What Is a Hybrid Approach for HDHPs?

Table of Contents

- Is a Hybrid HDHP Right for Your Organization?

- Hybrid HDHP vs. Traditional Plans

- The Core Benefits of a Hybrid Healthcare Plan

- Maximizing Savings With an HDHP-HSA Combination

- A Hybrid HDHP Guide for Employers

- Common Pitfalls to Avoid

- Frequently Asked Questions

- Get The Difference Card for a Better Hybrid Healthcare Solution

Healthcare costs are rising steadily. Employers are projected to see a 10% cost increase for 2026, with average annual family premiums reaching $26,993. For business leaders, this creates an impossible choice. Cut costs and risk losing talent, or maintain benefits and erode profit margins?

A hybrid high-deductible health plan (HDHP) offers a better solution. By combining the low premiums of an HDHP with the predictable copayments of a preferred provider organization (PPO), this approach delivers cost savings without sacrificing employee satisfaction. This guide explains how to implement a hybrid approach for an HDHP successfully.

Is a Hybrid HDHP Right for Your Organization?

A hybrid HDHP plan design delivers employer savings while maintaining employee access to affordable care.

To qualify as an HDHP under IRS guidelines, the plan must meet specific minimum deductible requirements — $1,700 for self-only coverage and $3,400 for family coverage in 2026. A high-deductible plan is eligible for a health savings account (HSA), which unlocks powerful tax advantages for both employers and employees. Without meeting these thresholds, you cannot pair the plan with an HSA, and you lose one of the hybrid model's most valuable features.

If you're wondering whether you should offer a hybrid HDHP, consider whether your organization fits these three criteria:

- You need to control costs: The primary driver for considering any HDHP is the need to lower fixed monthly premiums. Rising healthcare costs threaten profitability, and your balance sheet demands immediate action.

- You need to consider your employees: Traditional HDHP plans often create resentment because employees face massive deductibles before coverage kicks in.

- You want to offer better benefits: This plan serves a diverse workforce, supporting both cost-conscious and high-utilization employees. Its flexibility is especially valuable in multigenerational workplaces.

Hybrid HDHP vs. Traditional Plans

Understanding how a hybrid HDHP compares to traditional options helps clarify its unique value proposition:

| Feature | Traditional PPO | Traditional HDHP | Hybrid HDHP |

| Monthly Premium | High | Low | Low |

| Deductible | Low | High | Moderate |

| Predictable Copays | Yes | No | Yes, for certain services |

| HSA Compatibility | No | Yes | Yes |

| Best For | Predictability | Low premiums for healthy users | A balance of savings and predictability |

The Core Benefits of a Hybrid Healthcare Plan

This plan design creates value for both sides of the employment relationship. Employers gain financial advantages that extend beyond lower premiums, while employees experience tangible improvements in both their paychecks and their access to care.

For Employers

The financial advantages extend beyond the obvious cost reductions. HDHP premiums are substantially lower than PPO premiums, reducing your monthly fixed costs. For an organization with 100 employees, this difference can translate to tens or even hundreds of thousands of dollars in annual savings.

Lower premiums also mean lower payroll taxes. Because employer contributions to health insurance are subject to FICA taxes, reducing those contributions decreases your payroll tax burden. This secondary savings stream is often overlooked by employers when evaluating plan options. When you calculate the true cost difference between a PPO and a hybrid HDHP, factor in both the direct cost reductions and the indirect payroll tax benefits.

Perhaps most importantly, employee satisfaction and retention improve significantly compared to a traditional HDHP. Employees appreciate the known out-of-pocket costs, which make them feel the plan is genuinely usable. This perception matters, as benefits are a key factor in employee retention, and a plan that feels punitive or inaccessible can drive turnover. The cost of replacing an employee often exceeds their annual salary, making retention improvements financially significant.

For Employees

Fixed copayments protect against unpredictable routine care costs. Rather than paying the full negotiated rate until meeting a $3,000 deductible, employees pay set amounts for visits and prescriptions. Healthcare feels affordable and accessible. The psychological impact of this predictability is valuable — it removes the anxiety that causes many employees to delay or avoid necessary care.

Lower payroll deductions represent another tangible benefit. Because the premium costs are lower, employees often see reduced contributions deducted from their paychecks. Over the course of a year, this adds up to meaningful take-home pay increases. For an employee spending $200 per month on a PPO, a switch to a hybrid HDHP might reduce that payment to $120 — an extra $960 in annual take-home pay.

Finally, employees can contribute to an HSA, which offers powerful tax advantages for both immediate and long-term healthcare expenses. An HSA is a long-term savings vehicle that can grow tax-free and be used for healthcare costs in retirement. The tax advantages make an HSA a powerful financial tool available to employees.

Maximizing Savings With an HDHP-HSA Combination

HSA eligibility is one of the greatest features of a hybrid HDHP. Understanding how an HSA works — and communicating its advantages effectively to employees — is essential for maximizing the value of your hybrid plan.

The "Triple-Tax Advantage" Explained

An HSA offers three distinct tax benefits. Understanding these advantages helps employees see the full value of a hybrid HDHP and encourages maximum utilization.

- The up-front tax break: HSA contributions are pretax, which means every dollar contributed reduces an employee's total taxable income for the year. Immediate savings on income taxes result. It's like getting an instant return on their savings. For an employee in the 24% federal tax bracket, every $1,000 contributed to an HSA saves them $240 in federal income tax alone.

- The growth is tax-free: Unlike a standard savings or brokerage account, where you pay taxes on interest or investment gains, the money in an HSA grows completely tax-free. Over time, the balance compounds faster, creating a larger nest egg for future medical costs. Employees can invest HSA funds in mutual funds, stocks, and other investment vehicles, making it a genuine wealth-building tool.

- The payoff is tax-free: When employees use the money for qualified medical expenses, from copays and prescriptions to dental and vision care, withdrawals are tax-free. This crucial final step makes the savings real. Unlike a 401(k), where you pay taxes when you withdraw money in retirement, HSA withdrawals are never taxed. For 2026, employees can contribute up to $4,400 for self-only coverage and $8,750 for family coverage.

A Real-World Savings Example

The tax advantages of an HSA become more concrete when you see the actual dollar impact. Consider an employee in the 24% federal tax bracket who needs to pay a $1,000 medical expense. Using pretax HSA dollars for a $1,000 expense saves an employee $241 in overpaying with posttax income. This advantage grows over multiple expenses.

Unused HSA funds belong to the employee, carrying over from year to year and growing through interest and investments, all tax-free. When used for qualified medical expenses in the future — even in retirement — withdrawals remain tax-free. As a result, employees benefit from immediate savings on current healthcare and from potential growth in their HSA over time.

A Hybrid HDHP Guide for Employers

Implementing a hybrid HDHP successfully requires thoughtful planning and clear communication. These five steps will help you navigate the process and set your organization up for success:

- Consider employee demographics: Analyze your workforce age, health status, and healthcare utilization patterns. The hybrid approach works well for diverse populations, but understanding your specific demographics helps you tailor the plan design and communication strategy effectively. Review claims data from previous years to identify utilization trends and cost drivers.

- Align the plan with business goals: Define what success looks like. Are you primarily focused on premium reduction, workforce satisfaction, retention, or a combination of factors? Clear goals help you make design decisions and accurately measure outcomes. Establish baseline metrics now so you can track progress after implementation.

- Establish a realistic budget: Determine how much of the cost reductions you'll pass to employees versus retain. Decide on deductible levels, copay amounts, and employer HSA contributions. These decisions shape both your financial outcomes and employee perception of the plan's value. Many employers contribute a portion of the cost savings to employees' HSAs, enhancing the value proposition.

- Educate your employees: Employee understanding directly impacts satisfaction and utilization. Many people still avoid care due to cost, and satisfaction is directly linked to understanding benefits. Invest in clear communication, enrollment support, and ongoing education about how the plan works and how to maximize HSA benefits.

- Partner with an experienced administrator: A knowledgeable benefits administrator can guide plan design, handle regulatory compliance, provide member support, and ensure smooth implementation. The right partner turns complexity into confidence. Look for an administrator with proven experience in hybrid HDHP design and a track record of measurable client savings.

Common Pitfalls to Avoid

Copays that are too high can discourage employees from seeking care, undermining the accessibility you're trying to improve over a traditional HDHP. Setting them too low often means higher premiums. Partner with your benefits administrator and rely on claims data to calibrate these settings appropriately for your workforce.

It's crucial to confirm the plan's compliance with IRS HDHP standards, or Affordable Care Act (ACA) affordability/minimum value rules, as noncompliance can result in penalties or loss of HSA eligibility. Always consult with a qualified advisor or administrator to review your plan documents and eligibility criteria.

Finally, allow enough time for plan design, employee education, enrollment, and administrative setup. Rushing can lead to hurried rollouts, which increase confusion and reduce participation rates. Begin planning several months before open enrollment. Work with an experienced benefits administrator and hold regular check-ins after launch to monitor employee satisfaction and resolve any issues. Ongoing communication is key to long-term success.

Frequently Asked Questions

As you evaluate whether a hybrid HDHP is right for your organization, you likely have questions about how it works in practice. The following answers address the most common concerns employers raise when considering this approach.

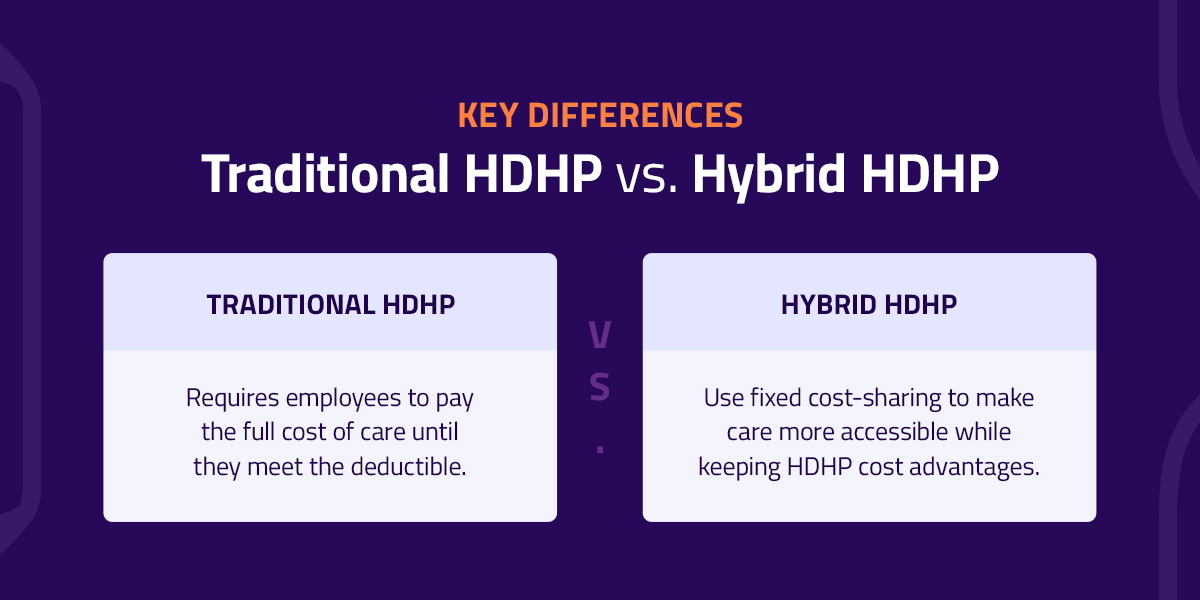

What Are the Key Differences Between a Hybrid HDHP and a Traditional HDHP?

The hybrid model adds fixed copayments back into the HDHP framework. While both plans offer low premiums and HSA compatibility, a traditional HDHP requires employees to pay the full cost of care until they meet the deductible. The hybrid approach provides set cost-sharing amounts for specific services, making care feel more accessible and affordable while still maintaining the cost advantages of an HDHP structure.

Is a Hybrid HDHP Suitable for All Employee Demographics?

This plan design offers flexibility that serves diverse workforces well. Healthy employees who rarely use healthcare appreciate the low premiums and HSA contribution opportunity. For employees requiring frequent care, known out-of-pocket costs make routine visits more affordable.

What Are the First Steps to Implementing a Hybrid HDHP?

Start by analyzing your employee demographics and defining your business goals. Next, establish a realistic budget and determine your cost-sharing strategy. Once the financial framework is clear, focus on employee education — clear communication is essential for adoption and satisfaction. Finally, partner with an experienced benefits administrator who can guide plan design, manage compliance, and provide ongoing member support.

Is an HDHP Better Than a PPO or HMO?

The answer depends on your goals, but the hybrid model often offers a better balance. A traditional PPO plan provides predictability but comes with high premiums. Traditional HDHP plans deliver cost reductions but create access barriers. The hybrid approach combines low premiums with fixed copayments, offering cost control for employers and accessible care for employees. For organizations balancing multiple priorities, this middle path often produces the best outcomes.

What Are the Downsides of a High-Deductible Plan?

The primary downside of a traditional HDHP is high out-of-pocket exposure before coverage begins, which can discourage employees from seeking necessary care. This is precisely the problem the hybrid model solves. By adding known copay amounts for routine services, the hybrid design removes the psychological and financial barriers that make traditional HDHP plans feel punitive, while still delivering the cost reductions employers need.

Get The Difference Card for a Better Hybrid Healthcare Solution

The hybrid HDHP provides cost control and predictable access, solving the challenge of healthcare benefits. Execution is key.

The Difference Card has spent over 20 years helping employers reduce healthcare costs without compromising benefits. Our Medical Expense Reimbursement Plan (MERP) design effectively executes the hybrid HDHP strategy — delivering savings while maintaining the set copayments that employees value.

We partner with you to build a plan that fits your workforce and budget. Our dedicated account managers provide ongoing support, and our U.S.-based customer service team resolves member questions in under 30 seconds on average.

Ready to control costs without alienating employees? Request a proposal and see how we can help.