What’s the Difference Between an ICHRA and a MERP?

Table of Contents

- Understanding the Terminology

- What Is a MERP?

- What Is an ICHRA?

- Comparing Key Differences Between an ICHRA and a MERP

- Benefits of Choosing a Medical Expense Reimbursement Plan

- Benefits of Choosing an Individual Coverage Health Reimbursement Arrangement

- Choosing the Right Plan

- Explore Insurance Plans With The Difference Card

Insurance brokers are essential in helping employer clients navigate the complex world of health insurance benefits. Employers will want to offer competitive benefits that attract and retain top talent while benefiting the business. Understanding the nuanced difference between a Medical Expense Reimbursement Plan (MERP) and an Individual Coverage Health Reimbursement Arrangement (ICHRA) will help you choose and present the right solution.

Businesses have many options when it comes to employee health insurance benefits. Most companies provide traditional health insurance plans that offer employees standardized medical coverage. However, the rise of personalized benefits and innovative reimbursement models is reshaping the benefits landscape. A clear understanding of the core differences between a MERP and an ICHRA is essential for strategic decision-making.

Understanding the Terminology

To effectively guide your employer clients through the intricacies of health reimbursement, it's helpful to define and help them fully understand a few key terms:

- MERP: A MERP is an employer-sponsored health plan that provides reimbursements for eligible out-of-pocket medical expenses.

- HRA: A health reimbursement arrangement (HRA) is a specific type of MERP designed to reimburse employees for qualified medical expenses. A traditional HRA is group-based, but it encompasses more than just group plans.

- ICHRA: An ICHRA is a specific type of HRA that enables employees to purchase individual health insurance.

What Is a MERP?

A MERP is an employer-sponsored benefit that reimburses employees and their dependents for eligible out-of-pocket medical expenses, including copayments, coinsurance, deductibles, and certain medical costs. Many employers pair a MERP with a health plan with high deductibles, low premiums, and higher cost-sharing. With this combined package, employees can use their MERP allowance to cover anything their insurance doesn't. Employers sometimes offer MERP products alone, so employees can choose to use their allowance to pay for individual health insurance.

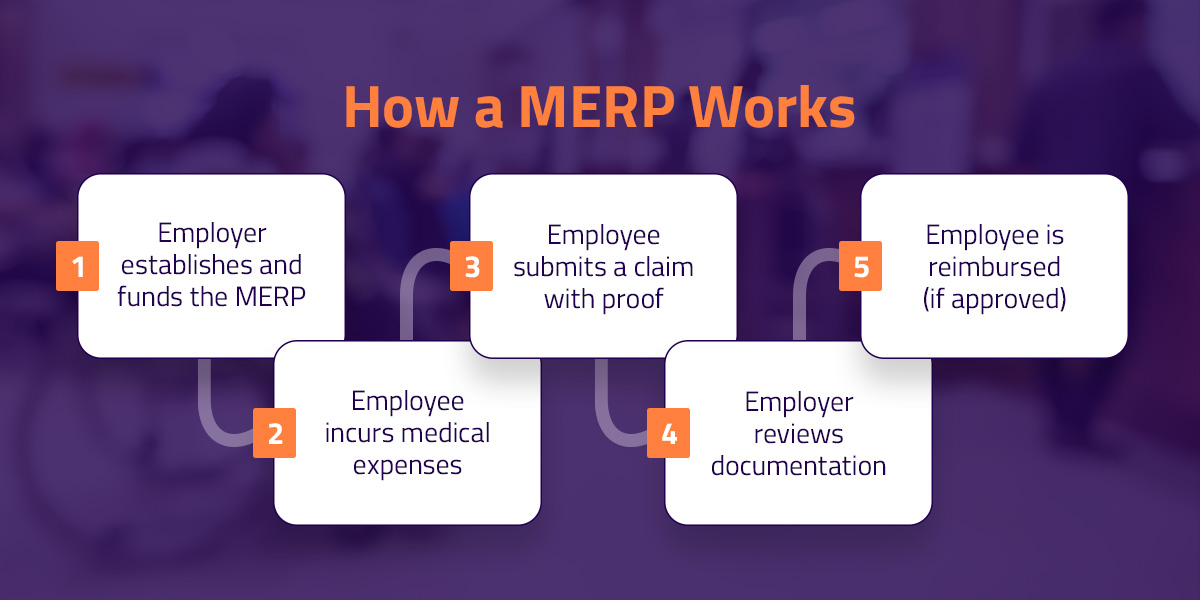

How a MERP Works

When employers provide MERP, they establish the guidelines and rules for what will constitute eligible expenses and reimbursements. When employees have medical costs, they submit claims alongside relevant medical documents for review. Every MERP is subject to compliance with federal regulations, so employers must ensure their plan adheres to the requirements that qualify them for tax benefits. Here is the basic step-by-step process of how a MERP works:

- Employer establishes and funds the MERP

- Employee incurs medical expenses

- Employee submits a claim with proof

- Employer or other team member reviews documentation

- Employee is reimbursed (if approved)

Brokers can help employers determine if a MERP is a good fit by assessing their specific needs and budget.

What Is an ICHRA?

An ICHRA is a type of health reimbursement arrangement that offers more flexibility than traditional group health insurance plans. This insurance model means employees can purchase their own health insurance coverage and receive reimbursement for their chosen premiums. In addition to premiums, an ICHRA can be used to reimburse medical expenses, such as deductibles and copayments. Brokers can guide employers through the complexities of ICHRA compliance and vendor selection.

How an ICHRA Works

Employers may not provide an ICHRA and group health plan to the same category of employees. Based on respective employers' policies, seasonal, temporary, part-time, and full-time workers may be eligible for an ICHRA. If an employer offers an employee an ICHRA and they accept, they must have individual health insurance coverage or Medicare that starts by the time their ICHRA begins. Employers must include certain key information when they offer an ICHRA to an employee, including:

- Coverage start date

- ICHRA dollar amount

- Dependent eligibility

- Special enrollment period (SEP) availability

- Premium tax credit (PTC) impact

- Right to opt-out

- Individual health insurance or Medicare requirement

Implementing an ICHRA often requires partnering with experienced ICHRA vendors who can provide administrative support, compliance guidance, and technology solutions.

The Origins of ICHRA

In 2019, the federal government finalized rules that expanded the availability of health reimbursement arrangements. These rules, effective from January 2020, aimed to provide more flexible and affordable healthcare options for employers and employees.

The ICHRA model was designed to address some of the limitations of traditional group health plans, which often take a one-size-fits-all approach to coverage, and the Qualified Small Employer Health Reimbursement Arrangement (QSEHRA). The main difference between ICHRA and QSEHRA is that the latter is limited to smaller employers. ICHRA allows businesses of all sizes to provide customizable healthcare benefits, enabling employees to select plans that best fit their needs.

Comparing Key Differences Between an ICHRA and a MERP

When brokers compare an ICHRA and a MERP for their clients, it's essential to highlight that while they're similar because an ICHRA falls under the MERP umbrella, they have specific defining characteristics that set them apart in practical application.

Insurance Coverage

The most significant difference between an ICHRA and a MERP is their contrasting insurance coverage requirements. Employees who receive a MERP are not required to have separate health insurance coverage. Employees with an ICHRA must purchase individual health insurance plans that meet minimum essential coverage (MEC) standards.

Employer Flexibility

An ICHRA gives employers control over healthcare costs by allowing them to set fixed reimbursement amounts and outline specific eligibility criteria. This rate predictability makes budgeting easier. Alternatively, when employers choose to provide a MERP option, they'll have more choices in the range of medical expenses that can be reimbursed.

Employee Choice

Receiving an ICHRA empowers employees to choose their own health insurance plans, while a MERP typically has a predetermined set of eligible expenses.

Compliance Requirements

When it comes to MERP and ICHRA, rules do apply that brokers must help employers understand. Both reimbursement plans must meet the requirements of the Affordable Care Act (ACA). A MERP must comply with ACA market reforms, such as avoiding unreasonable annual or lifetime limits and providing coverage for dependent adult children up to age 26. An ICHRA must be considered affordable based on rules set by the ACA. If it's not regarded as affordable, the employer could face penalties. An ICHRA and a MERP also have to follow existing compliance requirements like the Consolidated Omnibus Budget Reconciliation Act (COBRA) and patient privacy laws.

Benefits of Choosing a Medical Expense Reimbursement Plan

MERP products are available in numerous variations to suit different business sizes, budgets, and goals. These packages can be customized to meet the specific needs of employers and employees.

Employer Benefits

Brokers can emphasize the cost control benefits of a MERP to employers looking to manage their healthcare spending. A MERP offers employers a strategic approach to managing healthcare costs and enhancing employee benefits. The key advantages include:

- Cost control: One of the primary advantages of a MERP is the level of cost control it provides to employers. Unlike traditional health insurance plans with fluctuating premiums, a MERP allows employers to set a fixed allowance amount for employee reimbursements. This predictability allows accurate budgeting and informed healthcare-related financial planning. Additionally, employers define which medical expenses are eligible for reimbursement, optimizing their healthcare spending and avoiding unnecessary costs.

- Tax deductions: A MERP can offer significant tax advantages for employers because the reimbursements made to employees for their qualified medical expenses are tax-deductible as a business expense. This tax deduction reduces overall tax liability and lowers taxable income.

- Customization and flexibility: Unlike ICHRA, a MERP can be used alongside a traditional health group plan. The ability to use both models allows employers to offer a comprehensive benefits package that combines the security of group coverage with the reimbursement benefits of a MERP. Employers can tailor a MERP to cover an extensive range of medical expenses, including deductibles, copayments, and other out-of-pocket costs, providing employees with significant financial assistance.

- Attraction and retention: Offering attractive benefits can attract talent and retain valuable team members. The competitive nature of today's job market makes powerful recruitment and retention tools especially valuable. The financial assistance MERP provides can help employees manage their healthcare costs and improve their overall financial security. These benefits can lead to increased employee satisfaction, loyalty, and reduced turnover.

- Wellness and productivity: A MERP helps employees afford medical care, which can contribute to a healthier and more productive workforce. When employees have access to medical treatment and preventive care, they are less likely to experience health issues that can lead to absenteeism and reduced productivity.

Employee Benefits

Employers will want to be able to highlight the advantages of the plan they're offering. A MERP provides employees with valuable financial support and greater transparency in managing healthcare expenses. The primary benefits include:

- Tax savings: MERP reimbursements are generally tax-free for employees, providing valuable tax savings. This means that employees receive the full amount of the reimbursement without having to pay income taxes on it.

- Financial assistance: Having a MERP allows employees access to financial assistance with their medical expenses, helping them manage the cost of healthcare. This assistance is particularly beneficial for employees with high-deductible health plans or those who incur significant out-of-pocket medical costs.

- Transparency: Unlike some insurance plans with hidden fees, a MERP clearly defines covered services, deductibles, and copays. This transparency allows employees to make informed decisions about their healthcare spending, reducing the potential for surprise bills and promoting better financial planning.

Benefits of Choosing an Individual Coverage Health Reimbursement Arrangement

You may know what ICHRA insurance is, but do you fully understand the benefits? An ICHRA can be a flexible and beneficial model for both employers and employees.

Employer Benefits

Brokers can highlight the flexibility and portability of an ICHRA to employers who want to attract employees who value choice and control. The many ICHRA benefits for employers include:

- Cost savings and predictability: With an ICHRA, the employer has more predictable healthcare costs because they are capped at the allowance amount. When this limit is set, employees can then choose more affordable marketplace options than a group plan might offer, benefiting both parties.

- Tax advantages: Similar to a MERP, ICHRA reimbursements are tax-deductible for employers and qualify as tax-free contributions for employees. This dual tax benefit makes providing an ICHRA a financially efficient way to offer healthcare support that employees will likely appreciate.

- Targeted flexibility: An ICHRA offers employers the unique opportunity to tailor benefits. Unlike many other plans with more uniform reimbursement structures, an ICHRA allows different allowances to be set based on legitimate job-based criteria. Examples include setting guidelines for different workers, such as those who are full-time, part-time, salaried, hourly pay, or even in various geographic locations. This flexibility allows employers to create customized benefits based on employee demographics and needs, serving the business and employees alike.

- Competitive advantage: Offering an ICHRA can enhance the appeal of an open role and be a factor in employees choosing to remain loyal to a company. Many employees will appreciate having more control over their healthcare choices and budgets. This model may help employers attract new talent and show current employees a commitment to their well-being.

Employee Benefits

Employers must understand how to present the benefits of this plan to their employees for maximum employee satisfaction. Many employees favor ICHRA over traditional health insurance for reasons such as:

- Flexibility: With an ICHRA, employees are empowered to choose the plan that suits them best. This model allows employees to make decisions that align with their unique healthcare needs and preferences. This flexibility ensures that employees can prioritize the coverage that matters most to them, whether it's access to specific specialists, comprehensive mental health services, robust prescription drug coverage, comprehensive vision and dental care, specialized treatments for chronic conditions, or a lower deductible.

- Portability: One of the most significant and unusual advantages of an ICHRA compared to most plans is its portability. Unlike group health plans that are tied to employment, individual health insurance plans purchased through an ICHRA are owned by the employee. This means that when an employee changes jobs, they can take their health insurance coverage with them, ensuring continuous access to care and eliminating the disruption of switching plans.

- Budget control: An ICHRA gives employees greater control over their healthcare budget. Each individual can choose a plan with premiums, deductibles, and coverage levels to fit their financial situation. When employees have agency over their healthcare spending, it can promote responsible utilization and potentially lead to long-term savings.

- Tax benefits: As stated already, ICHRA contributions are tax-free for employees.

Choosing the Right Plan

Selecting the optimal health reimbursement arrangement requires careful consideration of your client's or organization's specific needs, priorities, and workforce demographics. There is no one-size-fits-all solution, as both a MERP and an ICHRA offer distinct advantages.

To make an informed recommendation or decision, assess your client's or company's risk tolerance, administrative capabilities, and employee preferences. Evaluate the potential impact on employee satisfaction, recruitment, and retention. Producers should also consider their clients' long-term service and support needs, including the selection of reliable ICHRA providers. Remember to consult with legal and benefits professionals to ensure compliance with all applicable regulations and to optimize plan design for maximum effectiveness.

Explore Insurance Plans With The Difference Card

The Difference Card specializes in Medical Expense Reimbursement Plans for organizations of all sizes. If you're an employer seeking to optimize your benefits strategy, The Difference Card can help. We provide expert guidance in building the most cost-effective healthcare plan tailored to your business's needs.

We also partner with producers to deliver cost-saving solutions that will impress your clients. If you want to become a partner, we welcome the opportunity to support your business. With The Difference Card, you'll receive the support of a dedicated team and exceptional customer service.

Request a proposal today and discover the difference our solutions can make.