How Section 105 Medical Reimbursement Plans Save on Taxes

Table of Contents

In the U.S., healthcare costs are rising faster than inflation, with health spending reaching $4.9 trillion in 2022 alone. Small business owners experience climbing premiums, while employees struggle with out-of-pocket costs. Failing to navigate complex tax laws correctly can lead to missing significant savings.

The Internal Revenue Code's (IRC) Section 105 offers a good solution. Different plan structures can take advantage of the section, making it easier for your business to design a plan that suits your needs. The section paves the way for a cost-effective health benefit without sacrificing coverage. Understanding what it is, how it works, and how it differs from other plans should help you make informed benefits decisions.

Learn More About MERPs

What Is a Section 105 Medical Reimbursement Plan?

A Section 105 medical reimbursement plan pertains to employer-funded arrangements compliant with IRC's Section 105. These plans enable you to reimburse employees' health insurance premiums and medical expenses tax-free. The plans don't function as a traditional insurance policy, but rather as a method for funding healthcare expenses.

These plans reduce your employees' financial burden, while your business gains tax deductions. They come in different plan structures, designed to benefit specific business situations and employee needs. Despite the different plan designs, all Section 105 arrangements come with the same tax-advantaged rules. Whether you run a small startup or an established company, understanding how to set one up can unlock significant savings.

How the Reimbursement Process Works

Here's how to set up a Section 105 plan:

- The employer establishes the plan rules: As an employer, you define the qualified expenses, eligibility rules, and reimbursement limits. You should also determine the monthly or annual contribution limits and other plan parameters based on your budget and employee needs.

- An employee submits a proof of expense: After incurring a medical expense, an employee must provide you with the proof of expense, which could be an invoice, receipt, or explanation of benefits statement. You must then verify if the expense meets the plan's reimbursement criteria.

- The employer reimburses the employee: After approval, you reimburse the employee with tax-free funds.

Note that employers maintain fund ownership — if an employee leaves the company, unused funds revert to you. This structure gives you greater control over healthcare spending while still providing valuable benefits to the team.

A third-party administrator makes this process seamless by handling the documentation review, compliance checks, and payment processing. It removes the administrative burden from your internal team while ensuring reimbursement accuracy.

Section 105 Plan Tax Advantages

As long as your plan remains compliant, all reimbursements are fully deductible as a business expense. This tax-deductible nature enables you to lower your taxable income, impacting your bottom line. The Internal Revenue Service (IRS) recognizes these reimbursements as legitimate business expenses when the plan follows federal guidelines.

Tax savings from a Section 105 plan also extend to employees. Unlike a salary bonus or wage increase, reimbursements are free from federal income tax, state income tax, and Federal Insurance Contributions Act (FICA) taxes. For someone with regular medical needs, these tax advantages can make reimbursements more helpful than increasing their salary. For instance, when you give an employee a $1,000 raise, they might only see $700 after taxes. That same $1,000 delivered through a Section 105 plan provides the full $1,000 in value.

Also, a Section 105 plan can work alongside a health savings account (HSA), which comes with its own tax advantages. An HSA lets employees contribute pretax dollars for future medical expenses. Section 105 and HSA options complement each other, and many businesses use them together strategically.

Rules for Section 105 Plans

Section 105 plans must adhere to federal regulations to maintain their tax-advantaged status. The specific regulations that apply depend on your plan type and employer size. Apart from the IRS rules, plans may need to adhere to the Affordable Care Act, Employee and Retirement Income Security Act, Health Insurance Portability and Accountability Act (HIPAA), and other state and federal laws.

For instance, nondiscrimination rules prevent plans from favoring specific employees, such as highly compensated employees or company owners. Your plan must offer similar benefits to all eligible employees to maintain its tax-advantaged status. HIPAA compliance requires protecting employee health information and maintaining privacy standards when handling medical expense documentation.

Reimbursements should also be limited to qualifying medical expenses. Although you define the specific coverage, your covered expenses should be present from the IRS's comprehensive list of eligible healthcare costs. Your plan documentation is the foundation of compliance and should be available for IRS review. It must outline the eligibility criteria, covered expenses, reimbursement procedures, and administrative processes.

Section 105 Eligibility

Eligibility for Section 105 plans varies based on your business structure. Understanding these distinctions helps you determine whether you and your employees can participate:

- C-Corporation (C-Corp): Because C-Corps are fully separate legal entities from their owners, owner-employees can participate in the plan just like any other employee. This structure offers the most flexibility for owners who want to benefit from Section 105 tax advantages.

- S-Corporation (S-Corp): S-Corp owners face a crucial restriction outlined in the IRC. Shareholders who hold more than 2% of company stock cannot receive tax-free reimbursements from a Section 105 plan. The IRS treats 2% shareholders differently from other employees for tax purposes. Regular employees who don't meet this ownership threshold can participate without restriction.

- Sole proprietors and partnerships: Owners of these business entities are not considered employees under federal tax law. Hence, they cannot participate directly in a Section 105 plan. However, you may hire your spouse as a bona fide W-2 employee. When structured properly per IRS guidelines, this approach allows the plan to cover the entire family since the employed spouse qualifies for benefits.

The detailed regulations in Section 105 outline these distinctions clearly. Consulting with a qualified benefits administrator ensures your plan structure complies with eligibility requirements for your specific business type.

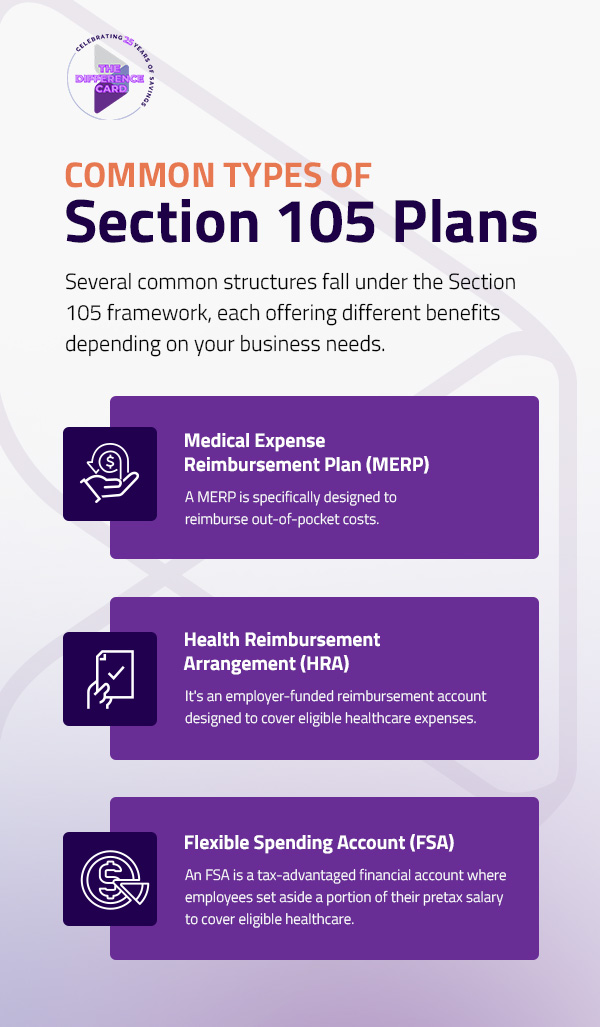

Common Types of Section 105 Plans

Several common structures fall under the Section 105 framework, each offering different benefits depending on your business needs. While no universal Section 105 plan template exists, understanding these standard arrangements helps you choose the right approach for your situation.

Medical Expense Reimbursement Plan (MERP)

A MERP is specifically designed to reimburse out-of-pocket costs like deductibles, copayments, and coinsurance. Many businesses pair a MERP with a high-deductible health plan (HDHP) to create an affordable benefits package. The employer offers a lower-premium HDHP to employees, then uses the MERP to cover the higher out-of-pocket expenses that come with that plan design.

This approach reduces the employer's premium costs while still protecting employees from excessive medical bills. When an employee visits the doctor and owes a copay or works toward meeting their deductible, the MERP reimburses those costs. This structure has become increasingly popular as businesses look for ways to control rising insurance premiums without cutting benefits.

Health Reimbursement Arrangement (HRA)

An HRA represents the broader category under which many Section 105 plans fall. It's an employer-funded reimbursement account designed to cover eligible healthcare expenses. Employers have the flexibility to define which services qualify for reimbursement within the bounds of the IRS rules.

Two specific HRA types benefit small businesses:

- Individual Coverage HRA (ICHRA): ICHRA lets employers reimburse employees for individual health insurance premiums purchased on the marketplace. Employees have the freedom to choose their own coverage while the employer provides financial support.

- Qualified Small Employer HRA (QSEHRA): QSEHRA is designed for businesses with fewer than 50 employees who don't offer group health insurance. Employees must still maintain minimum essential coverage, such as those plans they can purchase from the marketplace.

Flexible Spending Account (FSA)

An FSA is a tax-advantaged financial account where employees set aside a portion of their pretax salary to cover eligible healthcare and dependent care expenses. It typically covers a wide range of qualified expenses, including medical and dental care, prescription medications, vision care, and certain dependent care costs. To take advantage of Section 105, an FSA can also be employer-funded. However, employees forfeit unused funds at the end of each year.

Recent IRS guidance has provided some flexibility through carryover provisions and grace periods that allow limited extension of spending time frames. In 2025, the grace period can be up to 2 1/2 months after the end of the plan year.

Section 105 Plans vs. Traditional Group Health Plans

Understanding the key differences between Section 105 plans and traditional group health insurance helps you determine which approach best fits your business needs. While both provide healthcare benefits to employees, they operate through fundamentally different structures and offer distinct advantages depending on your situation:

| Feature | Section 105 Plans | Traditional Group Health Plans |

|---|---|---|

| Structure | Employer-funded reimbursement arrangement for medical expenses | Comprehensive insurance policy that pools risk across employees |

| Cost Model | Variable costs based on actual employee expenses, though employers set reimbursement limits | Fixed monthly premiums regardless of claim activity |

| Flexibility | High flexibility, where employers decide the covered expenses, reimbursement limits, and eligibility criteria | Limited flexibility, where employers choose from a carrier's available plan options |

| Unused Funds | Revert to the employer if the employee leaves or doesn't use the full allocation | Carrier keeps the payments regardless of utilization |

| Risk Management | Employer controls exposure through reimbursement caps | Insurance carrier assumes risk and manages claims |

| Participation Requirements | Requires nondiscriminatory participation or eligibility requirements | Often requires minimum participation thresholds and employer contribution minimums |

| Best For | Businesses wanting cost control and flexible plan design | Businesses seeking predictable costs and comprehensive coverage managed by a carrier |

Section 105 plans can work alongside individual coverage or serve as a stand-alone benefit structure. The right choice depends on your workforce demographics, budget constraints, and strategic benefits goals. Many businesses find that combining elements of both approaches creates the most effective healthcare benefits package.

Frequently Asked Questions

To further understand how Section 105 plans work and their benefits, consider these common questions and their answers:

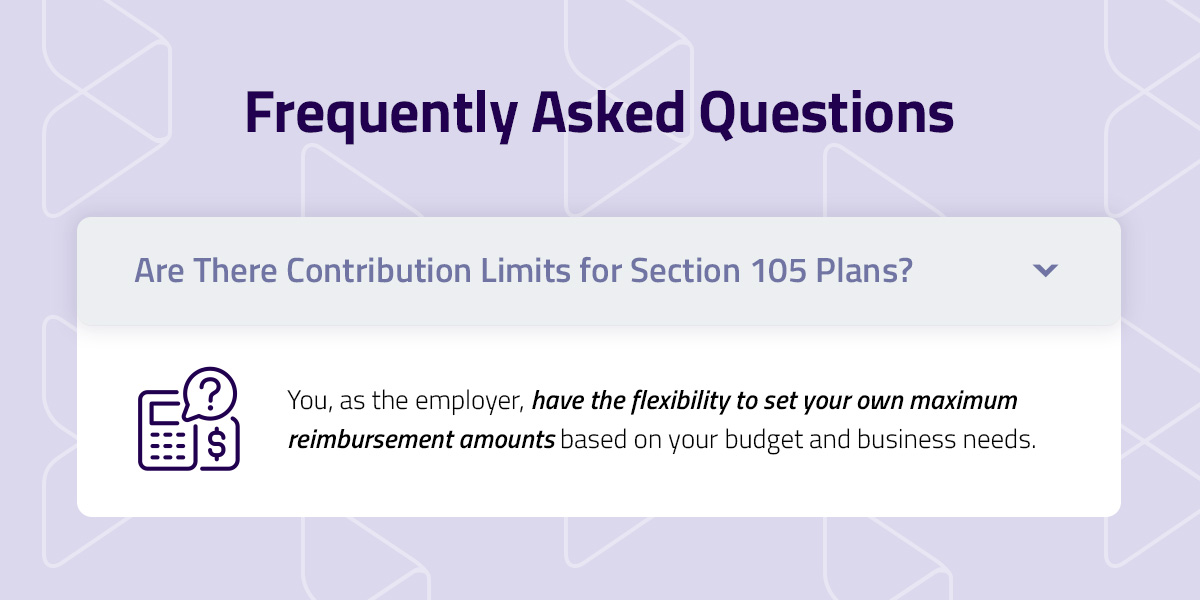

Are There Contribution Limits for Section 105 Plans?

Unlike HSA and FSA plans, most Section 105 plans don't have IRS-mandated contribution limits. You, as the employer, have the flexibility to set your own maximum reimbursement amounts based on your budget and business needs. However, QSEHRA's annual contribution cap that adjusts for inflation is an exception. For 2025, these limits are $6,350 for individual coverage and $12,800 for family coverage.

The key restriction isn't a dollar limit but rather a reasonable compensation standard. The total value of reimbursements provided to an employee must align with the work they perform for your business. Your plan documents should clearly outline maximum annual reimbursement caps to ensure compliance with this standard.

What Is the Difference Between Section 105 and Section 125 Plans?

Section 105 and Section 125 plans both offer tax advantages, but they differ in who contributes the funds. Section 125 plans, also called cafeteria plans, allow employees to make pretax contributions toward their benefits through payroll deduction. These plans let employees convert part of their taxable wages into pretax elections for benefits like health insurance premiums, HSA, dependent care, or group-term life insurance. Both you and your employees save on FICA and payroll taxes with Section 125 arrangements.

Eligibility rules also differ between the two. Partners, sole proprietors, and S-Corp shareholders owning over 2% cannot participate in Section 125 plans. Section 105 plans have similar restrictions but offer the spouse-employee workaround for sole proprietors. Many businesses use both plan types together strategically — a Section 125 plan for employee pretax contributions and a Section 105 plan for employer-funded reimbursements. This combination maximizes tax savings for everyone involved.

Is a Healthcare Reimbursement Account Worth It?

For most small businesses, healthcare reimbursement accounts offer significant value. The tax savings alone often justify the setup costs and administrative effort. These plans also give you greater control over healthcare spending compared to traditional insurance. The budget flexibility helps you manage costs while still offering competitive benefits that attract and retain quality employees.

However, be sure you understand the administrative requirements. You need written plan documents, proper recordkeeping, nondiscrimination testing, and ongoing compliance monitoring. For smaller businesses, managing this internally may feel burdensome. Working with a third-party administrator eliminates this concern by handling all compliance and administrative tasks, letting you focus on running your business while still enjoying the tax benefits.

Offer Cost-Effective Health Benefits With The Difference Card

Navigating Section 105 compliance can feel overwhelming, and the administrative burden can easily outweigh the benefits. The Difference Card can simplify the process for you. Our MERP solution handles administration and compliance, allowing you to enjoy tax savings without the headache.

Since 2001, we have helped clients achieve $2.13 billion in healthcare savings. Our team manages the entire reimbursement process, with 99% of claims processed in two days or less. Employees can even swipe The Difference Card Mastercard directly at the doctor's office for eligible copays. If you're ready to start saving, request a proposal today.