The Broker’s Four-Part Framework for a Winning Health Insurance Strategy

Table of Contents

A good health insurance plan can provide important assistance to your clients, but there are countless options available for businesses. What can you do to ensure you offer a personalized and impactful service that provides effective coverage and helps clients understand the common issues?

If you're a broker, creating a clear path for your clients helps you stand out in a competitive market. In the U.S., annual health expenditures were $4.8 trillion in 2023. With costs only increasing, a comprehensive strategy is vital for businesses with long-term goals.

Implementing a four-part framework can help resolve issues, improve employee satisfaction, and deliver long-term results to your clients.

Why Your Clients Need a Strategy

Having a strong health insurance strategy in place, rather than a general plan, can help answer questions about why a decision is made, how it'll be implemented, and why that was the logical option. A good strategy offers clear direction, accounts for potential changes in circumstance, and explains how to achieve the desired results.

A comprehensive healthcare strategy also gives your clients:

- The opportunity to align health insurance with long-term business objectives.

- The signposts and guidance needed to achieve these goals.

- A clear timeline to follow and keep them on track.

- The flexibility to adapt to unexpected issues along the way.

- Financial guidance that considers cost containment strategies in healthcare.

- Actions to retain employees and stand out from competitors.

Part 1: Foundational Data Is Your Starting Point

The right data provides a strong foundation for achieving your clients' desired outcomes. The following areas of research can give you the data points required to explain the importance of having a comprehensive healthcare plan.

Benchmarking

Benchmarking compares a company's data with industry-standard metrics and best practices to measure the organization's health benefits. It keeps client health insurance coverage competitive with other businesses and informs future strategic choices.

Systematically comparing health insurance options to competitors can help retain employees and provide a baseline for building attractive healthcare cost reduction strategies for your clients. The data gives a neutral perspective that highlights industry and individual expectations, while establishing growth goals as part of a successful health insurance strategy.

Benchmarking analysis offers a deeper understanding via:

- 1. Internal benchmarking: This type of benchmarking compares multiple divisions within the same company. It's best used when a business has many internal divisions and offices in different locations and may not suit clients in one centralized area who want to provide benefits equally across the company.

- 2. Functional benchmarking: Functional benchmarking involves comparing your client's organization to others in similar industries that operate with the same criteria. It can offer advantages in gaining candidate interest over these other businesses.

- 3. Competitive benchmarking: This type of benchmarking compares health benefits directly to those of other competitors. It is a good choice for businesses and clients that want to hire and retain skilled workers.

You can also use this data to create cost containment strategies in healthcare coverage for client and employee benefits.

Assessing Population Health and Risk

A comprehensive understanding of population health helps pinpoint where interventions may be needed and shows how existing interventions are working in specific areas. By broadening the focus to the collective health of groups within a chosen location, age range, or industry, you can evaluate current health issues and those who may be at risk in the future.

A health insurance strategy that considers population health includes a wide range of interconnected factors, including:

- Social causation: Social factors include a person's level of education, income, occupation, social support, and the overall quality of housing and clean air.

- General lifestyle: A person's lifestyle includes their ability to cope with stress, diet, alcohol consumption, smoking, and dietary behaviors.

- Genetic factors: Lifespan and health issues can occur due to inherited genetics.

- Other factors: Other factors affecting health include age, sex, culture, and ethnicity.

Accurate population health and risk assessments are essential in discovering opportunities to improve population health. Analyzing population health metrics can provide a strong foundation for your clients.

Defining Clear Business Objectives

One of the main reasons people leave their jobs is a lack of support for health and well-being needs. Balancing employee retention and benefit costs is an important part of any business. Comparing the cost of an attractive benefits package to recruiting new talent as part of a strategic health insurance offering can highlight the potential return on investment it offers.

Aligning these long-term benefits with your client's larger business objectives benefits both the client and employees, maintaining a more loyal and dedicated workforce that offsets the initial costs of the healthcare package.

Part 2: Plan Design and Cost Control Levers

Framing a plan design that suits your clients' needs means simplifying complex information to narrow down the value offered. Studies have shown that the design of a healthcare strategy can improve the value of health spending for businesses and employees.

Offering clear overviews of plan design and cost control options can help your client find a simple and effective solution.

Copays, Coinsurance, and Deductibles

Plan design depends heavily on the copays, coinsurance, and deductibles employees will pay. Offering a simple but comprehensive breakdown of each expense type can reduce concerns and streamline decision-making.

- Copays: Copays are a flat fee the patient pays each time healthcare is provided, such as doctor visits, tests, or visits to the emergency room. With a copay, the amount the patient pays for medical services is stated in advance. For example, a person might have a $15 copay for a monthly prescription or a $200 copay fee for a trip to the emergency room.

- Coinsurance: Coinsurance refers to the portion of healthcare costs a patient pays after meeting the deductible limit. Coinsurance is typically a percentage of the cost of medical services. While the rate varies by plan, patients can expect to be responsible for 10% to 40% of their medical expenses. They usually pay this amount after care has been given and the provider has sent a bill.

- Deductibles: The deductible is the amount a patient must pay for all covered healthcare services before health insurance begins to pay for healthcare expenses. Once the specific deductible amount is met, the individual only owes coinsurance. Deductibles reset annually.

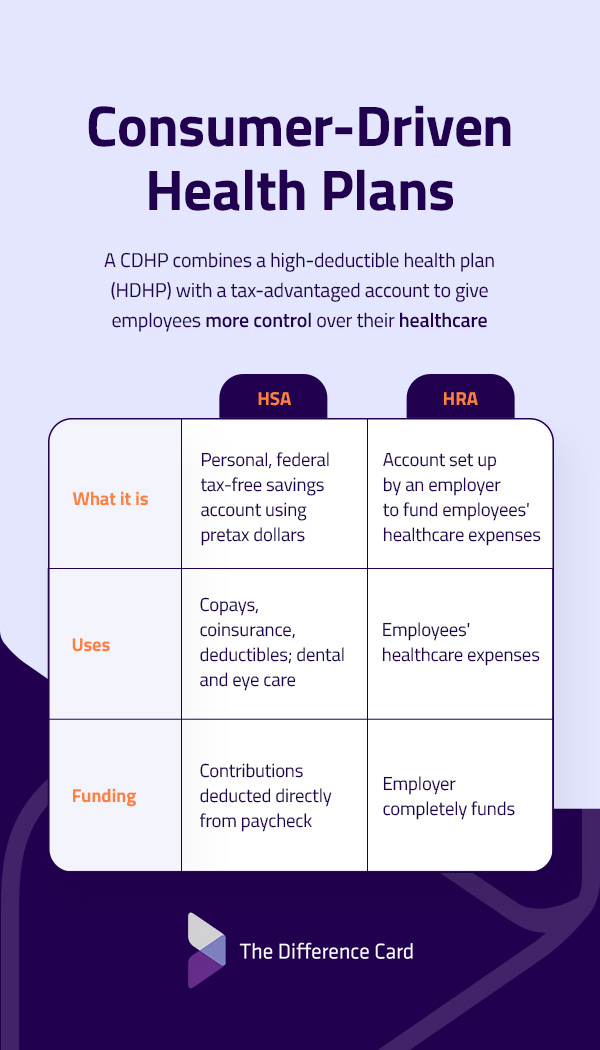

Consumer-Driven Health Plans

A consumer-driven health plan (CDHP) combines a high-deductible health plan (HDHP) with a tax-advantaged account to give employees more control over their healthcare spending. The CDHP best suited for your clients will depend on their specific business needs. Two cost control options are a Health Savings Account (HSA) or a Health Reimbursement Arrangement (HRA).

A Health Savings Account is a personal, federal tax-free savings account that employees can use for medical costs using pretax dollars. Employees can use this money to cover healthcare expenses such as copays, coinsurance, or deductibles. They can also use it for expenses not covered by health insurance, such as dental and eye care.

An HSA set up through an employer allows employees to have their contributions deducted directly from their paycheck, and some companies also match a percentage of the contribution.

A Health Reimbursement Arrangement is an account set up by an employer to fund employees' healthcare expenses. Since the employer completely funds these arrangements, coverage can't be transferred to a new job in the event of a career change. An HRA is a less traditional form of coverage clients may be unfamiliar with but find appealing.

Self-Insurance and Level-Funding

Other cost control options your clients might consider include self-insurance and level-funding. There's no "right" choice, but your clients must understand how each one works so they can decide which approach best suits their business. A strong healthcare funding model can be a unique selling point that attracts the best talent in the industry for your client.

- Self-insurance: This healthcare funding model allows a business to pay employee health claims directly, rather than through an insurance company. A business may work through a third-party administrator (TPA) to manage claims, which offers greater control over healthcare. While it provides flexibility in plan design and potential savings on insurance premiums, the business carries the financial risk of any possible claims.

- Level-funding: This approach involves the business paying a fixed monthly fee that covers any anticipated claims and associated costs. It gives businesses a predetermined cost structure that can still save them money on claims. This method is flexible, while also offering potential refunds if claims are lower than anticipated.

Healthcare cost reduction strategies for clients can succeed or fail depending on the funding model. Being clear about the benefits and limits of each option is essential.

Part 3: Boosting Engagement and Driving Value

For your clients, making current and future employees aware of all the services covered is an integral part of increasing engagement. More engagement helps clients get the most out of their investment by ensuring people use the service to its fullest.

Wellness and Preventive Care

Wellness is a broad concept many people struggle to attach meaning to. However, mental and physical well-being is now an important part of modern healthcare benefits, with many employees considering it a priority when choosing an organization to join.

The Affordable Care Act (ACA) requires insurance to cover many preventive care measures at no cost to the patient, such as medical physicals and screenings, vaccinations, and some wellness programs. Ensuring clients understand the depth of potential coverage in these areas helps them inform employees who may not be aware it exists.

Employee Engagement Plans

Implementing the benefits of client healthcare in promotional and internal communications can significantly boost morale and overall well-being. Some health insurance strategies also have coverage that incentivizes achieving health goals by offering rewards to encourage participation.

Employers can customize their engagement plan based on key data. For example, if they notice issues with absenteeism due to stress, part of their wellness program could include stress management advice.

Telehealth and Digital Tools

The flexibility of modern healthcare innovations means employees can benefit from support beyond their workplace. Your clients can choose from several benefits options that support employee well-being and increase access to care for remote workers.

Advancements like digital apps, virtual consultations, and wearable devices for monitoring health metrics and increasing employee care offer businesses new ways to support their employees. For clients, these benefits can be a huge selling point for recruiting talent or retaining existing team members.

Part 4: Measurement and Long-Term Optimization

The final part of a successful healthcare strategy involves monitoring performance data and results to implement long-term plans to improve efficiency and provide a baseline for improvement. These measurements give clients insights into organizational competence and the ability to improve cost containment in healthcare while providing the best possible coverage.

With the cost of healthcare in the U.S. rising, healthcare spending is a major concern for employers. Long-term planning and metrics that consider employee satisfaction and the financial bottom line help keep all parties satisfied.

Strategic Health Insurance Metrics

Three key areas of health insurance metrics show employers how the combined efforts of these framework strategies can improve employee satisfaction, business reputation, and the costs associated with their plan.

- User metrics: Measure how satisfied employees are with their healthcare coverage, service, and experience. User metrics also include the number of employees who remain with the company and how often they engage with apps, resources, and any other aspects of their healthcare.

- Operational metrics: The average amount paid for a claim, processing times, and the number of employee claims over a specific period indicate how successful the policy is on an operational level.

- Finance metrics: Improve cost containment in healthcare by knowing the amounts for claims paid out and premiums collected, and determining the expense ratio associated with them. These figures explain how successful a business's health insurance plan is. Finance metrics also include measuring net profit margins and expenses like administrative costs.

Creating a Long-Term Strategic Roadmap

Harnessing all of the available technologies to map out a health insurance strategy that aligns with employee needs and client expectations is the final key to unlocking the best results. There are three essential components of creating this long-term plan.

- Technology integration: Embracing innovations and new digitalized personal care tools is essential for meeting modern expectations. Technology can streamline many administrative processes that clients see as time-consuming and repetitive. Working with trusted new technologies keeps businesses aligned with the latest advancements while preparing them for the future.

- Personalization: Technology also helps personalize healthcare tools to reduce costs, decrease absenteeism, and improve retention. A personalized service bridges the gap between business and employee, reducing miscommunication and improving outcomes.

- Workplace culture: Leading by example can influence employees to use all the healthcare tools available. A workplace culture that prioritizes health as a key pillar of the business fosters a more open approach to well-being, ultimately increasing productivity.

Flexible Healthcare Tools for Long-Term Success

A strong healthcare strategy is crucial to standing out in a competitive healthcare landscape. Clients expect coverage solutions that achieve results for employees and their businesses. The Difference Card allows you to offer your clients customized benefits packages for their employees under one underlying plan.

The Difference Card can be paired with an HDHP to save employers and employees money and provide access to a supportive rep quickly. We generally process claims within two working days. Ready to give your clients a flexible healthcare strategy that delivers on all their needs? Request a proposal to learn more.