What Is a Medical Expense Reimbursement Plan (MERP)?

Table of Contents

- How Does a MERP Work?

- Expenses Covered by a MERP

- Advantages of a MERP

- What Are the Different Types of MERP Products?

- How MERP Compares to the Alternatives

- Can a MERP Replace Health Insurance?

- MERP Compliance Requirements

- MERP FAQs

- How to Get the Most out of Your MERP

- Maximize Your MERP With The Difference Card

In 2024, the average annual premiums for employer-sponsored health insurance cost $8,951 for single coverage, a 6% rise from the previous year. For family coverage, this figure was $25,572, 7% higher than the previous year. This trend of rising medical costs looks set to continue into 2026.

Considering these price increases, it's not surprising that many employers have begun to explore alternative ways to cut costs without depriving their employees of essential healthcare.

A medical expense reimbursement plan is a solution many employers now choose. These lesser-known plans can serve employers and employees in their quest for affordable healthcare.

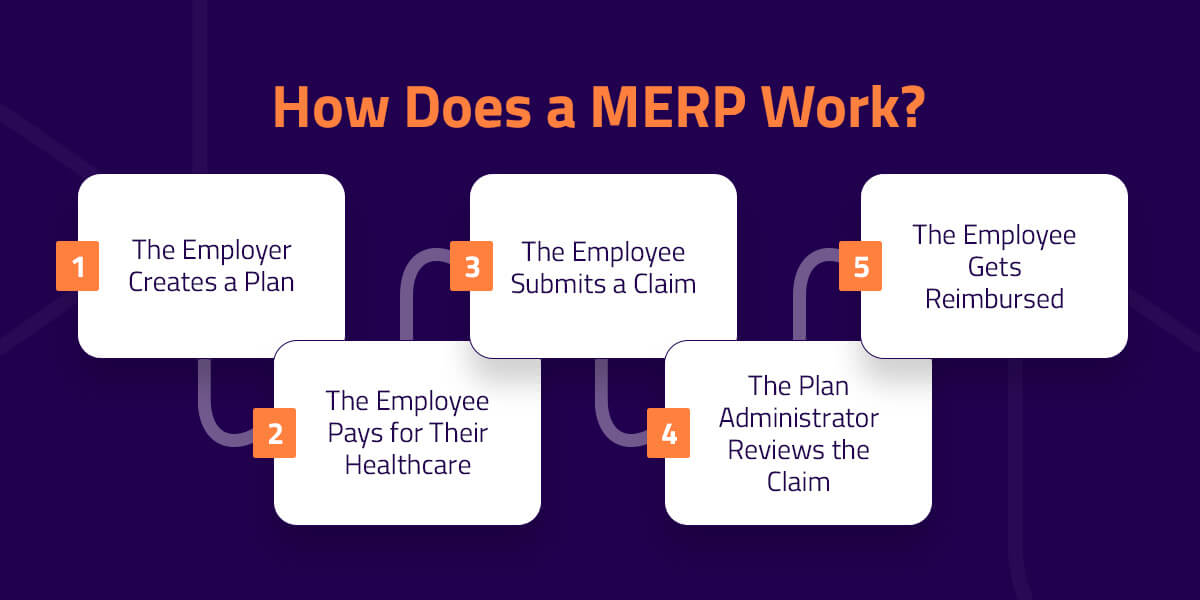

How Does a MERP Work?

A MERP is a benefit designed to help employers cover their employees' medical expenses. The employer sponsors, or contributes, toward it and decides which medical expenses qualify. They also decide how the reimbursement process will work based on their administrative capabilities.

MERP products follow a defined plan year. Unused contributions that don't roll over to the following year will revert to the employer, though some plans allow limited rollover.

1. The Employer Creates a Plan

The sponsor/employer sets covered expenses and monthly allowances for the MERP. In some cases, employees can roll their allowance, or maximum unused funds, from month to month or into the next plan year.

2. The Employee Pays for Their Healthcare

Employees pay upfront for eligible healthcare expenses, which may include various products or services depending on their plan. Some MERPs also allow reimbursement for personal health insurance premiums.

3. The Employee Submits a Claim

The employee then submits a claim for their medical expenses, accompanied by required documentation such as an invoice or receipt. Along with this, the employee must describe the reason for the expense.

4. The Plan Administrator Reviews the Claim

The plan administrator reviews each claim to confirm the expense qualifies and the employee has enough allowance for reimbursement. They may also request required documentation and additional details if needed.

5. The Employee Gets Reimbursed

The employee receives payment for their approved medical expense.

Expenses Covered by a MERP

Flexibility is a noteworthy benefit of a MERP. Employers can tailor the product to meet changing needs. MERPs can defray the costs of various eligible healthcare expenses, including:

- Doctor visits and hospital appointments

- Surgeries

- Prescription medications

- Mental health counseling

- Physical therapy

- Diagnostic tests like X-rays and MRI scans

- Vaccinations and other preventive care services

- First-aid supplies

Does a MERP Cover Dental and Vision?

While not all medical expense reimbursement plans include dental and vision expenses, some MERPs offset these out-of-pocket costs if they are not part of standard medical insurance.

Advantages of a MERP

MERP products offer many benefits for employers and employees.

Employer Benefits

Companies that sponsor MERPs can enjoy several financial and strategic advantages. Contributions are often tax-deductible and typically exempt from Social Security, unemployment and payroll taxes.

Employers also control which expenses their plan covers and set contribution limits, making it easier to manage costs and forecast spending. As a meaningful employee perk, a well-designed MERP can boost recruitment and retention. When employees can access timely care, businesses get a healthier, more productive workforce with higher morale and top talent.

Employee Benefits

MERPs reimburse eligible expenses to help employees afford medical care, even if they must initially pay out of pocket. Most plans cover essential preventive care like annual checkups, while some offer broader coverage.

Reimbursements are tax-deductible if the plan follows IRS Section 213(d) guidelines, offering additional savings. Above all, MERPs provide peace of mind, reducing financial stress when unexpected medical bills arise.

What Are the Different Types of MERP Products?

A MERP is one type of health reimbursement arrangement, but there are also different categories of MERP products. Here are some of the most popular.

Group Coverage HRA

A group coverage health reimbursement arrangement — also called an integrated, deductible or traditional HRA — pairs a MERP with a group health plan, often one with a high deductible that lowers premiums compared to standard group coverage.

Employers commonly raise the deductible on the group plan and use the MERP to reimburse employees for the difference. This strategy reduces premium costs, allows for tax-deductible reimbursements and maintains full medical coverage for employees.

Stand-Alone MERP and Qualified Small Employer HRA

A stand-alone MERP replaces a group health plan instead of supplementing it. Employers reimburse employees for their health insurance policies, avoiding the need to define covered expenses or manage rising group insurance costs.

A stand-alone MERP frees employees to shop around for a policy that perfectly suits them instead of signing up for a group policy that may not meet all their medical needs.

A qualified small employer HRA is a stand-alone MERP specifically designed for employers with fewer than 50 full-time equivalent employees. It can reimburse employees for their insurance premiums, plus health services and products not covered by their insurance policy.

Individual Coverage HRA

An individual coverage HRA is a MERP that lets employers offer different health plans to separate employee groups. Employers can define these based on factors like full-time vs. part-time status or remote vs. on-site roles.

Unlike most MERPs, which must be uniform, an ICHRA allows employers to provide group coverage to one class of employees and individual coverage to another. The IRS outlines 11 distinct employee classes to guide this flexibility.

- Full-time employees: Employers decide whether to classify “full time” as 30 or 40 hours per week.

- Part-time employees: Work fewer hours than the defined full-time threshold.

- Seasonal/temporary employees: Employees hired on a set short-term contract.

- Temporary employees of staffing companies: Temporary staff formally employed by a hiring agency rather than the company.

- Salaried employees: Receive a fixed wage, paid no more frequently than weekly.

- Hourly employees: Paid based on hours worked at a set rate.

- Employees under a collective bargaining agreement: Covered by a CBA negotiated by a trade union.

- Employees in a waiting period: Must wait up to 90 days before becoming eligible for health benefits.

- Foreign employees who work abroad: Employees who work in another country and don't hold U.S. residency.

- Employees working in different geographical locations: Grouped by geographic region, such as state or insurance rating area.

- A combination of the above classes: Employers can define overlapping employee classes by combining factors like job type and location. For example, they might create one class for full-time employees in New York and another for full-time employees in California.

Each defined class can receive different health benefits — such as group coverage for one and an ICHRA for another. However, all employees within the same class must have identical options. Employers can’t mix and match benefits within a single class.

Excepted Benefit HRA

An excepted benefit HRA, commonly known as an EBHRA, is a MERP specifically designed to reimburse employees for expenses not covered by a traditional health plan. These “excepted benefits,” as defined by the Affordable Care Act, typically include:

- Dental and vision insurance premiums

- Cancer insurance premiums

- Accident-only coverage

- Long-term benefits

- Short-term limited-duration insurance

- Limited health benefits

- Specific disease or illness coverage

How MERP Compares to the Alternatives

Employers can give their employees access to healthcare through a MERP, but other accounts can help workers get the coverage they deserve.

MERP vs. HRA

A MERP is a more flexible type of HRA. While all HRA plans help employees receive access healthcare, a MERP gives employers more freedom to decide how to do this.

MERP vs. HSA

A health savings account, or HSA, is similar to a MERP because it allows people to set aside pre-tax dollars to pay for medical expenses. Unlike MERPs, which are solely employer-funded, employees can contribute an annual maximum to their HSAs. Additionally, an employee owns their HSA, which means they can keep it even if they leave the company.

MERP vs. FSA

Like an HSA, a flexible spending account involves pre-tax money funded by the employer or employee. While some FSA plans don’t allow unused funds to roll over, many offer a grace period or limited rollover by dollar amount.

FSAs differ from other spending accounts in one notable way — employees can pay for health expenses before depositing money, making them more flexible in timing. The employer also owns the FSA, and an employee cannot take it with them if they leave.

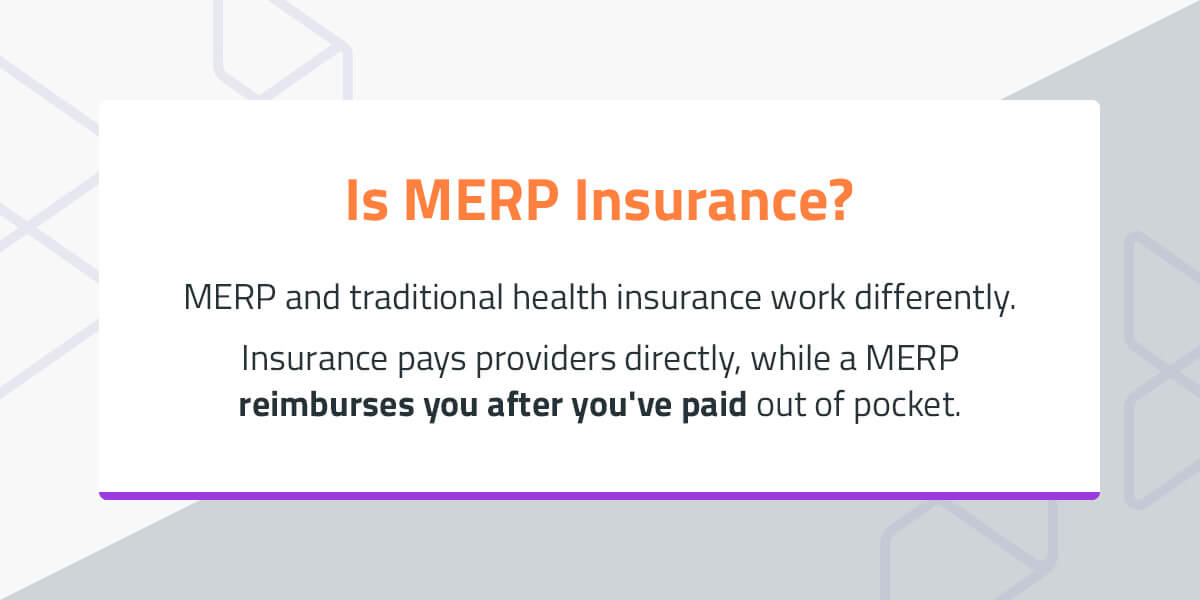

Can a MERP Replace Health Insurance?

Depending on your business, you can use a MERP to replace or complement a health insurance policy, such as with a GCHRA. The distinction between a MERP and health insurance is that an insurance policy will pay the medical expense for you, whereas a MERP will reimburse you after you've fronted the cost out of pocket.

While a MERP is employer-sponsored, either the employee or employee can pay the insurance policy's premiums and deductibles.

MERP Compliance Requirements

For a MERP to be legal, it must comply with several standards to protect anyone who purchases it.

- IRS Section 105: In the Internal Revenue Code, section 105 outlines which expenses can be tax-deductible, and requires the MERP administrator to ensure the plan doesn't favor higher-income employees over lower-income employees.

- Affordable Care Act: ACA details the minimum care standards that group health plans must meet.

- Employee Retirement Income Security Act: ERISA requires all MERP products of a specific size to meet reporting and disclosure requirements. These requirements include filing an annual report with the Department of Labor and providing an SPD and an SBC.

- Health Insurance Portability and Accountability Act: MERP administrators must secure employees' protected health information to meet HIPAA requirements.

- Consolidated Omnibus Budget Reconciliation Act: This act allows employees to receive temporary coverage after losing their medical benefits following qualifying events. COBRA rules apply to MERPs paired with group health plans that are subject to COBRA. If an employee loses their coverage, they may have the right to continue receiving benefits under COBRA.

MERP FAQs

Since MERPs aren't as well-known as traditional health insurance, many people don't fully understand how they work. Here are answers to some of the most common questions about MERP products.

Is MERP Insurance?

Many people mistake a MERP for traditional health insurance, but they work differently. Insurance pays providers directly, while a MERP reimburses you after you've paid for eligible medical expenses out of pocket.

Are MERP Products Only for Large Businesses?

Though large businesses can benefit from a MERP, these products can be particularly appealing to small businesses by giving them the flexibility they need to create the best healthcare solution for their employees. A MERP can also help small businesses save on their taxes.

What Are the Disadvantages of MERP Products?

MERPs aren't perfect for every employer due to potential drawbacks and limitations. However, your company can avoid or limit most of these disadvantages by working with a third party who's familiar with the product.

- Compliance: MERPs must meet legal standards and regulations, which can be administratively demanding.

- Upfront expenses: Employees must initially pay for their medical expenses themselves, which some people will balk at.

- Review demands: Reviewing and processing employee claims can take time and resources.

- Product misunderstanding: Because MERPs are less familiar than traditional health insurance, employers and employees often confuse the two. This uncertainty can lead to miscommunications, unrealistic expectations and missed opportunities to use the MERP effectively.

Are MERP Reimbursements Taxable Income?

Employees who meet all these conditions can exclude these reimbursements from their taxable income:

- The reimbursements are for a medical expense listed under IRS Section 213(d).

- The employee can provide proper documentation.

- The MERP complies with IRS Section 105.

How to Get the Most out of Your MERP

MERP products can slash your healthcare costs while providing employees with access to all the medical expertise they need. But you shouldn't switch to a MERP without knowing how to optimize it for everyone in your company.

-

- Customize the plan: MERP products are highly flexible, so you can adjust them to your needs. Review your team's past medical expenses and use this to decide appropriate reimbursement limits.

- Consider different plans for different classes: Since not all employees need the same coverage, you could save money if you split them by class.

- Understand the product: If you understand how your MERP works, you can take full advantage of it and avoid costly mistakes.

- Adjust your MERP: Business and employee needs evolve, so regularly review your MERP to ensure it still fits. It may be time to adjust the plan if it no longer aligns with your goals.

- Use integrated debit cards: If the MERP supports integrated debit cards, employees won't have to pay for the expenses out of pocket. Instead, they can swipe a card to streamline the process.

Maximize Your MERP With The Difference Card

- As healthcare costs rise nationwide, it's increasingly challenging for employers to stay within budget without removing employee benefits. A MERP offers a superior solution, especially when you partner with The Difference Card.With over 20 years of experience and strong relationships with insurance brokers from coast to coast, we help businesses design custom healthcare plans that save money without sacrificing coverage. Our clients reduce health benefit costs by an average of 18%, and employees appreciate that we process 99% of claims in two days or less.Discover what The Difference Card can do for your team and bottom line. Contact us today to start building a more cost-effective, employee-friendly benefits plan.