What Is PEO Insurance?

Table of Contents

A professional employer organization (PEO) offers health insurance, among other benefits. Many small- to medium-sized businesses work with one. However, you can often get better coverage, flexibility, and cost savings if you work with a medical expense reimbursement plan (MERP). PEO contracts come with strings attached that limit your flexibility regarding coverage.

Before making a decision, you'll first want to learn what PEO insurance is and how it works. Comparing PEO pros and cons can also help you determine if one fits your business. It's difficult to opt out of a PEO, so you should navigate your options thoroughly.

What Is a PEO and the Co-Employment Model?

A PEO provides comprehensive HR solutions for businesses. Apart from offering health benefits, it can offer administrative services. It uses a co-employment model, meaning you share employer responsibilities. While the PEO handles HR tasks, you manage the daily business operations.

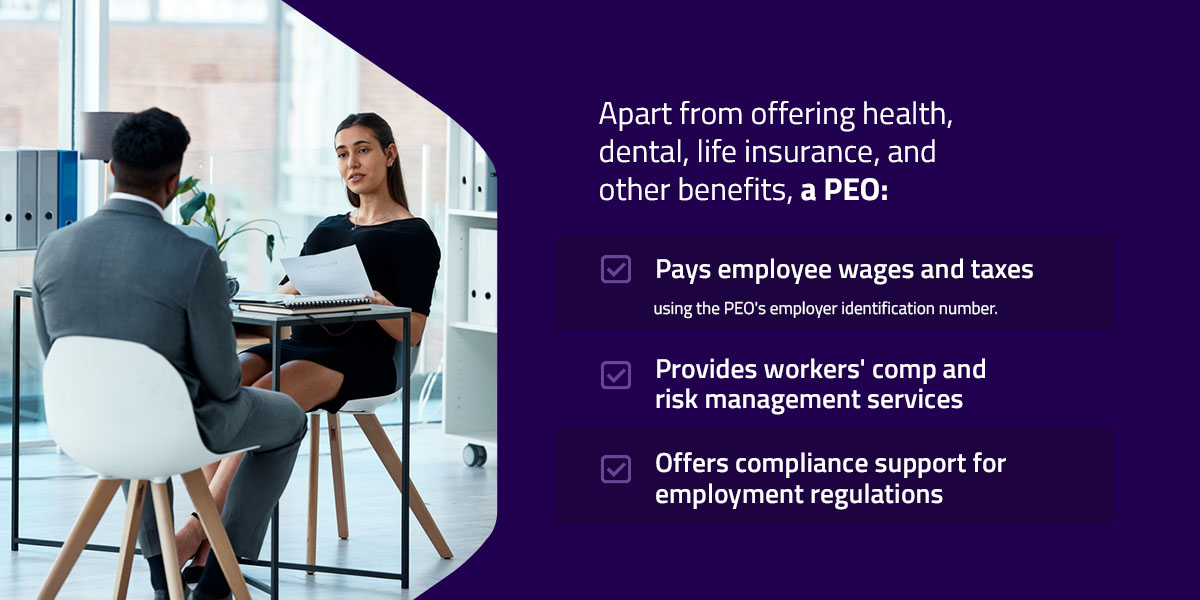

However, PEO services are usually bundled. You can't solely opt for healthcare benefits if that's the only thing you need. Apart from offering health, dental, life insurance, and other benefits, a PEO:

- Pays employee wages and taxes using the PEO's employer identification number.

- Provides workers' comp and risk management services.

- Offers compliance support for employment regulations.

A PEO is often confused with an employee leasing company. However, unlike employee leasing, a PEO doesn't provide your company with a workforce. It only helps you with HR-related tasks. Employment decisions still fall on you.

Your company maintains responsibility for production, product development, marketing, sales, job assignments, employee assessments, and other business operations. You also dictate the employee schedules, pay rates, and their benefits eligibility.

How PEO Insurance Works

Because a PEO has co-employment agreements with multiple companies, it has a larger pool of employees on paper. This gives them bargaining power, letting them access competitive rates from insurers. Small businesses can benefit from this, as it can be challenging to negotiate for lower rates themselves. Large businesses can take advantage of competitive rates while gaining access to HR platforms and professionals.

Once a PEO approves you for their policy, they manage the enrollment, claims processing, and compliance-related tasks. Some PEO platforms unify employee information and streamline workflow. However, if you leave a PEO, employees also lose their insurance coverage. You'd need to have an exit strategy and a replacement coverage ready.

PEO Benefits

Some of the main advantages of a PEO include:

- Competitive rates: A larger pool of employees results in lower risks for insurers. A PEO can negotiate better rates.

- Simplified administration: A PEO manages the benefits, alongside other HR tasks, so you won't need to communicate with insurers. You can focus on your business operations instead.

- Sophisticated technology: A PEO can use sophisticated HR software that tracks applicants and employees. Small companies can take advantage of this technology if they don't have their own.

- Compliance support: Compliance support is often a bundled service. A PEO stays up to date with the latest federal, state, and local laws, which can provide guidance on healthcare and employment regulations. This support can be beneficial for large businesses operating in multiple locations.

PEO Considerations

While the benefits can be enticing, the potential drawbacks of a PEO can be a deciding factor for companies:

- Complex setup: The co-employment arrangement is complex, especially for smaller businesses. It can even be unnecessary. Some companies also dislike third parties impacting employer-employee relationships.

- Unresolved issues: Even if a PEO offers comprehensive HR solutions, it doesn't always solve your business challenges. Problems can still arise, especially in communication and customer support.

- Limited control and flexibility: You'll lose control of your employees' healthcare benefits. You can't ensure the PEO's plan meets your workforce's needs. If the PEO switches policies, you must adapt. Your employees must get accustomed to the new plan, even if they'd already settled into the previous one.

- Potential coverage rejections: A PEO isn't an insurance company and can reject employees for coverage. Minimum qualifications help control costs. The PEO may also require a minimum number of participants, which can disqualify small businesses. It can even limit or reject participants with many claims from the previous year. Consequently, they may deny certain industries, such as construction or food service sectors, due to perceived healthcare usage patterns.

- Hidden fees: PEO contracts lack transparency. They often bundle insurance costs with administrative markups, such as fees for background checks, onboarding, compliance consultations, or software use. These fees may be hidden in the fine print of a lengthy contract. Without clear pricing, you may unknowingly and unnecessarily overspend.

- Restricted data access: The PEO controls the HR systems, so it owns the data. You may have limited access to this data. You may even need approval to modify time policies or perform routine changes. Once you leave the PEO, you also lose access to the claims data, which makes future renewals challenging.

- Hard to leave: Apart from losing historical data, leaving a PEO can be difficult. You need to replace all services in the PEO's bundle. Leaving can also result in paying employment taxes twice. For instance, if you leave the PEO mid-year, then your employees will receive two W-2 Forms — one from you and another from the PEO.

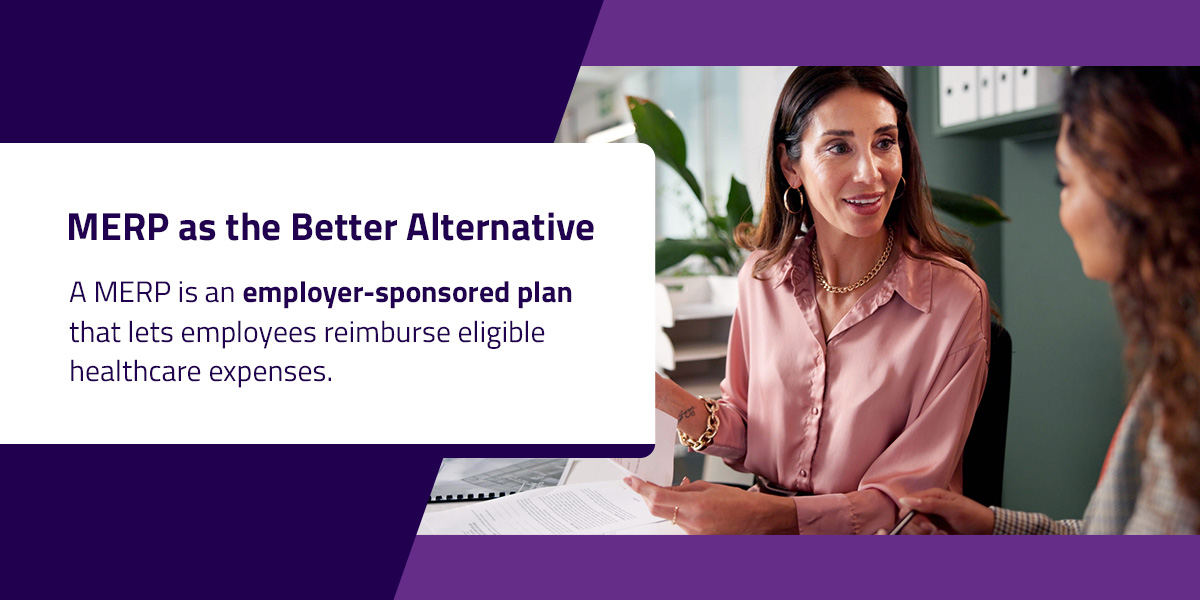

MERP as the Better Alternative

The considerations of PEO health insurance can be a deal breaker. Co-employment may also not make sense for your business structure. If you're looking to offer healthcare benefits with competitive rates, a MERP can be a suitable alternative. It's not considered a standard benefits offering, but it can help you reduce healthcare costs, increase tax savings, and provide benefits tailored to your employees' needs.

A MERP is an employer-sponsored plan that lets employees reimburse eligible healthcare expenses. These can include out-of-pocket costs and premiums. Employees can typically reimburse payments for doctor's visits, prescription medications, and hospital services. You can establish the eligible expenses and the reimbursement process.

You're free to design the plan according to your budget by setting the contribution limits. The plan can complement or replace your health insurance policy depending on the design. This reimbursement structure ensures you only spend on what employees actually need. Unused funds can also roll over to the following year.

Compared to a PEO, a MERP offers significant flexibility. You're not tied to a co-employment relationship, making it easier to make administrative and health benefit changes. MERP contributions are also often tax-deductible and exempt from Social Security, payroll, and unemployment taxes. You only need to comply with relevant standards to maintain the plan's tax-advantaged status. Administrators, like The Difference Card, can offer the compliance support you need.

Also, with a MERP, you can work with your trusted broker to help shop around for an insurance policy. This broker represents your interests. With their wide network of insurers, brokers can help you find the best policy for your employees. Since they're licensed and regulated, their guidance can be beneficial compared to simply taking what the PEO offers.

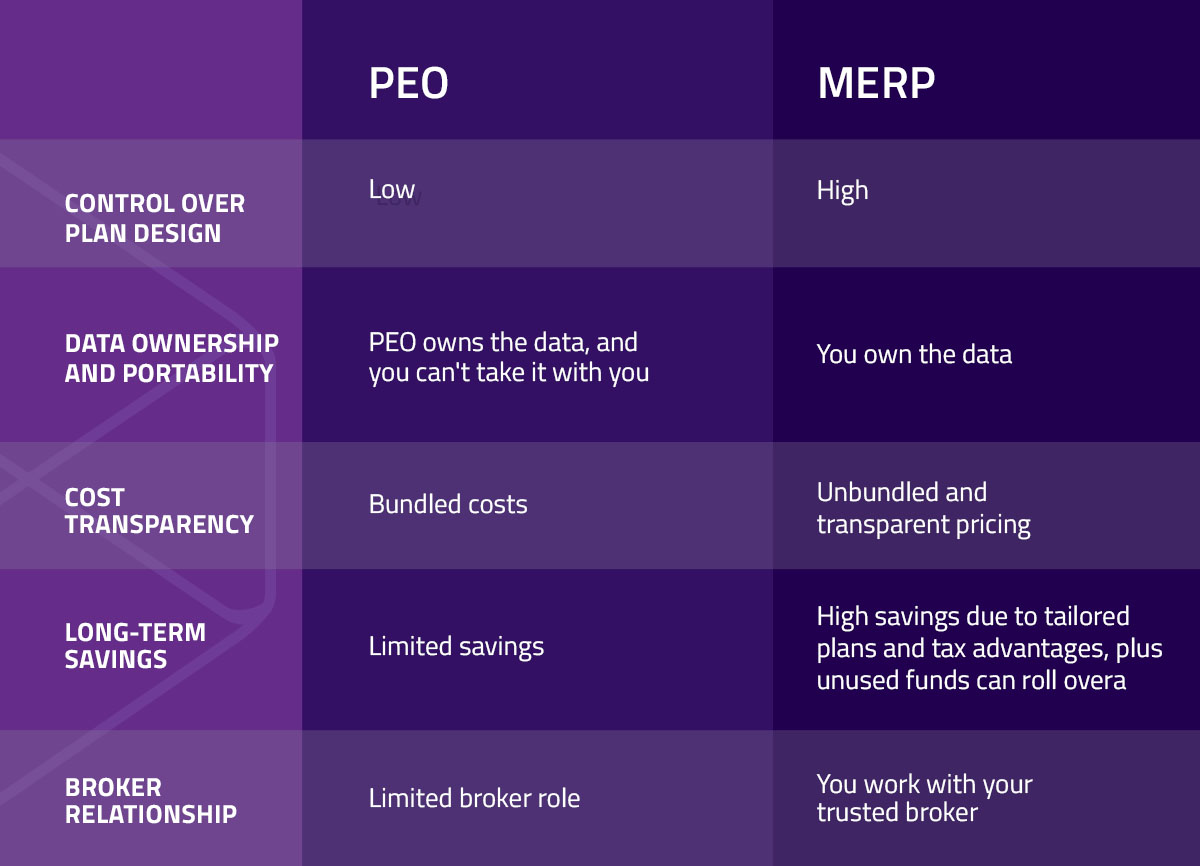

PEO vs. MERP

Here's a side-by-side comparison of a PEO and a MERP to help you see the full picture:

| PEO | MERP | |

|---|---|---|

| Control over plan design | Low | High |

| Data ownership and portability | PEO owns the data, and you can't take it with you | You own the data |

| Cost transparency | Bundled costs | Unbundled and transparent pricing |

| Long-term savings | Limited savings | High savings due to tailored plans and tax advantages, plus unused funds can roll over |

| Broker relationship | Limited broker role | You work with your trusted broker |

How a MERP Works

A benefits administrator helps in managing MERP claims.

- You establish the plan rules: As an employer, you set the rules for eligible expenses and the reimbursement process. You can set unused funds to roll over month-to-month or to the next year.

- Employees submit claims: After employees incur medical expenses, they must submit their claims with supporting documents, such as invoices or receipts, for reimbursement. Some administrators, like The Difference Card, offer a card that lets employees swipe for expenses, such as copays. Employees may also need to explain their reason for the expense.

- The administrator reviews and approves claims: The plan administrator reviews the claims to see if they meet your criteria. They may ask for additional documentation if needed. After they approve the claim, employees can receive the reimbursement. The Difference Card can process claims in two days or less.

Frequently Asked Questions

To help you understand how a PEO works and whether it's beneficial for you, explore these answers to common questions:

Why Is a PEO So Expensive?

Working with a PEO can be expensive due to its fee structure and the bundle of services it offers. While the PEO can negotiate rates for healthcare benefits, you must also consider payments for HR tasks, including compliance consultations, custom reporting, onboarding, and termination fees. The PEO may also charge for software use.

You may need to pay these fees monthly, per employee. They may also cost a percentage of your total payroll. Scaling your business and increasing your payroll can balloon the costs, even if you don't need additional HR services. Also, even if you get competitive rates for the health benefits, you're still susceptible to annual rate hikes.

Who Owns the Employees in a PEO?

The federal law recognizes a certified PEO (CPEO) as the employer for tax purposes. A CPEO is a PEO certified by the Internal Revenue Service for meeting specific requirements. This is why employees receive the W-2 from the PEO. However, you share employment responsibilities with the PEO.

The PEO can help you meet certain obligations, such as through payroll management and compliance support, but it still can't take full legal responsibility. It can serve as your advisor to make sure your company is compliant with relevant laws and regulations. Meanwhile, you maintain full control of your workforce.

If you have an in-house HR team, a PEO can supplement it. This can help your HR team focus on your employees instead of paperwork.

Why Do Companies Leave a PEO?

There are many reasons why companies leave a PEO. For instance, a PEO gets more expensive the larger your company grows. Although you may get competitive benefits, you still need to pay other HR fees. If your company develops complex HR needs, a PEO may also struggle to support these needs. A better long-term solution would be to look for alternatives, like a MERP.

A growing workforce may also develop other healthcare needs, which a PEO won't meet. With a MERP, you can customize employee benefits while increasing your savings. Companies can offer these tailored benefits as a competitive advantage, which is particularly important when scaling their business. You also get more hands-on control when managing related employee data.

A PEO also controls the employee handbook and policies. This impacts a company's culture, which plays a role in employee satisfaction. Creating these policies yourself can be more beneficial for your business long-term.

How Many Employees Do You Need for a PEO?

There's often no required number of employees to work with a PEO, although a PEO can require a minimum number of participants for health benefits. You can work with a PEO whether you're a small or large business. However, the larger your company, the more expensive a PEO can be. It can charge per employee or a percentage of your total payroll.

Improve Your Healthcare Benefits With The Difference Card

While a PEO can offer insurance benefits, these benefits are bundled with other administrative costs you don't always need. You also get less flexibility regarding your choice of policy, which can sacrifice employees' health and satisfaction.

If you're looking to upgrade your employee benefits, consider working with The Difference Card. We can help you create unique plan designs specific to your workforce.

On average, we help companies save 18% on insurance costs without reducing benefits. That amounts to $1.8 billion in healthcare savings for our clients. Our tailored plans also result in an average annual net savings of over $2,000 per employee. You can even keep your current insurance carrier.

We can help you analyze the benefits of a MERP compared to a PEO based on your circumstances. To get started, request a proposal today.