A Guide to Extended Open Enrollment

Table of Contents

The Affordable Care Act (ACA) requires employers with over 50 employees to provide specific healthcare benefits, although smaller employers may also do so. Employees can opt for these benefits during open enrollment. There is a set schedule at the federal level. However, some states have their own schedules if they have their own healthcare Marketplaces. Whether open enrollment will be extended or not is up to the state's discretion.

Multiple extensions have been set for 2025. Announcements for next year's extensions can be made in the middle or end of the year. Whether you're an employer or an insurance broker, you can use this article as your guide to understand how open enrollment and extensions work.

Open Enrollment Schedule

Open enrollment is the period people can apply for, drop, or update their coverage. At a federal level, here are the schedules:

| Open Enrollment Date | Coverage Starts |

|---|---|

| November 1 - December 15 | January 1 |

| December 16 - January 15 | February 1 |

Employers typically set their open enrollment period during the fall to submit documents on time. The period usually lasts a week up to a month. Outside these schedules, a person can only change their coverage if they experience a qualifying life event (QLE), making them eligible for special enrollment. For instance, new hires may be able to apply for coverage within 30-60 days of their start date, depending on the company.

If an employee fails to update, cancel, or apply for coverage during open enrollment, they will have to wait for the next open enrollment period. However, open enrollment can be extended depending on the state. Employees who miss the company's deadline can also contact their human resources department for any potential extension.

Open Enrollment Extension

Open enrollment is extended in some states to help more people access quality and affordable healthcare. This extension varies from year to year. For instance, in 2024, the Centers for Medicare and Medicaid Services (CMS) extended open enrollment by three more days, ending it on December 18, 2024, so more people could enroll and have their coverage start on January 1, 2025. This extension was applicable to 31 states that use HealthCare.gov.

Twenty states with their own Marketplaces announce when open enrollment extensions are available on their websites. These extensions can extend beyond January 15.

State-Based Exchanges and Extensions

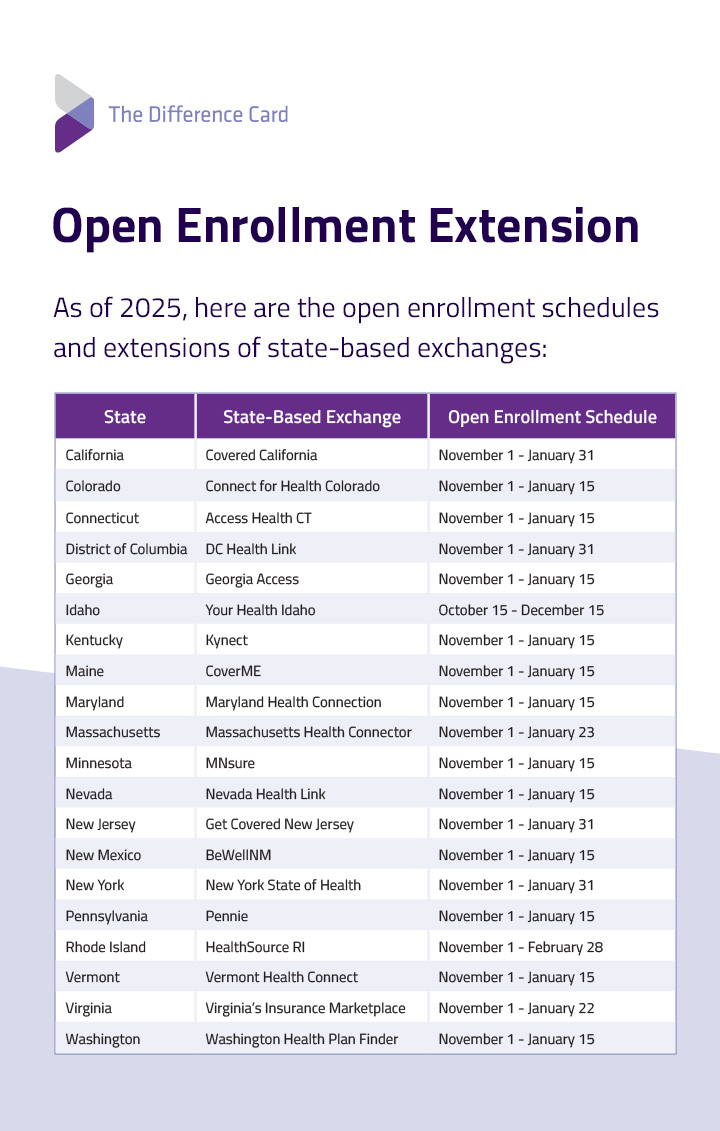

As of 2025, here are the open enrollment schedules and extensions of state-based exchanges:

| State | State-Based Exchange | Open Enrollment Schedule |

|---|---|---|

| California | Covered California | November 1 - January 31 |

| Colorado | Connect for Health Colorado | November 1 - January 15 |

| Connecticut | Access Health CT | November 1 - January 15 |

| District of Columbia | DC Health Link | November 1 - January 31 |

| Georgia | Georgia Access | November 1 - January 15 |

| Idaho | Your Health Idaho | October 15 - December 15 |

| Kentucky | Kynect | November 1 - January 15 |

| Maine | CoverME | November 1 - January 15 |

| Maryland | Maryland Health Connection | November 1 - January 15 |

| Massachusetts | Massachusetts Health Connector | November 1 - January 23 |

| Minnesota | MNsure | November 1 - January 15 |

| Nevada | Nevada Health Link | November 1 - January 15 |

| New Jersey | Get Covered New Jersey | November 1 - January 31 |

| New Mexico | BeWellNM | November 1 - January 15 |

| New York | New York State of Health | November 1 - January 31 |

| Pennsylvania | Pennie | November 1 - January 15 |

| Rhode Island | HealthSource RI | November 1 - February 28 |

| Vermont | Vermont Health Connect | November 1 - January 15 |

| Virginia | Virginia’s Insurance Marketplace | November 1 - January 22 |

| Washington | Washington Health Plan Finder | November 1 - January 15 |

Illinois is looking to transition to a state-based exchange for 2026. States with extended open enrollment for 2026 coverage are California, the District of Columbia, Massachusetts, New Jersey, New York, Rhode Island, and Virginia. The rest still follow the schedule at the federal level.

However, the extensions for open enrollment dates are not set in stone. For instance, Rhode Island only extended its open enrollment period until February 28, 2025, due to a cyber attack. You can keep track of any changes using each state's exchange website.

Extension Guidelines for Employers

Open enrollment periods can be confusing for employees due to the varying deadlines, requirements, and exceptions. As an employer, you can help make the process easier by informing them when open enrollment is and whether open enrollment has been extended.

Here are other things you and your human resources (HR) department can do for a smoother process:

- Send timely notifications: If employees forget about open enrollment, they might miss out on getting the most suitable benefits. By setting up timely announcements, you can be more certain that employees can maximize the employer-sponsored benefits.

- Allow some wiggle room with extensions: If your state announces an extension period, consider whether to reflect that in your own schedule. Many employees miss open enrollment deadlines, so being a little more flexible can be helpful.

- Use familiar concepts: Health insurance jargon can be confusing. It's best to use simple terms when talking about the different plans you offer. According to one study, 73% of employees want to be more educated on company benefits. Employees can fight analysis paralysis by having a clear understanding of their options.

- Point out coverages and limitations: Different benefits come with varying premiums, deductibles, and out-of-pocket costs. Explaining these costs clearly from the start can encourage prompt applications.

- Regularly reflect and fine-tune benefits: Your company should reflect whether your benefits are still sufficient or appropriate. Will it be helpful to offer a Health Savings Account (HSA) in addition to what you provide? Or maybe you should offer a Health Reimbursement Arrangement (HRA) as an option. Consider your employees' changing needs over time and budget accordingly.

- Make the most of virtual resources: You can provide online tools that educate your employees about different healthcare benefits so they can make an informed choice. You can also create virtual benefit fairs for your remote employees.

How Employees Can Apply for Coverage

The HR department is usually responsible for helping employees get the coverage that they need. Here are the steps employees need to take:

- Review available employer-sponsored benefits: Employees should consider which plan best fits their needs. For instance, offering a Flexible Spending Account (FSA) can help employees pay for medical expenses with pretax funds. If employees want to invest the money they save for healthcare, an HSA is an ideal solution. You might also offer a Medical Expense Reimbursement Plan (MERP) to cover doctor's office visits, hospitalization, and urgent care.

- Calculate the contributions, deductions, and out-of-pocket costs: As an employer, you can contribute to your employees' accounts as part of the benefits package. Employees should consider how much to expect, together with their costs. Also, employees need to figure out how much they're willing to pay for out-of-pocket expenses.

- Identify the eligibility requirements: Once employees find a plan they're interested in, they should figure out if they're eligible. Requirements may be based on their tenure and account prerequisites. For instance, a high-deductible health plan (HDHP) is required to open an HSA. You may also provide additional or specific health benefits to permanent employees.

- Fill out and submit the application form: Forms vary per company, and available packages also differ. Employees must fill out and submit the enrollment form on time.

What Happens if Employees Miss the Deadline

Sometimes, an employee misses the deadline for open enrollment, including the open enrollment extension. With an existing plan, missing a deadline only means the coverage will be renewed as-is. If they currently don't have coverage, they can try for plans not regulated by the ACA. Your company can offer these non-qualified plans as supplemental coverage, and they typically allow enrollment year-round. These plans include:

- Medical discount plans

- Critical illness plans

- Dental or vision plans

- Health plans with short-term coverage

Employees may also get coverage through a special enrollment period (SEP), but only with a qualifying life event.

Special Enrollment Periods

Special enrollment periods let people enroll, drop, or update their coverage due to recent changes in their lives. These life changes make their current plan inapplicable. Here are a few examples of a qualifying life event that can be experienced by your employees:

- They've moved to a new home.

- They got married.

- They had a baby or adopted a child.

- They got divorced or legally separated.

- They're switching jobs.

- They graduated and lost eligibility for a student health plan.

- Their plan was discontinued.

- Someone from their original coverage has passed.

- They've lost their coverage through a family member.

- They were affected by a natural disaster.

- They just became a U.S. citizen.

If you offer an HRA or a Qualified Small Employer Health Reimbursement Arrangement (QSEHRA), your employee may also be qualified for special enrollment. The SEP typically lasts 30-60 days, depending on the QLE. However, in 2025, CMS offers a monthly SEP if a person's projected household income is at or below 150% of the federal poverty level (FPL).

If employees don't opt for supplemental coverage or are not qualified for an SEP, then they may be susceptible to penalties.

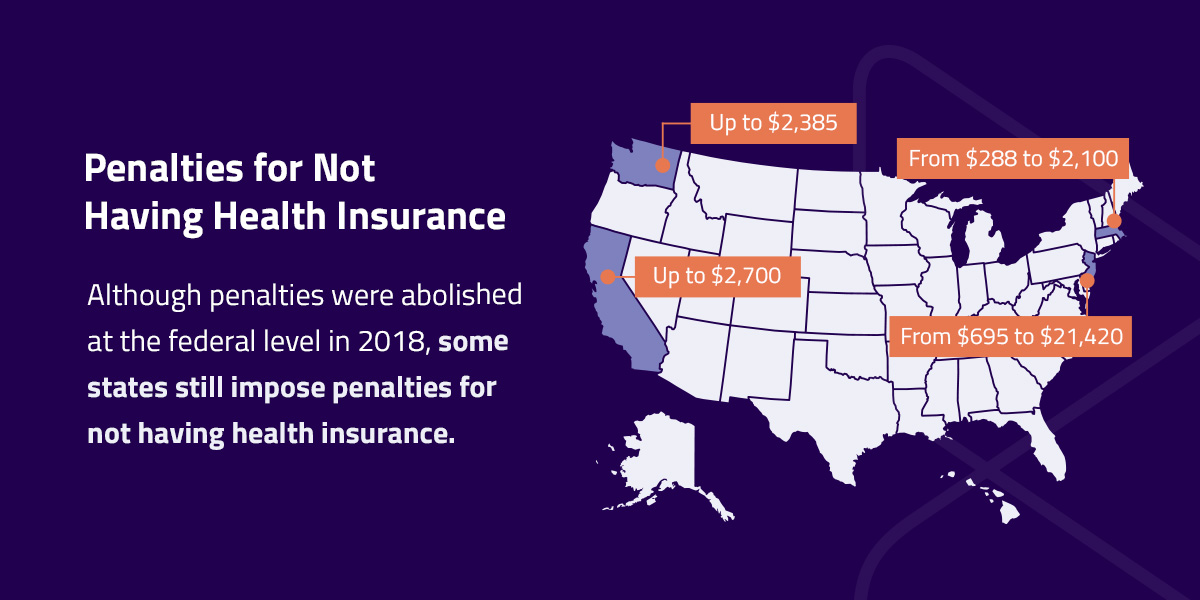

Penalties for Not Having Health Insurance

Although penalties were abolished at the federal level in 2018, some states still impose penalties for not having health insurance. If you belong in such a state, you can further encourage timely applications by informing your employees of these penalties. Here are the states with tax penalties:

| STATE | pENALTY |

|---|---|

| California | Up to $2,700 per family of four |

| Washington, D.C. | Up to $2,385 per family or 2.5% of the family income over the federal tax filing threshold, whichever is greater |

| Massachusetts | From $288 to $2,100 per year depending on the income |

| New Jersey | From $695 to $21,420 depending on the family size and income |

| Rhode Island | Depends on the family size, income, and metal plan |

States may change these penalties annually. Employers and insurers may also need to file annual information returns for states to enforce these rules. However, there are exemptions to these penalties, depending on the state. Some exemptions include persons who:

- Have an income below the state tax filing threshold

- Are members of a healthcare sharing ministry

- Are members of a religious sect opposed to health benefits

- Are members of a federally recognized tribe

- Have recently been incarcerated

- Have been without coverage for less than three consecutive months

If employees miss out on getting health insurance, it may affect you as an employer. If you're a large employer, you may have a shared responsibility payment if you don't offer minimum essential coverage to at least 95% of your full-time employees and their dependents. Offering minimum essential coverage means providing benefits that:

- Covers at least 60% of the total cost of the plan coverage

- Affordable based on the employee's pay rate or the federal poverty line

Unaffordable health insurance can be a reason for an exemption from an employee's state tax penalty. As an employer, you can budget for more benefits, so employees can find a better fit.

Examples of Benefits Employers Can Offer

When deciding which benefits to offer your employees, consider the following:

- Medical Expense Reimbursement Plan (MERP): A MERP enables your employees to receive reimbursements for out-of-pocket healthcare expenses. Eligible expenses typically include prescription medications and doctor's visits. Employees contribute to the plan through payroll deductions, reducing their taxable income.

- Health Reimbursement Arrangements (HRA): An HRA is an employer-funded reimbursement account that also covers eligible medical expenses. You'll define the eligibility requirements as the employer. The funds are not part of the employee's taxable income.

- High Deductible Health Plan (HDHP) and Health Savings Account (HSA): An HDHP has a higher deductible but a lower monthly premium, which can make it a more affordable plan for your healthier employees. It partners well with an HSA, which is a dedicated savings account for medical expenses.

- Flexible Spending Account (FSA): An FSA is a tax-advantaged account where employees can allocate a portion of their pretax salary for IRS-eligible expenses, including vision, dental, medical, and other out-of-pocket healthcare costs.

You can also create a wellness program to build a culture of healthy living for your employees. This program can come with incentives such as reduced deductibles or discounts on copays. Employers and brokers can discuss all available options and identify which is most suited for employees.

The Difference Card Makes the Open Enrollment Process Easy

We understand how tough open enrollment season can be, especially without the right support. That's why The Difference Card is here to ensure that the implementation of your benefits is seamless. We can provide your HR department with the appropriate education and communication tools, so employees can better understand their options. You'll also get a dedicated account manager, so you can get the timely answers you need.

With The Difference Card, you can build the most cost-effective healthcare plan without sacrificing employee benefits. On average, we help organizations save over 18%, with a total of $1 billion in savings and counting. We can also help you provide multiple types of accounts, including an HSA, an FSA, or an HRA. You can even offer non-health-related benefits, such as parking plans and dependent care accounts. To start preparing for the next open enrollment season, request a proposal today!