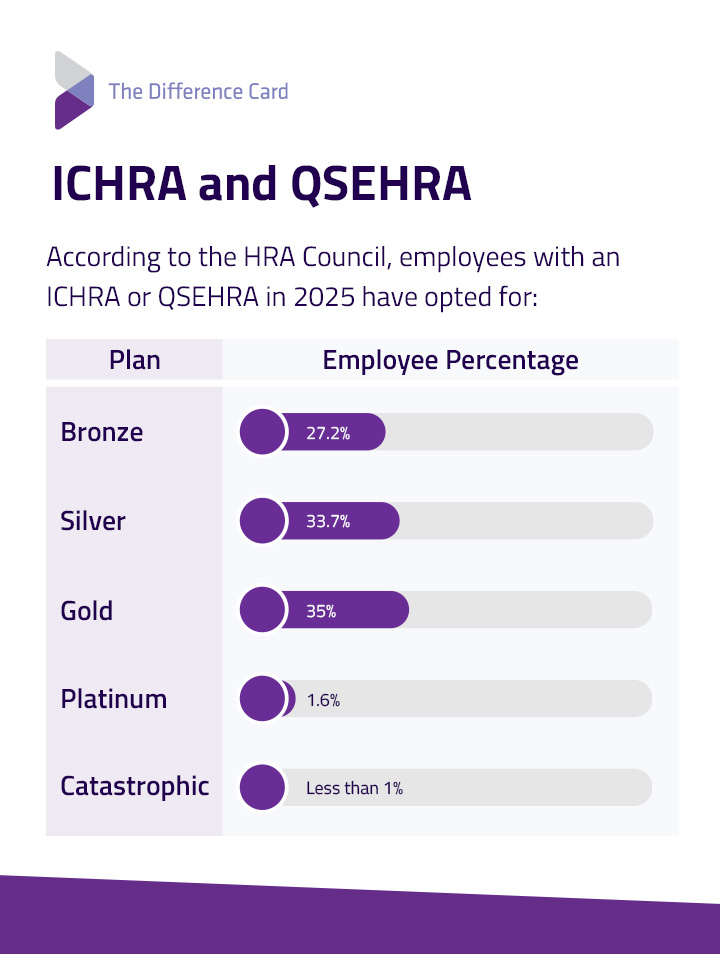

According to the HRA Council, employees with an ICHRA or QSEHRA in 2025 have opted for:

| Plan | Employee Percentage |

|---|---|

| Bronze | 27.2% |

| Silver | 33.7% |

| Gold | 35% |

| Platinum | 1.6% |

| Catastrophic | Less than 1% |

Medicare

Medicare is a federal health insurance program for people 65 years old and older, as well as people with certain disabilities. This program has four parts, but only parts A, B, and C can work with ICHRA, meaning employers must disclose to their employees that part D is not included. This is because an ICHRA doesn't directly cover prescription drugs. Employees would need Parts A and B together, which pertain to hospital and medical insurance, while Part C, which is Medicare Advantage, can be a stand-alone. In 2025, about 2% of employees enrolled in ICHRA through Medicare.

The company should submit the Medicare coverage notice for employees to the Centers for Medicare & Medicaid Services.

Benefits and Drawbacks of an ICHRA

Whether an ICHRA is good for employees and employers depends on their specific circumstances. Consider the following benefits:

- Tax advantages: Reimbursements are free of income and payroll taxes, benefiting both employers and employees. Because employees can select the most suitable healthcare plan, it's easier to avoid tax penalties for not having health insurance.

- Increased employee options: Health insurance coverage shouldn't be a one-size-fits-all solution. Employees can choose from the Marketplace options or from an insurance provider of their choice. Additionally, if an employee already has an existing policy, they won't need to worry about having to change it.

- Flexible contributions: Because employers get to decide how much to contribute, it's easier to budget for the accounts, regardless of whether a company is big or small.

- No participation requirements: Unless a company offers ICHRA and a traditional group health plan, the company doesn't have to worry about participation requirements. Traditional plans typically require a percentage of employees to enroll in their healthcare benefits.

- Simplified administration: An ICHRA's administration can be simpler compared to managing group plans. Although companies will have to track reimbursements, ensure compliance, and review coverages, third parties like brokers and administrators can help make implementation easier.

Despite the benefits, the following drawbacks can also influence a company's decision:

- Compliance requirements: Compliance requirements, such as affordability requirements, notice requirements, and limitations with traditional group health plans, can sound like extra work, especially for smaller businesses. Failing to comply may also cost the employer penalties.

- Coverage limitations: Employers must consider the class types and healthcare coverage requirements. Employees who choose an ICHRA should also consider the loss of premium tax credits.

- Additional employee effort: Because employees would need to look for qualified healthcare insurance coverage, this would require extra work on their part, compared to if the company had purchased the health insurance itself. Employees also need to keep receipts or proof of the covered medical expenses to get reimbursed.

Make Healthcare More Accessible With The Difference Card

Employers can work with brokers and ICHRA providers to offer individual coverage HRA accounts to employees. Professionals can make compliance easier. If you're a broker, The Difference Card can help your clients build the most cost-effective healthcare plan without sacrificing coverage. If you're an employer, you can also directly work with us to improve the healthcare benefits your employees receive.

Since 2001, we have been providing health insurance savings to our clients, with an average net savings of 18%. We can help you customize a plan according to your budget and workforce. What's more, we offer a dedicated account manager for each client, ensuring reliable and exceptional customer service. If you're looking to offer an ICHRA, request a proposal today to get started.