HMO vs. PPO vs. EPO: Which Health Insurance Plan Is Right for You?

Table of Contents

If you're looking for your next health insurance plan, you already know that there are countless options to choose from, ranging from providers to networks to coverage types.

As if navigating the health insurance market wasn't already challenging enough, companies often use confusing acronyms without providing proper explanations, such as HMO, EPO, and PPO.

This guide is your ultimate resource for finding answers to all your health insurance questions, like what HMO, PPO, and EPO insurance are, and which one is right for you.

HMO vs. EPO vs. PPO: Key Differences at a Glance

HMO |

PPO |

EPO |

|

| Cost | Budget-friendly, lower monthly premiums, and lower deductibles. Generally most affordable. | Higher monthly premiums that enable easier access to out-of-network services. Generally least affordable. | More affordable premiums than PPO plans but more expensive than HMO plans. |

| Out-of-network coverage | Coverage is generally restricted to in-network treatment, except for emergency care. | Coverage is available for both in-network and out-of-network services. | Coverage is generally restricted to in-network treatment, except for emergency care. |

| Personal care provider | Generally requires the appointment of a PCP to oversee your healthcare. | Does not generally require a PCP. | Does not generally require a PCP. |

| Referrals | Generally required in order to receive specialist attention. | Not required. | Not required for non-gated plans, but may be required for gated plans. |

| Flexibility | Least flexible. | Most flexible. | More flexible than HMO plans but less flexible than PPO plans. |

What Is an HMO Plan?

A health maintenance organization (HMO) plan is a traditional type of medical insurance plan offered by many private health insurance companies.

As the name suggests, HMO health insurance plans revolve around maintaining your health, focusing on preventive and wellness care treatments to avoid illness, and therefore keeping costs low.

HMO plans utilize an established network of doctors, hospitals, specialists, and other healthcare professionals. To receive coverage, members of an HMO plan must generally only use in-network providers for all their healthcare needs. Whether for a routine check up, a specialist appointment, or a hospital stay, an HMO plan requires you to see a provider within its network. As a result, HMO plans may require you to live or work in their specific service area to qualify for coverage.

Key characteristics of an HMO insurance plan include:

- In-network services only: Unless you require emergency care, out-of-area urgent care, or temporary dialysis, an HMO plan is unlikely to cover medical care provided by professionals or institutions beyond its established network.

- Monthly premiums: Most HMO plans require you to pay monthly premiums to keep your insurance plan and coverage active.

- Appointed primary care provider: In general, HMO insurance plans require the assignment of a primary care provider to oversee your healthcare treatments and services, provide referrals, and facilitate your appointments. A PCP is typically a doctor, but can sometimes be a physician assistant or nurse practitioner.

- Referrals required: Most HMO plans require you to obtain referrals from your PCP for specialist care and appointments. That means individuals on an HMO insurance plan do not generally have direct access to specialists.

- Budget-friendly: HMO plans tend to be the most affordable type of health insurance policy compared to EPO and PPO plans. This is usually because HMO plans operate within smaller, more restricted networks. PPO networks are larger and provide more options, and both PPO and EPO plans provide direct access to specialist care.

Who Is an HMO Plan Best For?

HMO plans have a range of benefits for both employers and individual plan members. In general, they are well-suited to those who:

- Require lower costs: HMO plans are ideally suited to those with more limited budgets, thanks to their lower monthly premiums, deductibles, and copayment options.

- Would prefer a primary care provider: If you would prefer having one person dedicated to organizing and overseeing your healthcare, and a focal point for all your healthcare communications, an HMO can provide you with an appointed PCP.

- Don't need direct access to specialists: If needing a doctor referral for each specialist visit won't be an issue, or if you don't foresee requiring frequent specialist appointments, an HMO plan could work well.

- Are happy with the established provider network: HMO plans require covered members to restrict their healthcare and treatment to organizations and professionals within the HMO network. If you do not foresee needing out-of-network attention, an HMO plan can be a viable option.

- Don't travel frequently: As HMO plans limit you to seeing professionals within their network, you will likely not be able to seek covered medical care while traveling.

- Prefer less paperwork: As your PCP generally oversees your healthcare, and most treatments are organized within the network, members of HMO plans are less likely to be required to personally complete paperwork, such as preapprovals for certain treatments.

What Is a PPO Plan?

A preferred provider organization (PPO) plan is an insurance policy that provides covered members with more flexibility and a wider network than HMO plans, generally at higher prices.

PPO plans give individuals the option to either limit their treatment to in-network providers for a lower cost, or seek external care at additional costs. Services within a PPO network require lower cost-sharing options, such as copay and coinsurance, and most out-of-network treatment will require the submission of an insurance claim.

Other out-of-pocket costs for a PPO plan include premiums, copays, and an annual deductible, all of which are generally higher than those for an HMO plan.

Key characteristics of a PPO insurance plan include:

- No primary care provider: Members of a PPO plan are not generally required to have an assigned PCP, and instead manage their healthcare needs and organize specialist treatment themselves.

- Established provider network: Just like an HMO plan, members with PPO coverage have access to an established network of healthcare organizations and professionals, many of which have pre-agreed discounted rates for plan members. PPO networks tend to be bigger than HMO networks, providing individuals with more choices.

- Out-of-network coverage: Unlike HMO plans, PPO plans offer more flexibility and allow for out-of-network coverage. However, out-of-network services often incur higher deductibles, copayments, and coinsurance.

- No referrals needed: PPO insurance plans offer more direct access to specialist care and don't require you to obtain referrals from a doctor or PCP. This can streamline treatment for anyone in need of specialist attention.

Who Is a PPO Plan Best For?

PPO insurance plans provide covered individuals with many benefits, and for those with higher budgets or more specialized health requirements, they may be the best option.

Generally, a PPO plan is ideally suited to those who:

- Prioritize flexibility: If you would prefer the freedom to choose any doctor or healthcare provider and don't want to limit yourself to the plan's provided network, PPO plans give you more options.

- Require direct access to specialists: Without needing a referral from a PCP, PPO plans give you more seamless access to specialist care.

- Have a higher budget: PPO plans are a viable option if you are able or willing to pay higher monthly premiums, deductibles, and copayments, in return for a wider network of providers and access to external care.

- Desire more control: Without a PCP, a PPO plan gives you the opportunity to coordinate your healthcare with a more hands-on approach.

- Travel frequently: For those who travel frequently and may need out-of-area medical attention on a regular basis, a PPO plan gives you the freedom to receive external medical support when needed.

- Don't mind more paperwork: With more power comes more responsibility. Without the centralized approach of an HMO plan and a PCP, you may have more administrative responsibilities, such as preapprovals for certain treatments.

What Is an EPO Plan?

An exclusive provider organization (EPO) plan is a hybrid managed health insurance plan that combines many aspects of both HMO and PPO plans.

There are two types of EPO — gated plans and non-gated plans. Both types have a similar structure to HMO plans, where your covered healthcare services are available from a network of preselected providers. However, if you have a non-gated EPO plan, you do not require referrals to see specialists and will generally not have a designated PCP.

Key characteristics of an EPO insurance plan include:

- Exclusive network: Similar to an HMO, EPO plans have an established network of healthcare professionals and do not generally cover out-of-network services, unless in the case of an emergency.

- PCP not generally required: Members of an EPO plan do not always require a PCP to coordinate their healthcare. While individuals on a gated plan may be assigned a PCP for referrals, non-gated plans do not require you to have a PCP.

- Direct access to specialists: Most EPO plans don't require covered members to obtain referrals in order to see a specialist, provided the specialist is within the established network. This is most common for non-gated EPO plans.

- Cost-effective: EPO insurance plans are more affordable than most PPO plans and offer more flexibility than HMO policies.

Who Is an EPO Plan Best For?

EPO plans combine the best of both worlds, offering individuals the flexibility of a PPO without its steep premiums. This type of plan is best suited to those who:

- Want to balance cost with flexibility: If neither element is more important than the other, EPO plans don't require you to choose between the two.

- Are happy with the established network: If you don't mind being limited to the professionals and establishments within the EPO network, and if you don't anticipate needing much out-of-area care, an EPO plan is a viable option.

- Don't want or need a PCP: EPO plans don't always require you to have an assigned PCP, giving you more autonomy and control over your healthcare management.

- Require direct access to specialists: If you anticipate needing frequent specialist attention, many EPO plans enable you to be seen and treated without a referral.

Key Health Insurance Terms to Know

To fully grasp how each health insurance plan works, it's essential to have a clear understanding of common insurance terms.

| Term | Definition |

| Premium | The cost of keeping your insurance plan and coverage active, usually a monthly cost. |

| Deductible | The amount you must pay yourself before your insurance provider contributes. |

| Primary care provider (PCP) | The primary point of contact for members of an HMO policy and some EPO policies. They oversee your healthcare and provide specialist referrals when needed. |

| Specialist | A healthcare professional who treats or focuses on a specific area of healthcare, such as a particular area of the body, or a type of illness or injury. For example, a cardiologist specializes in the health of the heart and blood vessels. |

| Emergency care | Urgent medical services required for life-threatening conditions or acute illnesses. Emergency care is typically covered by all three health insurance types. |

| Referral | A written order from a healthcare professional, usually a PCP, to be seen or treated by a specialist or receive specific medical services. |

| In-network care | Healthcare services provided by professionals and organizations within your policy's established network. |

| Out-of-network care | Healthcare services provided by professionals and organizations outside your policy's established network. |

| Coinsurance | The amount the insured person is responsible for paying beyond the deductible, usually established as a percentage. |

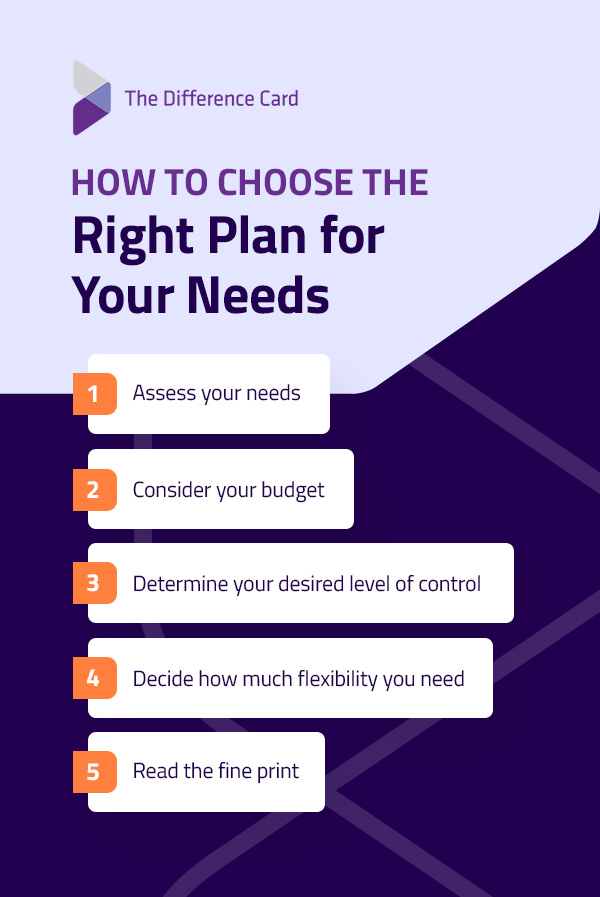

How to Choose the Right Plan for Your Needs

With healthcare plans, there is no one-size-fits-all approach to finding one that's right for you. To determine your ideal type of plan, you must:

- Assess your needs: Consider your existing medical conditions and current healthcare needs to decide how much coverage, specialist care, and out-of-network services you might require.

- Consider your budget: Determine how much you can afford and compare the different plans' required monthly premiums, deductibles, copayments, coinsurance, and other out-of-pocket costs.

- Determine your desired level of control: How much organizational support you need and how much freedom you prefer will impact which plan is right for you.

- Decide how much flexibility you need: If you can foresee yourself needing regular out-of-network or out-of-area care, you may benefit from choosing a plan with more flexibility.

- Read the fine print: While this guide can provide you with general guidelines, the exact benefits, costs, and provider approaches of each plan vary according to each unique insurance policy.

Frequently Asked Questions

If you're still on the fence about which plan is right for you, here are a couple of common questions about these health insurance options.

What Is Better: PPO or HMO Insurance?

The answer depends on your unique healthcare needs, lifestyle, budget, and preferences.

For example, if you frequently travel, foresee needing frequent specialist appointments, or prefer to seek out-of-network treatment, a PPO will suit you better than an HMO. However, if you are only seeking regular medical treatment to maintain your health, have a limited budget, or do not anticipate needing frequent specialist treatment, an HMO might be more suitable.

What Are the Cons of an HMO?

When compared to other traditional health insurance plans or a medical expense reimbursement plan (MERP), HMO plans can seem inflexible. While other plans might provide access to more extensive networks and seamless specialist treatment or reimburse your medical expenses, HMO plans operate within structured, small networks and require fixed monthly premiums.

Possible drawbacks of an HMO include:

- Limited network

- No external coverage, aside from emergency care

- No direct specialist access

- Fixed out-of-pocket costs

See the Savings With The Difference Card

When you use The Difference Card alongside or in place of a traditional insurance plan, you can see significant savings for yourself and your employees.

With our exclusive distribution strategy and customized plans, The Difference Card can be used as a stand-alone resource or in conjunction with an HMO, PPO, or EPO to guarantee you net savings at an average $2,000 per employee, per year.

Take your health insurance savings strategy to the next level. Request a proposal today or contact our expert team to find out more.