What Is an ICHRA?

Table of Contents

Every renewal season feels the same. Your broker provides new rates, premiums have increased again, and you're left deciding whether to absorb the cost or ask employees to contribute more.

But what if you could break that cycle? An Individual Coverage Health Reimbursement Arrangement (ICHRA) is an alternative to traditional health insurance options. Instead of a one-size-fits-all plan, you set a budget and let employees choose the coverage that fits their needs. You gain predictable costs. Your team gains flexibility.

Our guide explains how an ICHRA works and what you need to know about this specific plan. We'll also introduce a Medical Expense Reimbursement Plan (MERP), a strategic plan that can offer even greater savings.

The ICHRA Fundamentals

ICHRA plans became available through federal regulations finalized in 2019 and implemented in 2020. This regulatory change expanded options for employers who felt locked into traditional group coverage or unable to offer benefits. The launch coincided with rising healthcare costs and increased demand for flexible benefit options, making an ICHRA ideal for smaller businesses seeking alternatives to group plans.

The flexibility of an ICHRA goes beyond just letting employees choose their own coverage. You can set specific allowance amounts across different employee classes based on factors such as full-time versus part-time status, geographic location, or whether they're salaried or hourly. Within each class, you can also vary those amounts based on age and family size. There's no minimum or maximum contribution requirement, which means you control exactly how much you spend each month.

These plans operate under Section 105 of the Internal Revenue Code, which governs employer-provided health benefits. When structured correctly, your contributions and employee reimbursements are exempt from federal income tax and payroll taxes. The IRS and the Department of Health and Human Services regulate ICHRA plans to ensure compliance with both tax law and the Affordable Care Act (ACA).

As an employer-sponsored benefit plan, an ICHRA is subject to regulations under the Employee Retirement Income Security Act (ERISA), which sets standards for plan administration and participant protections. This regulatory framework ensures that the tax advantages and compliance requirements work together, providing a legitimate alternative to traditional group health insurance while maintaining the tax benefits you and your employees expect from employer-sponsored coverage.

How an ICHRA Works

Once you've decided an ICHRA fits your business, the implementation process takes 60 to 90 days. Setting up and running an ICHRA involves several key steps.

Step 1: Design Your ICHRA

Decide which employee classes you'll offer the benefit to and set reimbursement allowances for each class. You can vary allowances based on age and family size within each class. There's no minimum or maximum contribution requirement, giving you complete budget control.

Step 2: Choose Your Coverage Effective Date

Pick when you want the ICHRA to start. Employees will need to have individual health insurance coverage in place by this date to receive reimbursements.

Step 3: Notify Your Employees

The ACA requires written notice to eligible employees at least three months before the start of the plan year or 90 days before their hire date for new employees. This notice must include:

- A description of the ICHRA terms

- The employee's permitted benefit amount

- A statement that if they enroll in individual coverage through the healthcare marketplace, they may lose any premium tax credit eligibility

- Contact information for the Health Insurance Marketplace

- A warning that if they don't have minimum essential coverage, they may be subject to tax penalties in certain states

Step 4: Employees Shop for Coverage

Your employees purchase individual health insurance policies meeting minimum essential coverage requirements under the ACA. They can choose plans from the Health Insurance Marketplace, work with insurance brokers, or buy directly from insurance carriers.

It gives them the freedom to select coverage to fit their healthcare needs, preferred doctors, and budget. They can compare multiple plans and metal tiers — Bronze, Silver, Gold, and Platinum — to find the right balance between monthly premiums and out-of-pocket costs, something they can't do with a one-size-fits-all group plan.

Many employees appreciate being able to compare deductibles, copayments, prescription drug coverage, and provider networks before making their selection. This shopping process happens during open enrollment periods or within 60 days of a qualifying life event.

Step 5: Claim Submissions and Reimbursement

Employees must submit proof of insurance premiums and eligible medical expenses. You review the claims, verify coverage, and reimburse employees up to their allowance amount. When processed correctly, all reimbursements are tax-free for both you and your employees.

ICHRA Eligibility

ICHRA eligibility works differently for employers and employees, with specific requirements that determine who can offer the benefit and who can participate.

- For employers: Any business can offer an ICHRA, regardless of size. Whether you have five employees or 500, you can establish an ICHRA. You can offer it to all staff or specific employee classes. However, you cannot offer both a traditional group health plan and an ICHRA to the same class of employees. You can offer different benefits to different classes — for example, a group plan for full-time employees and an ICHRA for part-time workers.

- For employees: To receive tax-free reimbursements through an ICHRA, employees must have individual health insurance offering minimum essential coverage. It includes plans purchased through the Health Insurance Marketplace, directly from insurance companies, and certain other coverage types, such as Medicare Part A, B, and C.

Employees can decline the ICHRA if they prefer to purchase insurance without reimbursement or if they have another coverage source, such as their spouse's employer plan. This option allows them to qualify for premium tax credits through the Marketplace, which they cannot receive if offered an ICHRA.

The IRS allows you to create employee classes based on these criteria:

- Full-time vs. part-time employees: You can offer different allowances or offer the ICHRA to one group but not the other.

- Salaried vs. hourly workers: Compensation structure can define separate classes.

- Geographic location: Employees working in different states or rating areas can be in different classes, which is helpful when insurance costs vary significantly by region.

- Seasonal employees: Workers hired for a specific season can form their own class.

- Employees covered by collective bargaining agreements: Union and non-union workers can be separate classes.

- Combination classes: You can combine categories, such as offering one ICHRA to full-time employees in California and Texas.

For example, a retail company with locations in Illinois and Florida might offer a $500 monthly ICHRA allowance to full-time employees in Illinois, where health insurance premiums tend to be higher, and a $400 monthly allowance to Florida full-time employees. Part-time employees in both states might receive a $250 monthly allowance for their different coverage needs and your budget allocation.

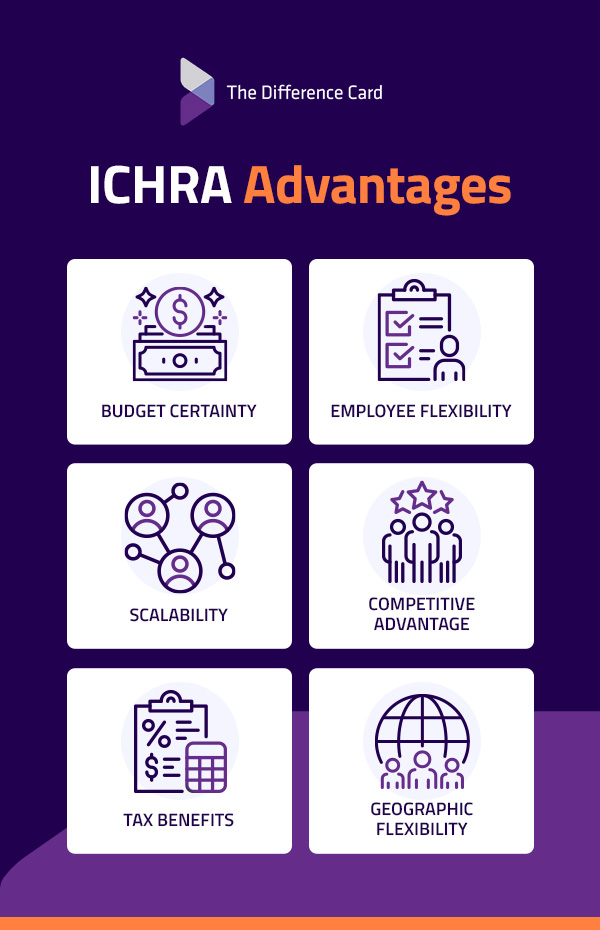

ICHRA Advantages

An ICHRA offers several benefits that make it an attractive alternative to traditional group health plans.

Benefits include:

- Budget certainty: You set fixed reimbursement amounts, so you know what you'll spend on healthcare benefits. Unlike group health insurance, your ICHRA costs remain consistent unless you choose to adjust allowances. This predictability makes budgeting and financial planning easier for growing businesses.

- Employee flexibility: Your staff can choose their own health plans and doctors. This freedom allows employees to maintain their established healthcare relationships or to address specific medical needs that require access to certain specialists or facilities.

- Scalability: Whether you have five employees or 500, an ICHRA can work. You can start small and expand as your business grows, adding new employee classes or increasing allowances over time without the complexity of switching insurance carriers.

- Competitive advantage: Offering healthcare benefits helps you attract and retain quality employees, even if you're not large enough to access affordable group coverage or if your industry faces challenges with traditional insurance.

- Tax benefits: Employer contributions are tax-deductible business expenses, while employees receive reimbursements tax-free. There are no payroll or income taxes on the benefit, which creates savings for both employers and employees.

- Geographic flexibility: For businesses with remote workers or multiple locations, an ICHRA eliminates the challenge of finding a group plan that adequately covers all areas. Employees can select plans available in their specific location.

Potential Disadvantages

While an ICHRA can offer many benefits, there are some considerations to keep in mind.

These considerations include:

- Premium tax credit impact: Qualifying employees cannot also receive premium tax credits through the Health Insurance Marketplace. An ICHRA is affordable if it costs the employee no more than a certain percentage of their household income, calculated using the cost of the lowest-cost Silver plan in their area.

- Administrative requirements: You'll need to verify that employees have qualifying coverage, process reimbursement claims, and maintain documentation for compliance purposes. Compliance includes following HIPAA privacy requirements when handling employee health information. While administration is generally simpler with an ICHRA than a traditional group health plan, it's not entirely hands-off.

- Employee resources: Employees may be unfamiliar with shopping for individual health insurance and may need assistance understanding their options, different coverage levels, and evaluating costs. Provide resources and support to help them shop confidently.

- State-specific considerations: Some states have additional regulations around ICHRA plans or healthcare coverage that you'll need to understand and follow. A few states also have individual mandates that require residents to have health insurance or pay a penalty.

The Difference Between an ICHRA and Other Health Plans

Understanding how an ICHRA compares to other health benefits helps you make an informed decision about which approach best fits your business needs.

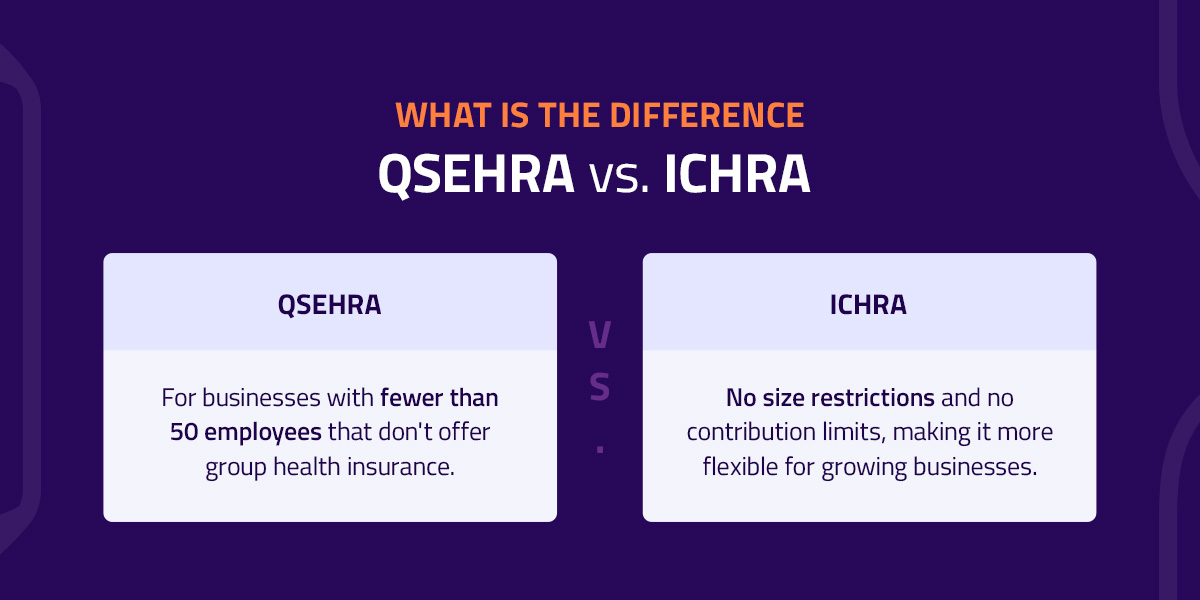

ICHRA vs. QSEHRA

A Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) is similar to an ICHRA but has key restrictions. QSEHRA is only for businesses with fewer than 50 employees that don't offer group health insurance. The IRS also sets annual contribution limits — $6,450 for individual coverage and $13,100 for family coverage in 2026.

An ICHRA has no size restrictions and no contribution limits, making it more flexible for growing businesses.

ICHRA vs. Traditional Group Health Insurance

Group plans offer simplicity. It's one plan for everyone. But limited flexibility and often unpredictable cost increases. An ICHRA gives employees choice and gives you budget control, but requires more employee education and individual plan shopping.

Group plans may be better if you want a turnkey solution and have a relatively homogeneous workforce with similar coverage needs. An ICHRA excels when your team has diverse needs or when you want completely predictable healthcare costs.

ICHRA vs. COBRA

When employees leave your business, the Consolidated Omnibus Budget Reconciliation Act (COBRA) allows them to continue their group health coverage temporarily. An ICHRA works differently, as employees own their individual health policies.

If an employee leaves, they keep their individual insurance plan and stop receiving your reimbursements. It is simpler for both parties than navigating COBRA continuation requirements.

ICHRA vs. Health Stipends

Giving employees money to buy health insurance creates taxable income for them and doesn't meet the ACA employer mandate requirements if you have 50 or more full-time employees. ICHRA offers the same flexibility, with tax advantages and regulatory compliance built in, making it a great option for businesses that want to support employee healthcare costs.

The MERP Advantage

While an ICHRA covers insurance premiums and can reimburse out-of-pocket medical costs, pairing it with a MERP creates a more comprehensive benefit package for your employees.

A MERP is a Section 105 plan that reimburses employees for qualified medical expenses, such as healthcare deductibles, coinsurance, and copays. Offering employees an ICHRA for premium coverage and a MERP for additional medical expenses provides financial support for a range of healthcare costs.

This combination is highly effective when employees choose high-deductible health plans to keep their premium costs lower. The ICHRA covers their monthly premiums, and your MERP helps with out-of-pocket medical costs.

For example, an employee might choose a Bronze plan with lower premiums through the ICHRA, knowing that the MERP will help cover higher deductibles and copays when they have a doctor's appointment or need to fill prescriptions.

Benefits of a MERP

A MERP offers several advantages that make it a powerful complement to your ICHRA:

- Transparency: With a MERP, it's clear exactly what healthcare expenses are eligible for reimbursement. Your employees can better manage their out-of-pocket healthcare costs.

- Flexibility: You can switch to different health insurance carriers and adjust plan designs through a MERP. An HRA is much more difficult to move or alter.

- Control: You have full control over what expenses qualify and can set the guidelines for reimbursement. Additionally, unspent funds from the MERP can carry over into the following year's program.

- Rate stability: You gain the ability to stabilize rates at renewal, giving you predictable healthcare costs year over year instead of facing unexpected premium increases.

See What You Could Save With The Difference Card

Ready to explore whether an ICHRA makes sense for your business? With 25 years of cost-saving healthcare solutions, The Difference Card makes it easy to set up, manage, and optimize your ICHRA with our comprehensive platform and expert support. We handle the complexity of eligibility verification, claims processing, and compliance tracking, so you can focus on growing your business.

Our team guides you through plan design, employee education, and ongoing administration. Plus, with our exclusive Difference Guarantee, we ensure you're getting the most value from your healthcare benefits dollar.

To see how much you could save with an ICHRA designed specifically for your business, contact our team to discuss your unique needs.

We'll connect you with a dedicated account manager to help you create a benefits package that works for your budget and your people.