The Official MERP FAQ

Table of Contents

- What Is a MERP?

- What Expenses Are Eligible for MERP Reimbursements?

- How Does a MERP Differ From a Traditional Group Health Plan?

- How Does a MERP Differ From an HSA?

- What Are the Pros and Cons of MERP Products?

- What Are MERP Benefits for Brokers?

- Can a MERP Integrate With Other Health Benefits?

- What Are the Compliance Requirements for MERP Products?

- What Are Common MERP Misconceptions?

- How Can Producers Help Clients Maximize the Advantages of a MERP?

- See the Savings With The Difference Card

As healthcare costs rise, companies need options to help their employees afford quality care while minimizing employer expenses. Medical Expense Reimbursement Plans (MERP) are among the insurance producer's most effective tools for creating win-win group coverage solutions, but they're also among the most misunderstood healthcare products. Whether you want help understanding MERP products or explaining them to a client, this MERP FAQ guide will provide the straightforward answers you need.

What Is a MERP?

A MERP is a Medical Expense Reimbursement Plan — a healthcare solution that allows employers to reimburse their employees for eligible medical expenses. Employees may also claim reimbursement for the medical expenses of their eligible dependents, including spouses and children. These reimbursements are tax-free under the Internal Revenue Code (IRC) Section 105.

What Expenses Are Eligible for MERP Reimbursements?

IRC Section 105 outlines the expenses eligible for tax-free reimbursement from a MERP. These include:

- Many prescription and over-the-counter medicines

- Doctor visits

- Hospital care

- Emergency room and urgent care visits

- Surgeries

- Physical therapy

- Premiums and copays

- Dental care

- Glasses, contact lenses, and LASIK surgery

- First aid supplies

How Does a MERP Differ From a Traditional Group Health Plan?

MERP products have a few distinguishing features that set them apart from conventional group health insurance plans:

- Direct reimbursement: Where traditional health insurance involves the carrier paying the healthcare provider, a MERP requires the employee to pay for their care, but enables them to claim reimbursement from their employer. The employee can claim reimbursement from the employer's MERP fund by submitting proof of payment, such as an invoice or receipt. Some MERP products also provide employees with MERP debit cards with preloaded funds for allowable expenses.

- Employer funding: Traditional group health insurance typically requires contributions from both the employer and employee, while MERP products are often solely funded by employers. The employer can set the annual and monthly maximum reimbursement amounts per employee.

How Does a MERP Differ From an HSA?

A MERP is employer-funded and allows the employer to define covered expenses and reimbursement limits. Within these parameters, the employer uses their MERP funds to reimburse employees for eligible expenses and can deduct their employer contributions to the MERP as business expenses.

A Health Savings Account (HSA) is employee-owned and allows the employee and their employer to make tax-free contributions. These savings also grow tax-free, and the employee can withdraw funds tax-free to pay for eligible expenses.

MERP and HSA products have several similarities. Both offer tax advantages, integrate well with high-deductible health plans (HDHP), and can help employees afford a wide range of medical services. Which solution a producer should recommend depends on their client's priorities. An HSA tends to have simpler compliance requirements and gives employees the greatest autonomy in their medical spending, while a MERP gives the employer more control and predictable costs.

What Are the Pros and Cons of MERP Products?

Every healthcare solution has strengths and weaknesses depending on the situation, and understanding these can help you maximize the solution's benefits. Here are the MERP advantages and drawbacks you need to know about.

MERP Advantages

Producers can point to multiple benefits of MERP products when presenting them to employers, including:

- Tax advantages: Employers can deduct their MERP reimbursements as a business expense under IRC Section 162 to reduce their taxable income. These reimbursements are also exempt from Social Security and unemployment taxes. The tax advantages of MERP products extend to employees, too, as reimbursements for eligible expenses are not considered taxable income.

- Flexibility: With a wide range of eligible expenses and broad scope for customization, producers can help employers offer the MERP-based benefits that suit their priorities. This provides greater flexibility than traditional insurance, which limits employers to the coverage structure their carrier defines. Some MERP products even allow employers to build multiple member plan options for their employees on a single underlying group plan.

- Cost control: Employers can cap reimbursements and limit eligible expenses within the range of expenses allowable by the IRS. This helps to contain costs within a predictable range. Plus, MERP products can allow the employer to retain unused funds, which makes MERP products more cost-efficient than conventional insurance, which requires employers to keep paying premiums regardless of whether employees make claims.

- Improved recruitment and retention: By reimbursing medical expenses, MERP products help keep employees healthy and happy. They can contribute toward improved employee satisfaction, productivity, and retention. Enhancing a benefits package with a MERP can also help attract top talent.

MERP Disadvantages

Understanding the limitations of MERP products is crucial. If an employer has a need that a MERP alone can't satisfy, they may want to explore integrating a MERP with another healthcare solution or consider alternatives. Potential MERP drawbacks include:

- Administrative tasks: Reviewing and administering reimbursement claims can place new demands on company resources. The simplest solution is to partner with a third-party administrator (TPA) that offers MERP products and facilitates reimbursements.

- Compliance requirements: Employers must partner with a reputable producer and MERP carrier to ensure their MERP complies with legal requirements and healthcare regulations. A compliant MERP must have a Summary of Benefits and Coverage (SBC), a Summary Plan Description (SPD), and a nondiscrimination testing protocol.

- Communication challenges: Since many employers and employees are more familiar with traditional group insurance than MERP products, producers may need to provide more resources to help their clients understand this solution. Partnering with a MERP carrier that publishes helpful resources can save producers time while ensuring the employer and members understand their MERP product and how to use it.

- Upfront expenses: Unless the MERP carrier provides a MERP debit card for the employer to preload with funds, employees must pay medical bills themselves before seeking compensation. Integration with an HDHP and using a MERP debit card are viable solutions to this concern.

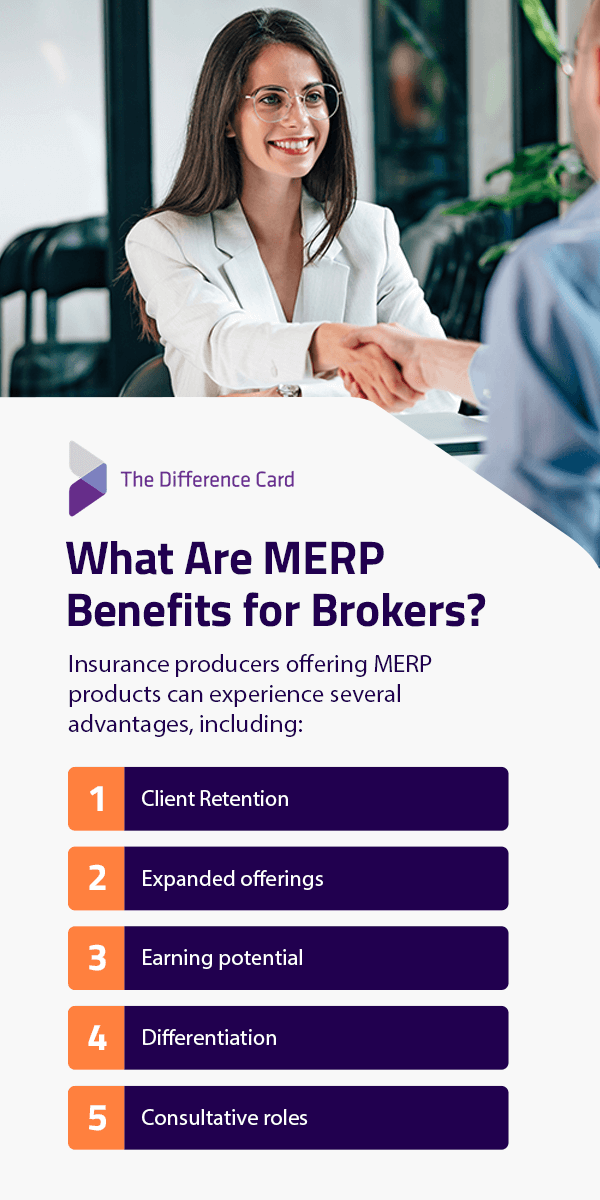

What Are MERP Benefits for Brokers?

Insurance producers offering MERP products can experience several advantages, including:

- Client retention: Offering MERP products lets producers create custom plans to suit each employer's needs. This customization can help enhance customer satisfaction and promote lasting client relationships.

- Expanded offerings: A MERP is a versatile tool in the producer's toolkit, equipping them to meet the needs of more diverse clients.

- Earning potential: Producers may charge commissions and fees for setting up and managing MERP products, increasing their potential income.

- Differentiation: In a competitive marketplace, offering MERP products can help a producer stand out and attract clients with personalized solutions.

- Consultative roles: The customization process allows producers to position themselves as trusted advisors to their clients.

Can a MERP Integrate With Other Health Benefits?

Yes, a MERP can integrate with other healthcare solutions. The most popular MERP integration is a MERP with a high-deductible health plan (HDHP). An HDHP allows employers to provide extensive coverage while paying low premiums, though employee out-of-pocket costs can run high. Contributing to a MERP lets employees offset deductibles, copayments, and coinsurance by receiving reimbursement. This integration creates a win-win healthcare arrangement for employers and employees.

Another option is to integrate an HDHP with an HSA, and add a MERP to cover expenses the HSA excludes, like vision or dental insurance premiums. MERP products can also combine with any traditional group insurance plan for comprehensive coverage.

What Are the Compliance Requirements for MERP Products?

MERP products must meet compliance standards set by several laws and regulations, including:

- ERISA: The Employee Retirement Income Security Act requires all group health plans, including MERP products, to meet reporting and disclosure requirements. These include providing an SPD and SBC and filing an annual report, Form 5500, with the Department of Labor. An SPD must explain the plan in a way the average participating employee can understand.

- ACA: The Affordable Care Act sets minimum essential coverage standards that group health plans must meet, such as full coverage for basic preventive services like screenings and vaccinations. MERP plans must either meet all these requirements themselves or integrate with group health insurance plans that fill the gaps to ensure compliance with essential coverage requirements.

- COBRA: The Consolidated Omnibus Budget Reconciliation Act applies to MERP products when integrated with group health plans that fall under COBRA. This act entitles employees to continue receiving temporary coverage after a qualifying event like termination of employment. COBRA seldom applies to stand-alone MERP plans or those integrated with a group plan when the employer meets small employer exception requirements.

- HIPAA: The Health Insurance Portability and Accountability Act requires MERP administrators to guard the confidentiality of employees' protected health information (PHI) through administrative, technical, and physical security. PHI includes an employee's medical history, diagnoses, treatment information, and Social Security number.

- IRC Section 105: This section of the Internal Revenue Code outlines the allowable expenses for tax-free reimbursements and requires MERP administration to implement nondiscrimination testing. Annual nondiscrimination testing ensures the plan does not favor highly compensated employees over lower-income employees.

What Are Common MERP Misconceptions?

MERP products are often misunderstood, meaning producers must be ready to answer client questions based on misconceptions. These misconceptions include thinking that MERP products are:

- For large companies only: MERP products offer flexibility and tax advantages that can benefit companies of all sizes. Larger companies may favor integrated MERP solutions, while stand-alone and integrated options can work for small companies.

- Expensive: The ability to control spending and carry over unspent funds often makes MERP products more cost-effective than traditional group plans.

- Noncompliant: A reputable MERP carrier can help producers and clients ensure their MERP plans meet all compliance requirements.

How Can Producers Help Clients Maximize the Advantages of a MERP?

A client-centric producer can use several methods to help clients get the most out of a MERP product. Here are four of the most effective strategies.

Educate Clients

Many clients are unaware of MERP products, how they work, and their benefits. To bridge this gap, client-centric producers can share presentations, brochures, online articles, and webinars. When employers have a firm grasp of what a MERP product can do for them, they're more likely to purchase one and collaborate with the producer to implement it effectively.

Customize Plans

Flexibility is one of the top benefits of MERP products. Producers can take advantage of this benefit by customizing plans for their clients to:

- Meet needs: Employers can tailor MERP plans to include the benefits most relevant to their workplace demographics, industry risks, and employee-specific activities. For example, construction workers may be at greater risk of musculoskeletal injury, and could benefit from higher reimbursement limits for physical therapy and orthopedic care.

- Save money: An employer can cap reimbursements at amounts that make sense for their benefits budget and limit coverage to the medical services their employees actually need.

- Motivate progress: Because employers can build several member plan designs on an underlying MERP, they can consider offering additional benefits to employees who hit key career milestones, join wellness initiatives, or achieve more years of service. This incentive structure encourages employees to pursue productivity and growth.

Leverage Data

Data is the producer's most valuable resource for tailoring MERP plans. Key data sources include claims, reimbursements, and employee experience surveys. Analyzing data from these sources can reveal which medical needs require additional coverage, which are less important, and what employees like and dislike about their benefits.

Demographic data can also be useful. For example, if older employees submit more claims for vision expenses, the employer could raise the reimbursement cap for these costs as employees age.

Promote Prevention

Preventive wellness measures are crucial to improving employee health and reducing an employer's long-term spending on reimbursements. Helpful tactics for promoting wellness include:

- Covering screenings, wellness visits, and vaccinations within MERP employee plans.

- Encouraging employees to use their MERP funds.

- Educating employees about health fundamentals like nutrition, exercise, and sleep.

- Partnering with local gyms to offer membership discounts to employees.

- Incentivizing participation in wellness programs with additional MERP funds or other benefits.

See the Savings With The Difference Card

A MERP is a producer's secret weapon to save clients money while providing superior flexibility and quality benefits. Teaming up with a reputable carrier is key to ensuring compliance and exceptional client-centric service. If you're a producer seeking a MERP carrier with a track record you can trust, The Difference Card is your ideal partner.

The Difference Card is a highly customizable and compliance-friendly MERP solution. Our clients receive support from a dedicated account manager, receive reimbursement approvals within two business days, and can manage their plans from a user-friendly mobile app and member portal. We also provide detailed plan reporting and savings tracking to help our partner producers show the clients the impact The Difference Card makes. Since 2001, The Difference Card has saved clients an average of 18% on annual healthcare costs, amounting to over $1 billion in savings and counting for our clients.

Request a proposal from The Difference Card today to help your clients see the difference.