How Section 125 Plans Work

Table of Contents

- What Is a Section 125 Cafeteria Plan?

- How Do Section 125 Plans Enable Tax Savings?

- A Detailed Look at the Types of Section 125 Plans

- What Expenses Are Covered?

- Essential Compliance Rules for Employers

- A Step-by-Step Guide to Set up a Section 125 Plan

- Frequently Asked Questions

- Partner With The Difference Card to Administer Your Plan

As health insurance premiums rise, you're likely seeking options that offer substantial cost savings without reducing employee benefits. In 2025, the average annual health insurance premium was $9,325 for single coverage and $26,993 for family coverage, according to the KFF 2025 Employer Health Benefits Survey. This cost increases annually.

While it's a perk that enhances your competitive edge and employee satisfaction, it can strain your finances over time. A section 125 plan is a powerful solution when you feel the pinch. This guide covers everything you need to know about section 125 plans, from how they work and their tax-saving advantages to essential compliance rules and how to set one up for your employees.

Key Takeaways

- A section 125 plan lets employees buy benefits with pretax money. It lowers employees' taxable income and reduces employers' payroll taxes.

- Types of section 125 plans include POP, FSA, and DCAP.

- Strict IRS compliance rules apply, such as nondiscrimination testing and the "use-it-or-lose-it" rule.

What Is a Section 125 Cafeteria Plan?

Under the Internal Revenue Service code, a section 125 cafeteria plan is an employer-funded benefit program that allows employees to convert their taxable benefits, such as a portion of their salary, into qualified nontaxable expenses. These can include health insurance premiums, dental care, deductibles, doctor visits, or child care, paid with pretax dollars.

When employees make pretax deductions, their taxable income decreases. Your business will also benefit from lower tax obligations.

How Do Section 125 Plans Enable Tax Savings?

Beyond offering pretax benefits, section 125 plans provide financial relief through tax savings. Here's how you and your employees can save on costs.

For Employers

A section 125 plan creates tax savings for your business in two ways. First, it reduces your payroll taxes, such as the Federal Insurance Contributions Act. With a cafeteria plan, employees make contributions that are free from federal, Medicare, and Social Security taxes. You don't have to pay taxes on these contributions toward the plan.

Offering a section 125 plan can also reduce your turnover rate by boosting morale. Employees tend to stay longer with employers that offer sought-after perks. A more stable workforce keeps your Federal Unemployment Tax Act taxes down, because unemployment tax liabilities increase when turnover rises.

For Employees

Employees also enjoy cost savings with a section 125 plan, with gains like these.

- Immediate tax savings: Pretax contributions lower employees' taxable income.

- Reduced tax liability: Less money goes toward federal income tax, Social Security, and Medicare.

- Increased take-home pay: When employees pay for essentials like child care or copays before taxes, they end up saving more of their hard-earned money.

- Flexible benefit options: Employees can customize their benefits by choosing options to fit their needs.

A Detailed Look at the Types of Section 125 Plans

You can choose from various cafeteria plans to offer your employees, including the premium-only plan, flexible spending account, Dependent Care Assistance Program, and simple cafeteria plan. Here's what each option offers your employees.

Premium-Only Plan

A premium-only plan is the simplest section 125 option. It lets employees pay their share of employer-sponsored insurance premiums, such as medical, dental, vision, disability, and life, using pretax dollars. Because this plan only applies to premiums, employees cannot use the funds for any other expense.

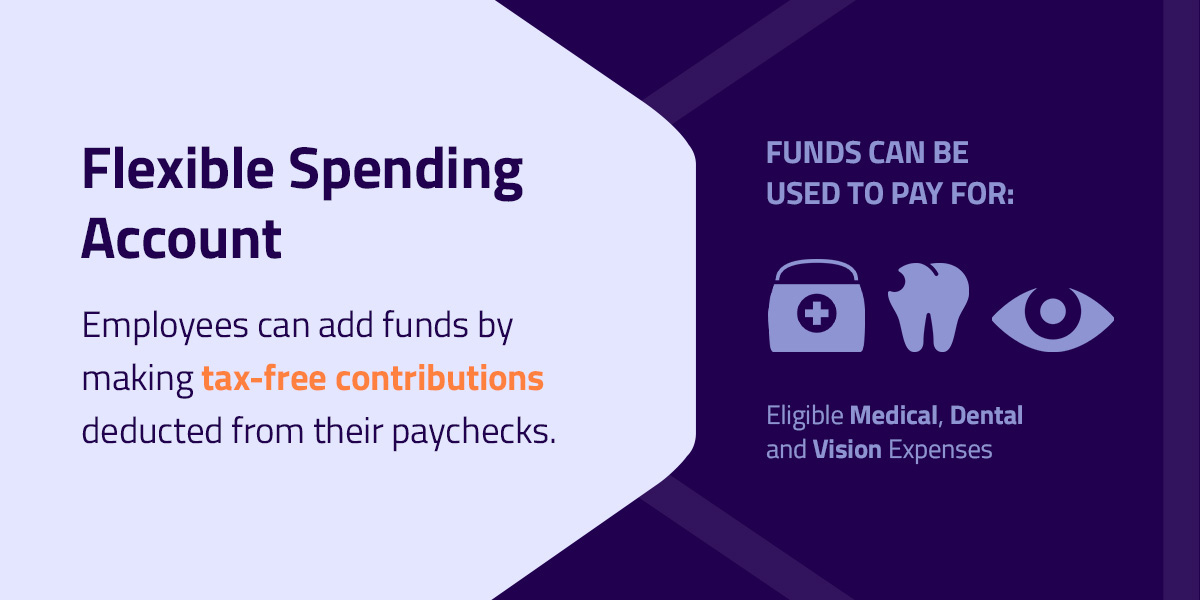

Flexible Spending Account

A flexible spending account is a tax-advantaged savings account. Employees can add funds by making tax-free contributions deducted from their paychecks. Then, they can use their FSA funds to pay for eligible medical, dental, and vision expenses, including doctor visits, eye exams, prescription medications, and mental health services.

Dependent Care Assistance Program

The Dependent Care Assistance Program is an excellent benefit for employees with children, eligible dependents, or elderly parents. It allows employees to use tax-free funds to pay for child or eldercare expenses.

An employee's federal filing status determines the maximum they can elect. They allocate that total across the plan year by dividing it by their pay periods, and the resulting amount comes out of each paycheck.

Simple Cafeteria Plan

You can implement a simple cafeteria plan if your business has 100 or fewer employees. This plan is an ideal choice for smaller businesses and lets you avoid costly annual nondiscrimination testing. However, you must fulfill IRS simple plan requirements to be eligible. Those include meeting the 100-employee limit, allowing employees with at least 1,000 hours of service for the plan year to participate, and contributing toward the plan on each employee's behalf.

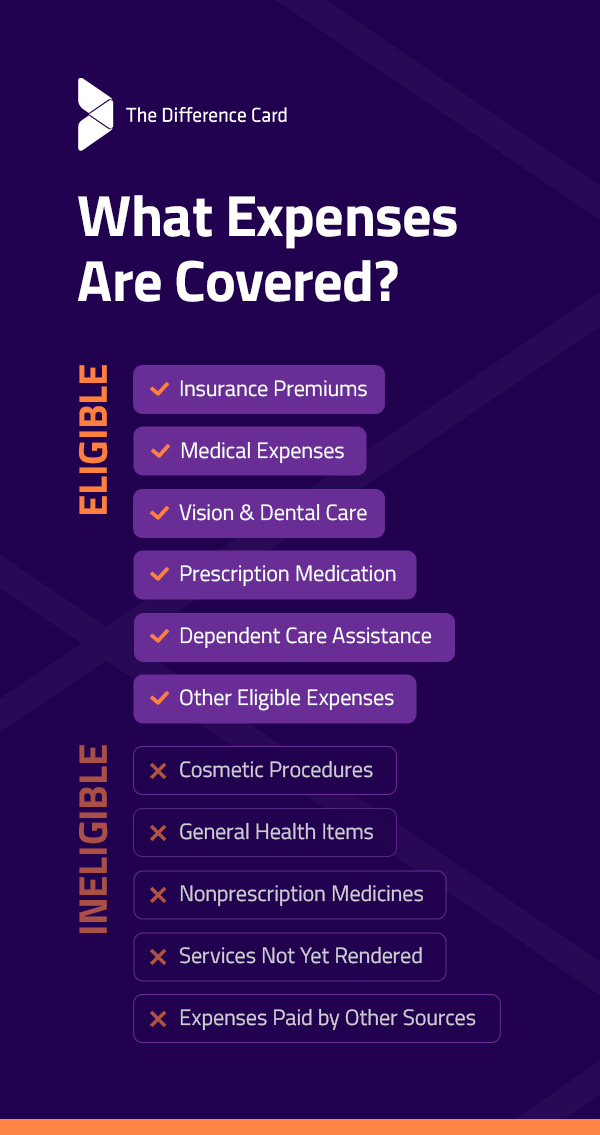

What Expenses Are Covered?

A section 125 plan covers specific, qualified expenses, including health benefits, group-term life insurance coverage and child care costs. Your employees, their spouses, and their dependents can use these benefits.

Eligible Expenses

Expenses covered by section 125 plans include the following.

- Insurance premiums: Includes medical, dental, vision, and disability coverage.

- Medical expenses: Health-related deductibles, coinsurance, copays, doctor visits, hospital bills, and laboratory fees.

- Vision and dental care: Dental procedures and prescribed eyewear, contact lenses, and laser eye surgery.

- Prescription medication: Qualified over-the-counter medicines require a doctor's prescription.

- Dependent care assistance: Expenses for care of a child under 13, or a dependent incapable of self-care, allowing the employee/spouse to work.

- Other eligible expenses: Qualified adoption assistance and HSA contributions.

Ineligible Expenses

Some medical procedures, medications, and other expenses are not eligible for reimbursement under the benefit plan.

- Cosmetic procedures: Treatments performed solely for aesthetic purposes, such as teeth whitening, liposuction, veneers, and dermal fillers.

- General health items: Includes toiletries and personal care products such as toothpaste, soap, shampoo, daily vitamins, supplements, and sunscreen.

- Nonprescription medicines: While some OTC items are eligible, many are not. Unless taken for a specific medical condition with a doctor's note, these items are out-of-pocket costs.

- Services not yet rendered: If employees prepay for services they won't receive until a future plan year, they can't claim those costs under the current plan. Only services actually provided during the plan year qualify.

- Expenses paid by other sources: If insurance or another party covers an expense, employees can't submit it. Doing so would amount to double recovery.

Essential Compliance Rules for Employers

To ensure compliance with your cafeteria plan, you must provide and maintain a written plan document and a summary plan description to your employees while also following strict IRS regulations. These include nondiscrimination, the “use-it-or-lose-it” rule, and qualifying life events your employees may experience. You must also give your employees the option to choose between cash compensation and pretax benefits.

The "Use-It-or-Lose-It" Rule Explained

The IRS’s “use-it-or-lose-it” rule states that if employees contribute to an FSA for health or dependent care, they must use all funds within the year, or risk forfeiting them.

Most section 125 plans follow this rule. However, there's usually a grace period to use the remaining funds before they expire. As an employer, you can also set a carryover provision to allow your employees to spend the money in the next year.

Benefit Changes for Qualifying Life Events

Once employees have chosen their benefits from the cafeteria plan menu, they typically can't change them until the next enrollment period. But if your employees experience a qualifying life event, they can adjust their benefit selection during a special enrollment period.

A QLE is a significant change in your employees' lives, such as:

- Marriage, divorce, or separation

- Birth or adoption of a child

- Involuntary coverage loss under an external plan

- Employment status changes

- Aged off a parent's plan

Understanding Nondiscrimination Testing

Employers must run annual nondiscrimination tests to prove that their plans don't favor owners or highly compensated employees. The IRS requires three tests — eligibility, benefits and contributions, and key‑employee concentration — to confirm the plan is fair to all participants.

- Eligibility: A fair share of employees can join the plan, not just management.

- Benefits: Contributions and benefits are equal for everyone. Highly compensated employees don't have access to additional nontaxable benefits.

- Key-employee concentration: Employees don't receive more than 25% of the total pretax benefits in the plan.

The IRS will audit the results of your nondiscrimination testing. Failing the test indicates that:

- The plan excludes a large portion of non-HCEs.

- HCEs receive more plan benefits than the rest of your team.

- Key employees account for more than 25% of the total plan benefits available.

A Step-by-Step Guide to Set up a Section 125 Plan

Are you ready to set up a cafeteria plan for your employees? Here's everything you need to do so.

1. Appoint a Plan Administrator

Decide whether you want to handle the setup in-house or use a third-party administrator for compliance and administration. If you choose the latter, your TPA will help you manage the plan, process reimbursements, and keep your business compliant.

2. Select Your Plan

Decide which plan best fits your company and your employees' needs.

3. Draft the Written Plan Document

The written plan is a mandatory document that details your plan's operation, eligibility, benefits, and plan year. If you don't complete this document, the IRS won't allow pretax deductions.

4. Create the Summary Plan Description

Inform eligible employees about the benefit options and their tax advantages and share the SPD with them. Include the following information.

- Plan overview: Clarify that this is a voluntary, pretax benefit program.

- Benefits offered: List included benefits — for example, medical, dental, or vision care, FSA, or POP.

- Tax savings: Explain that salary reductions for these pretax benefits are tax-free.

- "Use-it-or-lose-it" rule: Inform employees that they must use their FSA funds by the end of the plan year.

- Enrollment details: Provide deadlines, required forms, and enrollment instructions.

5. Configure Payroll Systems

Set up payroll to calculate and deduct employee contributions before applying taxes. Track these deductions and include them on your employees' paychecks for accountability.

6. Manage Ongoing Compliance

Monitor compliance by adhering to the "use-it-or-lose-it" rule for an FSA, offering a grace period for carryover, and conducting annual nondiscrimination testing.

Frequently Asked Questions

Do you still have questions about section 125 plans? We have answers for you! If you need further information, the IRS covers many other questions in detail.

What Does Section 125 Mean on an Employee's Paycheck?

If employees opt into a section 125 cafeteria plan, their paychecks will reflect pretax benefit contributions alongside their other payroll deductions.

Is Nondiscrimination Testing a Requirement?

Unless you have a simple cafeteria plan, you must conduct nondiscrimination testing annually to qualify for tax-favored status and ensure benefit fairness for all employees.

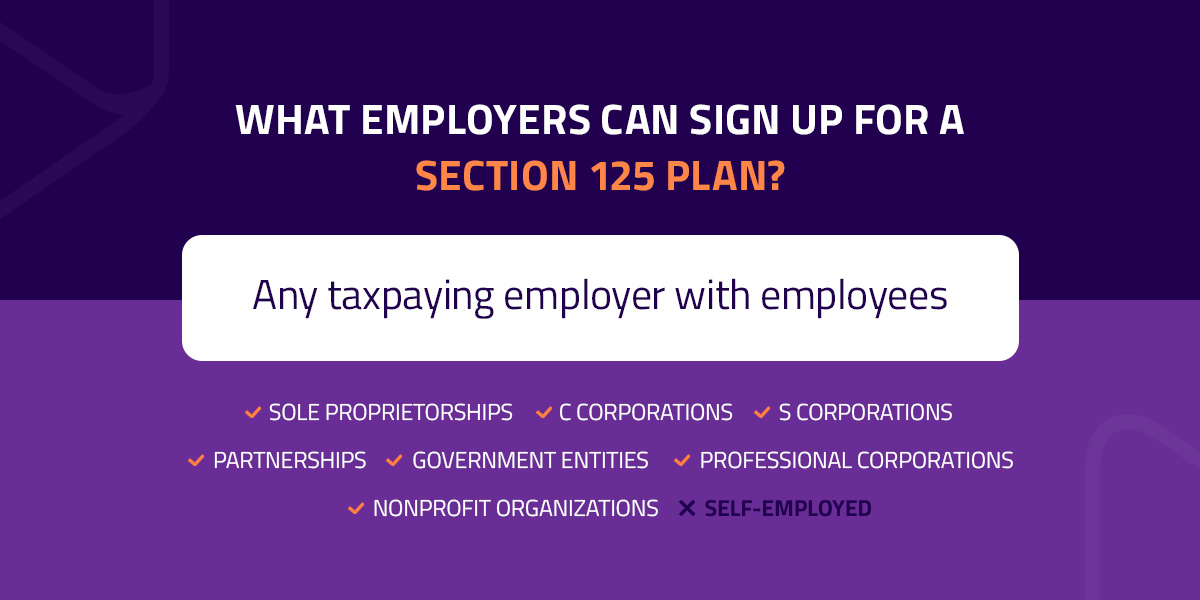

What Employers Can Sign up for a Section 125 Plan?

Almost any taxpaying employer with employees can establish a section 125 plan. While self-employed people are ineligible to sign up, this option is available to:

- Sole proprietorships

- C corporations

- S corporations

- Partnerships

- Government entities

- Professional corporations

- Nonprofit organizations

Can Employees Receive Cash Instead of Benefits?

Yes. However, you should inform them that this cash alternative will be taxable, unlike the pretax benefit option.

Partner With The Difference Card to Administer Your Plan

The Difference Card works to make health insurance more affordable for businesses. Since 2001, we’ve saved businesses $2.13 billion, with an average savings of 18% per employer group. We simplify the process so you can offer more comprehensive benefits without increasing your costs.

As part of our administration services, we'll assist you with setting up and managing section 125 plans. Our team prepares the required documents, ensures compliance, and recommends the cafeteria plan that best fits your workforce. We value long‑term partnerships and provide personal support to keep your business moving forward.

Learn more about our compliance services and request a proposal to get started.