Employers Brace for the Largest Health Insurance Increase in 15 Years

Table of Contents

Offering healthcare benefits is essential in staying competitive. In 2025, 88% of employers consider them as very or extremely important. However, a significant health insurance cost increase is expected in 2026 and beyond, posing a challenge for employers and brokers alike. Employers may need to adjust their budgets without sacrificing the needs of their employees, and brokers need to propose a better cost-containment solution.

The healthcare cost drivers vary, including inflation, technological advancements, utilization rates, and legislation. Solutions also differ based on the employer's unique situation. As a broker employers rely on, you must stay on top of these changes and understand how your clients can navigate them. In this article, The Difference Card breaks down the trends you need to know.

2026 Faces the Largest Surge in Healthcare Costs in Over a Decade

Different studies estimate a huge increase in healthcare costs in 2026. Aon predicts that employer-sponsored plans will surge at about 9.5%, the highest since 2011. Meanwhile, Mercer's survey of over 1,700 U.S. employers projects the health benefit cost per employee to rise by 6.5% on average in 2026. Employers who don't adjust their plans may see an increase of up to 9%.

The International Foundation of Employee Benefit Plans (IFEBP) also estimates a 10% increase in healthcare costs due to catastrophic claims and the rising cost of prescription drugs. While many factors contribute to the rising expenses, 2026 marks the fourth consecutive year with elevated rates. The average annual increase in the previous decade was only 3%.

Why Is Health Insurance Cost Increasing?

Rising healthcare costs influence premium increases. However, other factors also play a role. Here's how each of them contributes to the expenses:

1. Inflation

Inflation in healthcare spending often outpaces the rest of the economy's inflation. However, even with a similar growth rate, the price increase remains significant. For instance, from March 2023 to March 2024, medical care costs increased by 2.2% while the rest of the goods and services increased by 3.5%. The cost of hospital and related services increased by 7.7%, while the cost of nursing homes rose by 3.9%. Insurers adjust their premiums to keep up with the costs.

Other insurers also consider broader economic factors, such as labor shortages. They consider how healthcare workers' wage increases influence increasing medical prices. However, prices for private insurers typically rise at a faster rate than public counterparts. Private insurer pricing results from provider negotiations, while public payer pricing, such as Medicare and Medicaid pricing, is determined by the administration.

Additionally, increasing provider consolidation offers healthcare providers more negotiating power. This can result in higher reimbursement rates and affect insurance premiums. Eleven percent of employers attribute the increasing healthcare expenses to medical provider costs.

2. Specialty Drugs and Technological Advances

Twenty-three percent of employers attribute the rising healthcare expenses to the cost of prescriptions, while 15% claim the cost is due to chronic health conditions. Those who believe costly prescriptions to be the reason believe the following drugs to be the cause:

| % of Employers | Causes of the Increasing Healthcare Cost |

|---|---|

| 59% | GLP-1 drugs |

| 50% | Cancer drugs |

| 21% | Cell and gene therapy |

| 26% | Other drugs |

While many companies cover GLP-1 drugs for diabetes, some cover them for obesity. In 2026, companies may attempt to mitigate expenses by requiring approval for the use of GLP-1 for weight loss, while some insurers exclude the drug altogether for weight loss purposes. The growing number of diagnoses also exacerbates the increase in cancer care treatment. Companies are focusing on cancer prevention and screenings to help manage the costs.

Apart from prescription costs, technological advances also contribute to the rising expenses. The health services and technology (HST) industry — companies that offer healthcare tools, like artificial intelligence (AI) — and specialty pharmacy-related services have a growing share in the industry's EBITDA, which is estimated at 19% in 2024. Its expected compound annual growth rate (CAGR) from 2023 to 2028 is 8%.

EBITDA refers to earnings before interest, taxes, depreciation and amortization. The rising rates mean an increasing portion of the industry's profit is generated from technological services for handling expensive medications.

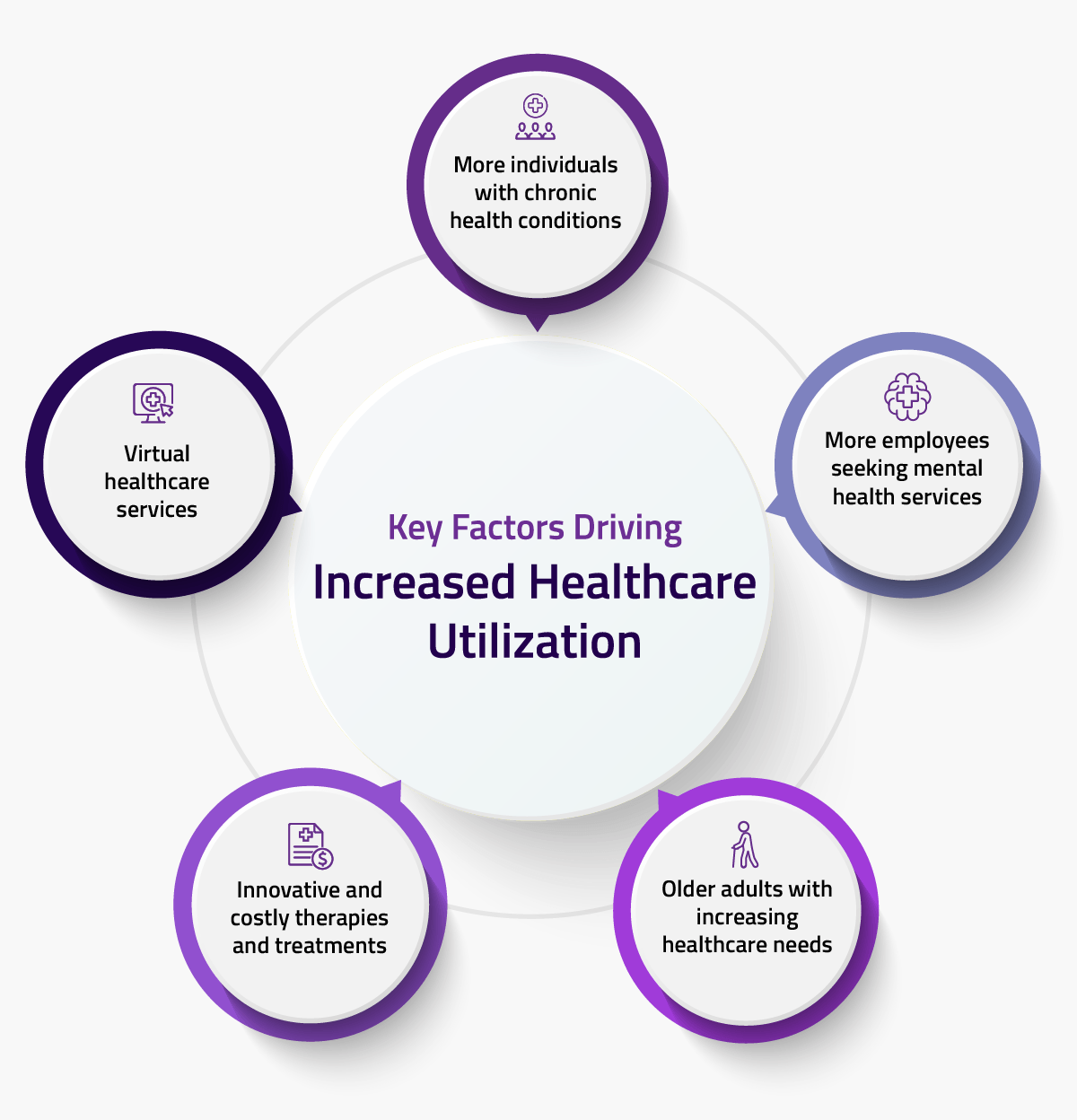

3. Increased Healthcare Utilization

Over the past 15 years, healthcare utilization has increased, contributing to higher healthcare spending. The higher the spending, the higher the chances of an increase in premiums the following year, especially with fully insured plans. The following reasons contribute to the increase in utilization:

- More individuals with chronic health conditions

- More employees seeking mental health services

- Older adults with increasing healthcare needs

- Innovative and costly therapies and treatments

- Virtual healthcare services

Catastrophic claims, or claims comprising a large medical bill for one person, also prompt insurers to raise premiums to cover the costs. These claims often cost thousands to millions of dollars for a single bill. While insurers need to justify rate increases, 31% of employers believe that catastrophic claims are a contributing factor to the increase in healthcare expenses.

4. Legal Drivers

Regulatory changes also influence healthcare prices, with recent changes impacting prices for 2025 and beyond. For instance, companies and healthcare providers are watchful of cost spikes related to tariffs. A significant portion of medical goods in the U.S. comes from international sources, including medical devices, pharmaceuticals, personal protective equipment, and other essential items such as needles and syringes.

In the first four months of 2024, the U.S. imported over $14.9 billion in medical equipment. Tariffs may impact the availability of these healthcare essentials, increasing costs and potentially causing shortages. Some insurers factor this uncertainty into their rate determinations.

Additionally, Marketplace premium payments may increase due to the expiration of enhanced premium tax credits in 2025. Brought about by the Inflation Reduction Act (IRA), the enhanced tax credits increased the financial assistance available for Marketplace and middle-income enrollees. Once the tax credits expire, some enrollees will lose eligibility for this assistance and experience higher premiums.

How Employers Can Combat High Insurance Costs

Employers can combat high insurance costs by analyzing trends and identifying cost-containment strategies tailored to their employees' needs. Employers can consider opting for higher deductibles and providers with narrower networks. They can also establish health and wellness initiatives to encourage a healthy lifestyle for their employees.

1. Higher Deductibles and Copays

Twenty-seven percent of employers believe that cost-sharing initiatives would be effective in managing healthcare costs in 2026. This includes shifting costs to employees through higher deductibles and out-of-pocket expenses, such as copays. A lower copay tends to come with a higher premium, while a high-deductible health plan (HDHP) paired with a health savings account (HSA) can mitigate expenses for employers and employees. An HSA also provides tax advantages and retirement benefits, offering cost savings without sacrificing an employee's needs.

Apart from deductibles, 17% of employers consider relying on plan design initiatives, such as dependent eligibility audits, spousal surcharges, or formulary changes. Other employers may also choose plans without prescription coverage or opt for a separate prescription plan. The more specialized brand names the insurance covers, the pricer the premium may be.

2. Narrower Networks

Narrow network health plans limit coverage to certain healthcare providers. The larger the network, the more expensive the premium may be. While there's no specific definition of what constitutes a narrow network plan, they often cover less than a quarter of the physicians in a location.

Twenty-three percent of Marketplace enrollees can be considered a part of a narrow network plan. About 70% were in a plan that covered up to half of the doctors in their area. Although limited in coverage, narrow health plans still come with high-quality providers. They can often be an exclusive provider organization (EPO) or health maintenance organization (HMO).

Apart from potentially lower premiums, an HMO also requires doctor referrals to see a specialist. This helps prevent potentially unnecessary healthcare expenses. However, when selecting a narrow network provider, employers still need to consider what's most suitable for their employees' needs.

In the Marketplace, 1 in 5 enrollees reported that their insurance did not cover the provider they needed, while about 23% noted that it was difficult to book an appointment with a covered provider. While network size varies, urban areas tend to have lower average provider participation rates.

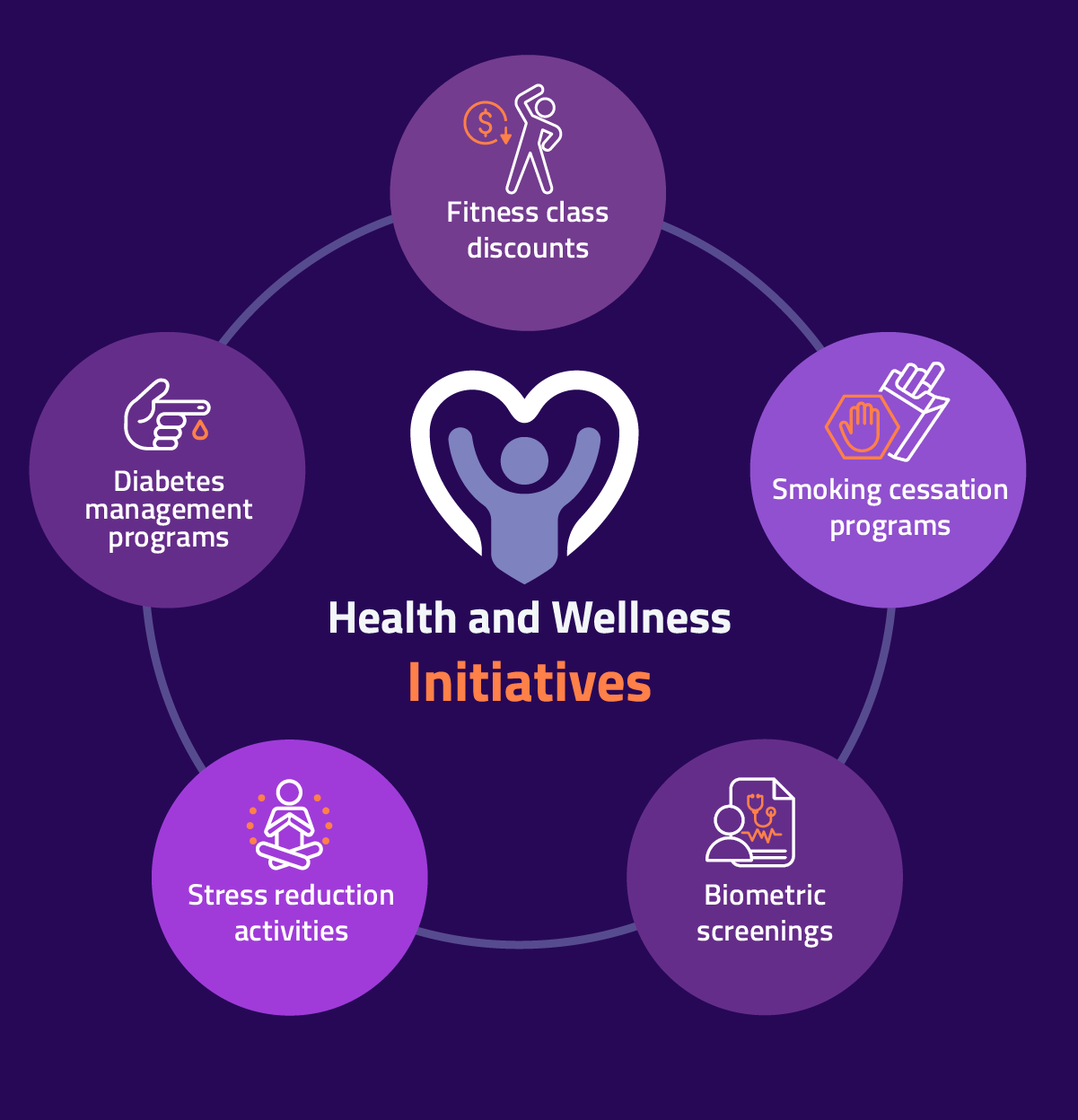

3. Health and Wellness Initiatives

Different health and wellness initiatives can promote a healthy lifestyle, which benefits both employees' and employers' budgets in the long term. This could be through:

- Fitness class discounts

- Smoking cessation programs

- Biometric screenings

- Stress reduction activities

- Diabetes management programs

Regularly educating and disseminating health-related information can also help employees make more mindful decisions regarding their health benefits. For instance, through a company seminar, employees may learn when they should visit urgent care centers instead of emergency rooms. They may also learn to spot errors in their medical bills.

Additionally, making healthcare more accessible through virtual services can help manage costs. Employees won't need to travel to the doctor's office and still get the healthcare they need. Seventeen percent of employers believe that telemedicine and other initiatives can be effective, while 12% think that utilization control initiatives, such as nurse advice lines and prior authorizations, would help.

The Broker's Role

If you're a broker, the rising healthcare costs pose a challenge and an opportunity. When planning with your clients, consider the long-term strategies that can help navigate budget concerns. While some employers may benefit from cost-sharing, smaller businesses with up to 50 employees may find the Small Business Health Options Program (SHOP) more beneficial.

SHOP plans offer flexibility for employers and employees. For instance, employers can choose to offer health-only coverage, dental-only coverage, or both. Employers also have the option to choose how much they pay toward premiums and whether to offer coverage to dependents.

Larger employers may benefit from cost-containment solutions, like a Medical Expense Reimbursement Plan (MERP). A MERP is an employer-sponsored plan that lets employees receive reimbursement for out-of-pocket expenses. In this plan, the employer has the freedom to set the rules for eligible expenses. Employees also get to contribute through payroll deductions, which reduces their taxable income.

Clearly communicating with employers their options and spreading this knowledge to employees helps everybody get the optimal solution for their needs. You can also provide support during open enrollment and offer compliance services that reduce unnecessary healthcare costs, such as fines and litigation fees.

Frequently Asked Questions

Some questions may arise when employers and employees see changes in healthcare premiums. Consider these answers when explaining the situation to your clients:

Why has my insurance premium increased?

Insurance premiums increase due to many factors. For instance, medical care prices typically increase annually, sometimes at a rate higher than the general inflation rate, which can impact insurance premiums. Technological advances, such as the use of AI for optimized billing, also influence the cost.

If more people have utilized healthcare services in the past year, and if a large part of these expenses are catastrophic, the next year's premiums can also increase to cover the expenses. Legislative changes, such as tariff changes, also impact the costs of medical products imported into the U.S.

Is it cheaper not to have health insurance?

It's not always cheaper to go without health insurance. While employers and employees won't be paying premiums, emergencies can leave a dent in an employee's budget. What's more, individuals without health insurance may be penalized, depending on the state they live in. Large employers can also be penalized if they meet the definition of an Applicable Large Employer (ALE). The Affordable Care Act (ACA) requires certain employers to provide affordable minimum essential coverage to full-time employees and dependents.

How can I lower my health insurance cost?

Employers can lower their health insurance costs by reevaluating their plans and considering cost-containment solutions. They can also offer health savings accounts with high-deductible health plans to mitigate out-of-pocket expenses. Choosing a more affordable network and promoting a healthy lifestyle through company initiatives can also benefit the company in the long term.

Help Your Clients by Planning Ahead

The surge in healthcare costs expected in 2026 may come as a surprise to employers and employees. As a broker knowledgeable in the different cost-effective strategies, you have the opportunity to guide them in navigating the changing circumstances. Whether the strategy you propose aims to adapt to inflation, reduce costs on unnecessary drugs, limit utilization to essential health needs, or align with legislation, you can clearly outline and discuss with your clients their options.

Opting for an HDHP with an HSA, choosing limited network providers, and starting health-related initiatives can be ideal temporary or long-term solutions. However, what matters most is that employers can provide what their employees need without sacrificing their bottom line.