Stop-Loss Insurance for Brokers: Specific vs. Aggregate, Lasers, and Corridors

Table of Contents

- What Is Stop-Loss Insurance?

- What Are the Stop-Loss Insurance Types?

- Pitching Specific vs. Aggregate Stop-Loss

- Level-Funded vs. Self-Funded: Key Differences

- Advanced Medical Stop-Loss Strategies

- How Brokers Can Deliver Stop-Loss With Confidence

- 10 Broker Stop-Loss Insurance FAQs

- How The Difference Card Can Boost Your Stop-Loss Strategy

Employers have a responsibility to find the most valuable health benefits for their employees. However, it is easy to overlook the considerable impact that medical expenses have on businesses. Confidently explaining why stop-loss insurance is a viable option to help employers manage associated costs is essential.

This guide focuses on the basics and advanced knowledge every broker needs to know about stop-loss insurance. From the differences between specific and aggregate to advanced medical stop-loss strategies and frequently asked questions, our guide provides what you need to know.

What Is Stop-Loss Insurance?

Stop-loss or excess insurance is a type of insurance that enables employers to self-fund employee health benefits. Employers purchase stop-loss coverage to protect against high medical expenses.

However, the employer is not fully liable for losses resulting from the self-funded plan. Once claims exceed a set limit, the insurance company covers the excess.

What Are the Stop-Loss Insurance Types?

Two options of stop-loss insurance are available — specific and aggregate. With each type, employers should consider the particular requirements and impacts on their businesses:

Specific Stop-Loss

Also called individual stop-loss insurance, this insurance protects employers against high claims involving a single employee. Specific stop-loss insurance is for high-cost individual claims, not frequency.

Aggregate Stop-Loss

Aggregate stop-loss limits eligible expenses that employees can claim during their contract period. Once a contract is complete, the insurance provider reimburses employers for any aggregate claims.

Pitching Specific vs. Aggregate Stop-Loss

Understanding stop-loss insurance is the first step. Confidently pitch stop-loss by focusing on each client's risk profile and financial objectives. Here are the key points to address for specific vs. aggregate stop-loss:

Specific Stop-Loss

If an employee's claim exceeds the employer's contribution limit for the year, the insurance company reimburses the difference to the employer:

- Primary focus: Specific stop-loss insurance is suitable for employees who have a single, high-cost claim that requires a large deductible. For example, the claim may be for cancer treatment or surgery.

- Attachment point: The attachment point is the claim threshold where stop-loss insurance begins to pay. For specific stop-loss coverage, this point is set based on claims history and risk tolerance.

- Employer payment: Under a specific stop-loss, the employer makes an up front payment, up to the deductible. The insurance carrier covers any amount above that.

- Typical clients: A specific stop-loss client is often a small or medium-sized enterprise (SME) with limited cash reserves. Another typical client is a business with sporadic insurance claim activity and occasional spikes in claims from employees.

- Key considerations: With the specific stop-loss, employers have lower specific deductibles with increasing premiums but more overall protection. However, with higher deductibles, employers can expect lower premiums.

Aggregate Stop-Loss

Aggregate coverage protects an employer if the total amount of all claims from employees surpasses a predetermined total:

- Primary focus: Aggregate stop-loss insurance protects against excessive utilization. The insurance provides a safety net for employers when claims exceed contribution limits.

- Attachment point: This is the amount the employer must pay toward medical expenses and is typically set as a percentage of the expected claims amount. The insurance provider will reimburse expenses over the attachment point.

- Employer payment: Assessment for reimbursement occurs once an employee's policy ends. The total claim costs are assessed against the attachment point.

- Typical clients: The typical aggregate stop-loss clients are bigger companies with a large number of employees. Other typical clients may include employers that prefer to set a total annual limit on employee healthcare costs.

- Key considerations: Aggregate insurance is generally more cost-effective and allows employers to set limits and pay only their set contributions.

Level-Funded vs. Self-Funded: Key Differences

Level-funded and self-funded health insurance involve employer financial responsibility, but they are different. Understanding these differences helps you recommend the best solution for your clients. Here's what you need to know:

Self-Funded Plans

For companies that want complete control, self-funded plans allow employers to manage risk and claim payments more closely:

- When an employee incurs medical expenses, the employer pays the claim instead of making premium monthly payments.

- Employers purchase aggregate and specific stop-loss insurance policies separately.

- Employers are also liable for claim amounts up to the agreed attachment point.

- Employers can customize specific elements, such as lasers and corridors, to manage an employer's risk tolerance.

- Self-funded plans are more flexible. However, the monthly costs may vary.

Level-Funded Plans

With level-funded plans, employers have a combination of predictable monthly costs with the same features as self-funded plans:

- Employers pay a fixed amount each month, which covers premiums, administrative fees, and estimated claims.

- Specific or aggregate stop-loss insurance coverage is a component within a level-funded plan to help manage risk.

- An insurance provider reimburses employers for claims over the attachment points. Reimbursement offers protection for employers to sustain significant losses.

- Employers may receive unused funds at the end of the plan year.

- Level-funded plans help employers navigate stop-loss insurance and assist with budgeting.

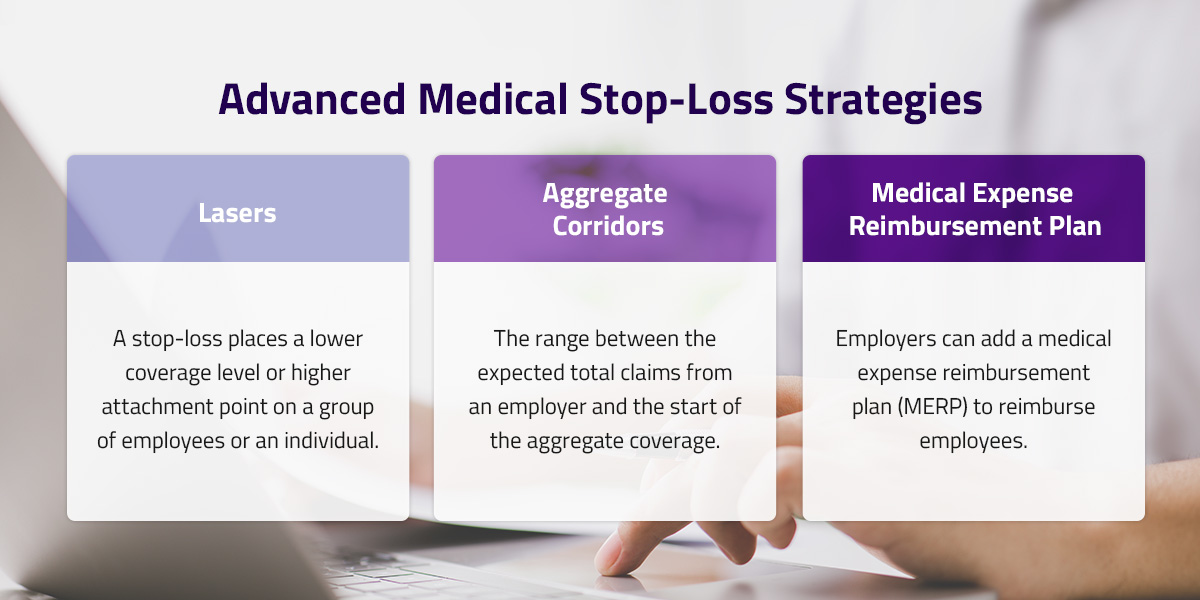

Advanced Medical Stop-Loss Strategies

Going beyond the basics and understanding specific advanced strategies provides a better experience. Advanced methods deliver benefits, including lower premiums and improved plan predictability.

Explaining advanced strategies helps clients make informed decisions:

Lasers

A stop-loss laser places a lower coverage level or higher attachment point on a group of employees or an individual. A stop-loss laser recipient often has a chronic health condition, such as cancer or heart disease.

Individuals with chronic health conditions tend to have higher medical costs, so an employee with a laser policy will likely have a higher deductible. Employers must be able to pay for medical expenses before stop-loss reimbursement starts.

Stop-loss laser insurance offers a comprehensive level of coverage while the provider manages its risk.

Aggregate Corridors

An aggregate corridor is the range between the expected total claims from an employer and the start of the aggregate coverage. For example, with expected claims of $1 million annually and a 125% set corridor, the employer must take responsibility for $1.25 million of claims.

In this example, the 0.25 difference carries some risk to the employer because the total claims exceed the expected figure. Aggregate corridors enable insurers to maintain balanced premiums and effectively manage overall risk.

With employers covering costs up to the corridor limit, an insurance provider is protected against smaller and more regular claims. Widening or narrowing a corridor affects premium prices — the more risk the employer shoulders, the lower their stop-loss premium will be. As a broker, advise clients on selecting the right coverage for their needs.

Medical Expense Reimbursement Plan

Employers looking to lower their stop-loss premiums can choose a high-deductible health plan (HDHP) to take on more risk and raise the stop-loss attachment point. To offset the higher deductible for employees, employers can add a medical expense reimbursement plan (MERP) to reimburse employees for their out-of-pocket medical expenses.

While a MERP does not directly affect a stop-loss insurance policy, it can allow employers to reduce their stop-loss insurance costs while keeping health care costs manageable for employees.

How Brokers Can Deliver Stop-Loss With Confidence

The process of stop-loss insurance may appear difficult to understand. However, the purpose of stop-loss is to ensure that employers receive manageable self-funded and level-funded plans. An easy-to-understand pitch helps employers feel comfortable with stop-loss insurance:

- Stop-loss employer protection: By implementing stop-loss insurance, employee benefits remain unchanged. Therefore, the process of reimbursing employees for medical expenses stays the same. Stop-loss effectively protects employer budgets.

- Aggregate and specific risks: Highlight the differences between specific and aggregate stop-loss policies to ensure employers have the correct coverage. Aggregate stop-loss supports a yearly cap to manage the volume of claims. Specific stop-loss safeguards against high, unexpected claims.

- Key underwriting tools: Providers can incorporate underwriting tools, including attachment points and lasers, to help identify and mitigate potential risks. With clear and straightforward explanations, employers can make informed decisions to support their business.

- Plan reliance on stop-loss: Both level-funded and self-funded health plans rely on stop-loss insurance in various ways. For example, level-funded plans offer employers predictable monthly costs, while self-funded plans deliver more flexibility.

- Breaking down the jargon: Understanding how stop-loss insurance works and finding the ability to explain it in plain language brings confidence to employers about self-funding. Delivering simple and effective explanations builds trust with clients.

If you discuss the benefits of stop-loss insurance with employer clients, be sure to keep jargon to a minimum. Your goal is to demonstrate how stop-loss is essential for protecting medical expense budgets and offers peace of mind.

10 Broker Stop-Loss Insurance FAQs

For extra clarification, the following is a list of 10 frequently asked questions to fill in any gaps:

How Is Medical Stop-Loss Insurance Different From Traditional Reinsurance?

Self-funded employers buy stop-loss insurance to protect themselves against significant claims. With medical stop-loss insurance, employers are responsible for paying employee health claims to a certain limit, after which the stop-loss insurance reimburses them for extra costs.

Insurance providers purchase traditional reinsurance coverage to manage their own risk and protect themselves against losses from the policies they sell.

What Is a Typical Attachment Point?

There is no typical attachment point for all employers. Attachment points vary based on different factors unique to each company, such as the company's risk tolerance and claims history.

Many SME companies set attachment points of up to hundreds of thousands of dollars. An aggregate attachment point is typically 125% of potential claims across the plan year.

Is It Essential for Employers to Have Specific and Aggregate Coverage?

Neither coverage is required. However, employers have more protection with both plans since one covers expenses for high-risk individuals and the other covers claims in a plan year.

Can Employers Self-Fund Claims Without Stop-Loss Insurance?

An employer can self-fund medical claims without purchasing stop-loss coverage. Stop-loss insurance protects employers in the event of high-cost expenses and catastrophic events.

Are There Tax Advantages With Stop-Loss Insurance?

The IRS allows employers with self-funded health plans to pay qualified medical claims with pretax dollars, but adding stop-loss insurance does not provide any additional tax advantages.

Do Stop-Loss and Health Insurance Share the Same Regulations?

Under federal law, health insurance and stop-loss insurance are subject to different regulations. Stop-loss insurance reduces employers' financial risk and is lightly regulated to prevent misuse.

Health insurance covers employees' healthcare. A self-funded health plan is subject to Employee Retirement Income Security Act (ERISA) regulations.

Does Offering an HDHP Limit the Need for Stop-Loss Coverage?

No. A high-deductible health plan (HDHP) may lower the amount of claims, as some up front costs are the employees' responsibility. However, stop-loss insurance protects employers from large claim volumes and high-cost claims.

Can Stop-Loss Insurance Allow Funds to Roll Over?

Roll over of unused claim funds does not apply to stop-loss insurance. A stop-loss policy is only applicable to medical claims within the plan year. However, some level-funded and self-funded plans may allow funds to roll over to the following year.

Is Stop-Loss Insurance Suitable for All Business Sizes?

Small and large businesses can all benefit from stop-loss insurance, but the impact is different depending on employer size:

- Small employers: Having stop-loss insurance is more beneficial for small employers, as it helps maintain budgets and mitigates high medical claims.

- Large employers: Smaller claims are more manageable for larger employers, but stop-loss insurance protects against catastrophic claims and stabilizes risk.

Are Stop-Loss Insurance Policies Customizable for Employers?

Yes, stop-loss insurance coverage is customizable. Brokers work closely with providers to build tailored solutions for employers. Depending on factors such as lasers and high deductibles, stop-loss coverage premiums can fit comfortably within an employer's budget.

How The Difference Card Can Boost Your Stop-Loss Strategy

Understanding stop-loss insurance helps you provide the best solution for your clients. At The Difference Card, our innovative product allows your clients to provide the necessary coverage and balance their business needs.

Our experienced professionals help you develop strategies tailored to your clients' goals. Implementing MERP options and other solutions helps employers manage their budgets more effectively by utilizing higher deductibles and limiting the impact of laser costs.

Ready to learn how The Difference Card can benefit employers and support brokers? Contact our team today and request a proposal for your clients.