Self-Insured vs. Fully Insured Health Plans for Employers

Table of Contents

Employee health insurance plans that balance comprehensive benefits with affordable premiums have become increasingly hard to find, often forcing employers to make tricky compromises. While self-insured plans offer flexibility, fully insured plans shift risk to the provider — but often at a higher cost for benefits your team may not need.

How do you make responsible choices for your valued employees' well-being in a complex marketplace? Use this guide to compare self-funded versus fully insured plans and find the ideal solution for your business.

Self-Funded vs. Fully Funded Insurance

This side-by-side comparison provides an at-a-glance look at these two plan structures, so you can determine which fits your organization's goals better.

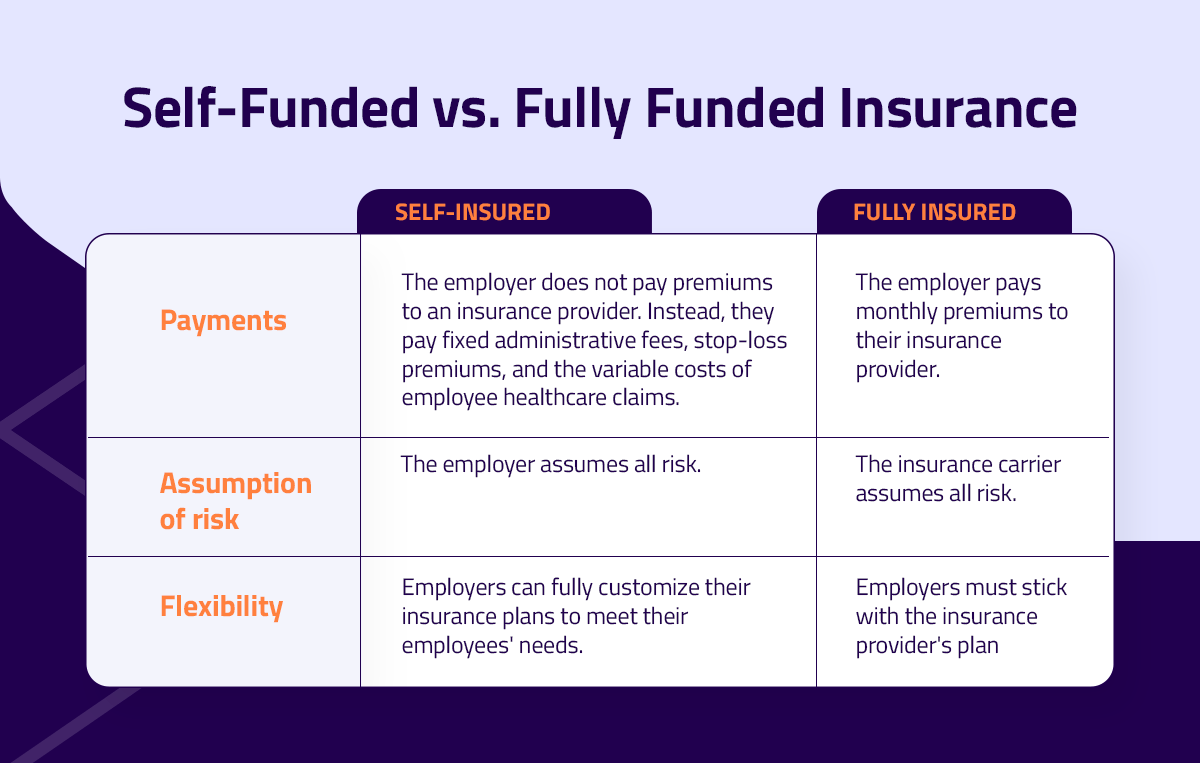

| Self-Insured | Fully Insured | |

| Payments | The employer does not pay premiums to an insurance provider. Instead, they pay fixed administrative fees, stop-loss premiums, and the variable costs of employee healthcare claims. | The employer pays monthly premiums to their insurance provider. |

| Assumption of risk | The employer assumes all risk. | The insurance carrier assumes all risk. |

| Flexibility | Employers can fully customize their insurance plans to meet their employees' needs. | Employers must stick with the insurance provider's plan options. |

What Is a Self-Funded Health Plan?

A self-funded or self-insured health plan does not require employers to pay monthly premiums to their insurance provider. With this option, you may choose to collaborate with a third-party administrator to manage policies and claims, freeing you to spend more of your time and energy on your daily responsibilities. TPAs reduce the need for in-house insurance management resources and provide expertise on policies and compliance adherence, and their popularity is on the rise.

Instead of opting for one of their insurance carrier's plan options, self-funded insurance lets employers customize plans to meet their employees' needs. With help from a TPA, self-funded plans enable employers to avoid unnecessary fees associated with fully insured plan costs.

While this flexibility is undoubtedly appealing, self-funded plans require employers to assume additional risk by covering unexpected claims or employee out-of-pocket expenses. There is also less consistency, as costs can change from month to month.

Employers often add stop-loss insurance to mitigate the risks associated with self-funded insurance plans. Stop-loss insurance allows employers to limit how much employees can claim. If an employee's claim exceeds this set amount, the insurance provider must cover the excess.

Self-Funded Health Plan Pros and Cons

Self-funded insurance policies have multiple benefits.

- Increased flexibility: Instead of opting for an insurance carrier's plan, self-insured policies enable employers to customize plans to their employees' needs.

- Potential cost savings: Employers pay for claims as they arise, potentially reducing costs compared to monthly premiums.

- Cost sharing: Self-insured policies allow employers to share costs with their employees for certain claims.

There are also potential downsides to be aware of.

- Increased risk: Without the coverage fully insured policies provide, unexpected costs can fall on the employer.

- Unpredictability: With costs varying from month to month, self-insured plans may make budgeting challenging.

- Increased administration: Though TPAs can provide assistance, it is ultimately the employer's responsibility to administer and organize a self-insured plan.

What Is a Fully Funded Health Plan?

A fully funded or fully insured health plan is a more conventional approach. Employers pay monthly premiums to their insurance carrier, and when covered employee medical expenses arise, it is the insurance company's responsibility to pay for them.

Fully insured plans shift financial risk to the carrier, but any surplus after claims stays with the insurer. Despite offering short-term predictability, they often cost more than self-funded plans over the long term due to higher premiums and taxes.

Fully Funded Health Plan Pros and Cons

Fully funded insurance policies provide multifaceted advantages.

- Predictability: Fixed monthly installments do not waver, making it much simpler to budget for insurance.

- Less administration: Since the insurance carrier manages the policy plan and claim, employers do not need to worry about policy-based administration.

- Lower financial risk: Employers who choose fully insured health plans won't have to cover unexpected costs even if their employees submit extensive claims.

Fully funded insurance policies include possible drawbacks.

- Rigidity: Policy plans may not be flexible enough to cover all employees' health requirements.

- High recurring costs: Unless employees incur very high unexpected costs, monthly premiums tend to be more expensive than the monthly costs associated with a self-insured plan.

- Wasted money: If you and your employees do not maximize your coverage, surplus payments will go to the insurance carrier.

Beyond the Basics — A Comprehensive Look at HRA Products

Employers might consider a health reimbursement arrangement when exploring health insurance coverage for their employees. With this employer-funded setup, employees initially pay for their medical expenses and get repaid for qualifying expenses and premiums.

An HRA has several defining characteristics.

- Non-portable: Unlike a health savings account, an HRA is not portable. In other words, an employee who leaves the company cannot keep it.

- Predetermined amount: The employer chooses how much money to allocate to each employee's HRA. All workers who fall under the same classification — like full-time versus hourly — must receive the same HRA contribution amount.

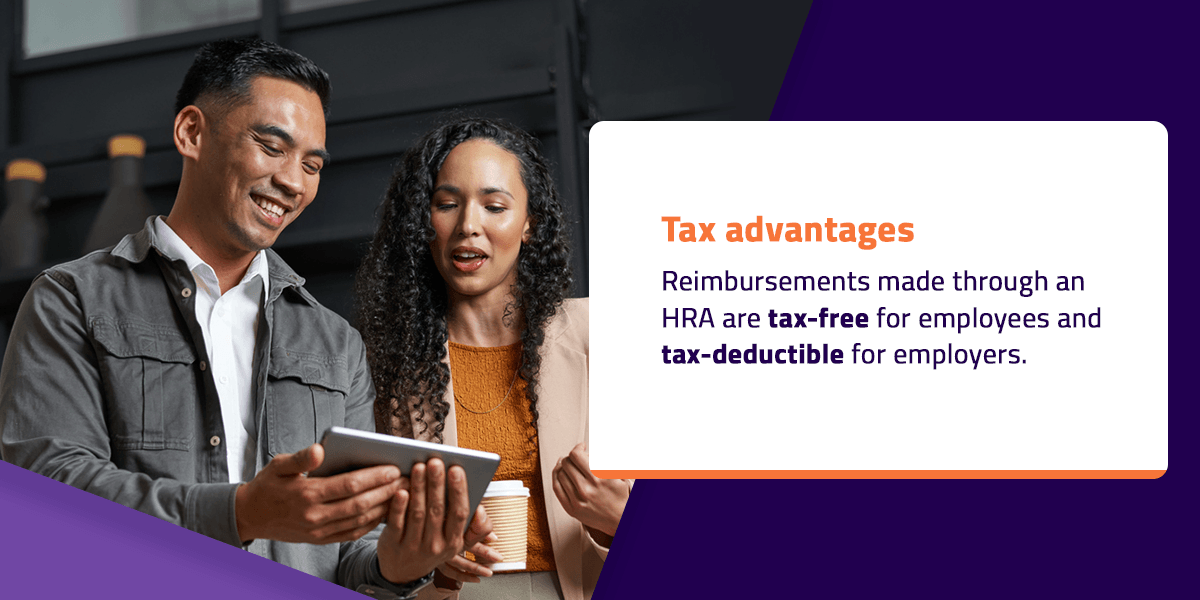

- Tax advantages: Reimbursements made through an HRA are tax-free for employees and tax-deductible for employers.

- Predetermined coverage: Employers can decide which medical expenses and insurance premiums qualify for an HRA.

Individual Coverage HRA

An ICHRA is an employer-sponsored health benefit that enables the employer to set a monthly allowance for their employees to use for eligible medical expenses. Any employer with at least one employee can choose this tailored coverage, making it an accessible option for all businesses.

- Employee choice: Employees can select health plans that suit their unique needs.

- Budget control: Fixed monthly allowances eliminate unpredictable costs.

- Tax advantages: Reimbursements made through an HRA are tax-free for employees and tax-deductible for employers.

Qualified Small Employer HRA

The qualified small employer HRA is also a viable option for many small businesses. A QSEHRA is another insurance device that enables employers to reimburse employees for approved medical expenses, premiums, and coinsurance costs, provided the employees maintain minimum essential coverage.

To qualify for a QSEHRA, a company generally must:

- Employ fewer than 50 full-time workers.

- Not already offer a group health insurance plan, such as a SHOP plan or an FSA.

- Offer the same terms for all full-time employees. However, reimbursement amounts can vary depending on variables such as age.

With a QSEHRA, employers can decide how much they want to contribute to their employees’ health care costs, up to an annual maximum set by the IRS.

Initially, employees pay for their healthcare costs through their insurance carrier, and later get reimbursed by the QSEHRA after submitting proof of payment. If an employee does not make a claim or use their employer's entire contribution by the end of the policy year, they may retain the unused amount or roll it over to the next year of employment.

MERP Products as a Bridge to Self-Funding

A medical expense reimbursement plan, or MERP, strikes a balance between cost-effectiveness and comprehensive benefits.

For employers who do not want to pay high insurance premiums and cannot fully fund their employee health insurance policies, a medical expense reimbursement plan combines the flexibility of self-funded plans with the predictability of fully funded policies.

How Does a MERP Work?

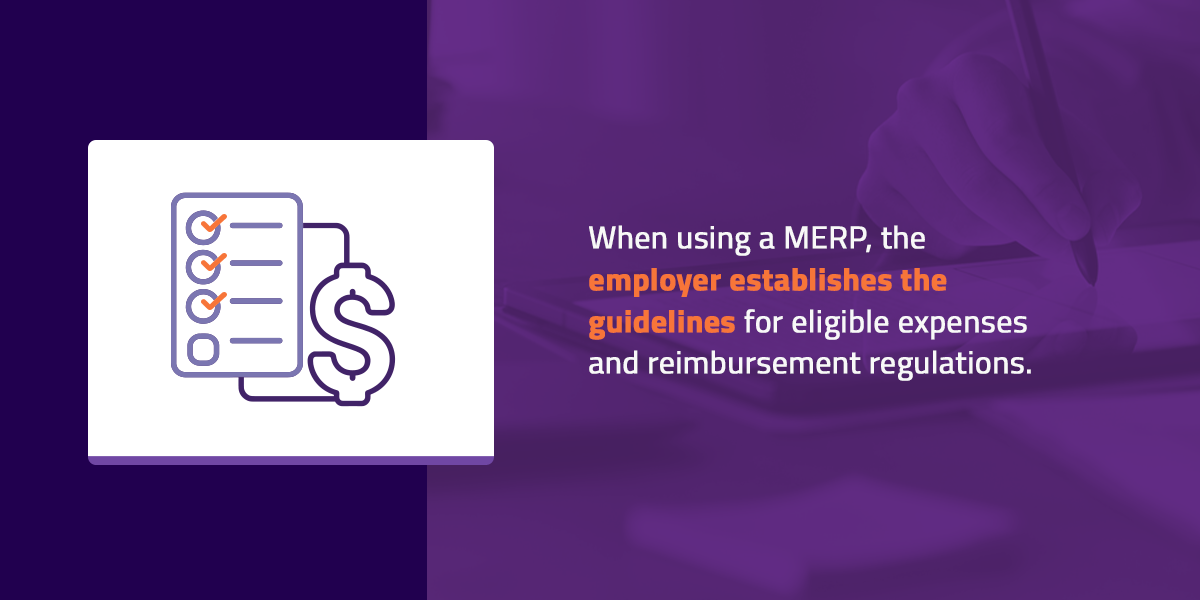

When using a MERP, the employer establishes the guidelines for eligible expenses and reimbursement regulations. Employees contribute to a MERP via pre-tax payroll deductions, and when they submit eligible claims with appropriate documentation, they receive reimbursements from the plan administrator.

Typically, a MERP process constitutes five simple steps:

- The employer sets a monthly allowance.

- Employees pay for health products and services out of pocket.

- Employees request reimbursement, supported by proof like receipts or EOBs.

- The employer reviews the requests and documentation.

- The employer reimburses their employees.

-

What Makes a MERP Different?

A MERP is very similar to an HRA — employers can use them to repay employees for eligible out-of-pocket medical expenses, and the reimbursements are tax-free for employees and tax-deductible for the employer.

A MERP provides employers and employees with the flexibility they need to meet their financial and medical needs. When designing a MERP, employers can decide their preferred contribution amounts, eligible expenses guidelines, and reimbursement processes. This fluidity enables employers to plan their employee healthcare insurance plans around their budget and preferred timelines.

In addition to complete customizability, employers can also apply more than one MERP to a single insurance plan, providing options for employees' varying needs.

MERP products also cover a wide range of healthcare expenses, many of which an HRA or other insurance policies do not always cover:

- Hospital services

- Doctor visits

- Prescription medication

- Dental and vision expenses

- Health plan deductibles

MERP products give employees more financial freedom. Depending on the type of MERP you have, your team can pay for some services directly.

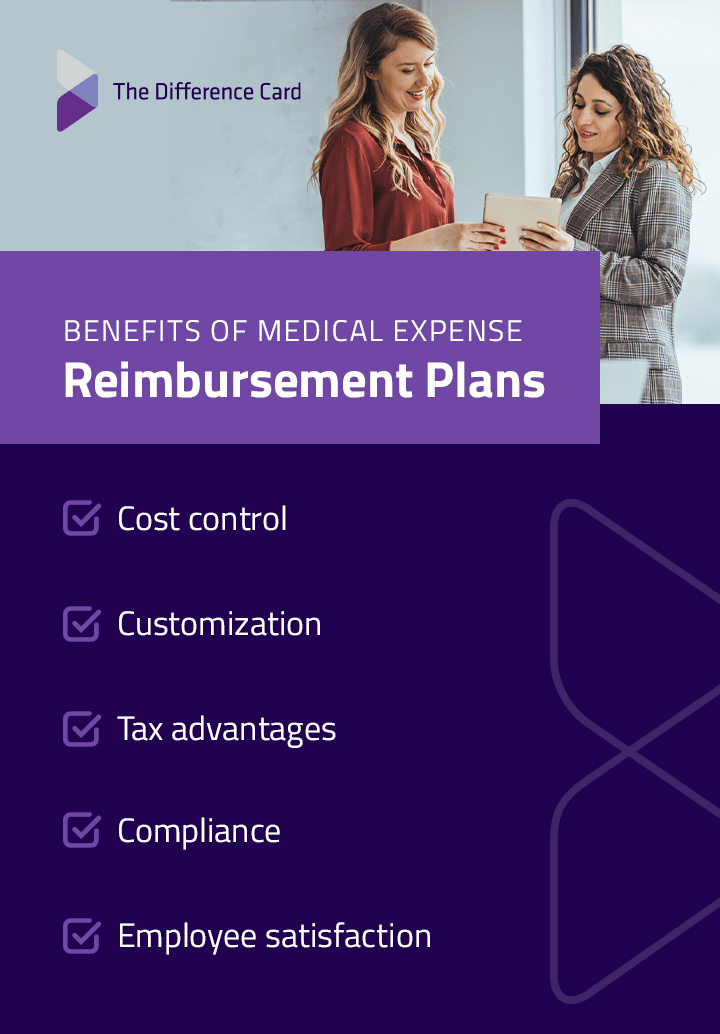

Benefits of Medical Expense Reimbursement Plans

- MERP products combine the best elements of self-insured and fully insured health plans.

- Cost control: With a MERP, employers can set their preferred contribution limits, decide which expenses are eligible, and have complete control over their healthcare budget.

- Customization: A MERP offers employers a flexible, easy-to-tailor design process.

- Tax advantages: Contributions made to a MERP are often tax-deductible for employers, providing them with potential savings via deductions.

- Compliance: A valid MERP must comply with relevant regulations, so employers do not have to worry about meeting legal requirements.

- Employee satisfaction: Reimbursing team members' healthcare expenses may boost morale, make your employee benefits package more attractive, and can attract and retain top talent.

The Difference Card MERP

The Difference Card offers all the benefits of a standard MERP with extra perks.

- Detailed plan reporting: The Difference Card provides daily, weekly, and monthly data, offering valuable insights into data usage.

- Savings tracking: We track how much money the MERP has saved to provide concrete evidence of your plan's success.

- Dedicated account management team: Every member of The Difference Card receives assigned managers who streamline plan implementation and employee communications.

- Guaranteed savings: You can include a reinsurance policy that saves your organization money regardless of the circumstances.

- Simplified process: Integrating the MERP lets employees easily take advantage of the copay services.

See the Difference Today

The Difference Card streamlines health insurance for you and your team. This accessible MERP solution blends the strengths of fully funded vs. self-funded plans without the usual compromises.

Explore The Difference Guarantee or request a proposal today.