A Small Business Owner’s Guide to Affordable Health Insurance

Table of Contents

The cost of health insurance can have a significant impact on small businesses. Finding a comfortable balance between keeping costs down and providing the healthcare benefits your employees deserve is essential for employee retention.

Introducing strategic funding is a viable way to pay for healthcare benefits rather than high-priced insurance plans. This guide explains how to find comprehensive healthcare coverage at a lower cost.

Comparing Health Insurance for Small Businesses

Finding an employee health insurance plan that offers everything you require can be tricky. Various factors, such as premium prices and coverage limitations, can make it difficult for you to ensure your employees feel valued in the workplace. To find the best solution, start by comparing your options:

Small Business Group Health Insurance

Employers purchase group health insurance plans to provide coverage for employees and their families. As the employer, you make monthly contributions to the premium, and the employee pays the remaining portion as a payroll deduction.

The benefits of group health insurance include:

- Shareable costs: You can lower costs by sharing premiums with employees, helping you oversee budgets effectively.

- Tax benefits: Monthly employer contributions are tax-deductible, allowing you to offer healthcare coverage at minimal cost.

- Retaining talent: Comprehensive coverage helps you retain and attract employees.

Disadvantages of group health insurance for employers are:

- High admin responsibilities: A group plan requires significant admin across all employees, including managing enrollment, eligibility, and ensuring compliance. For fully insured plans, the carrier handles direct claims processing.

- Increased premiums: The plan's premiums can rise with healthcare costs, leaving little predictability to manage your budgets.

- Limited flexibility: Once your employee's job ends, the group healthcare plan also terminates. Employees may experience a lapse in coverage.

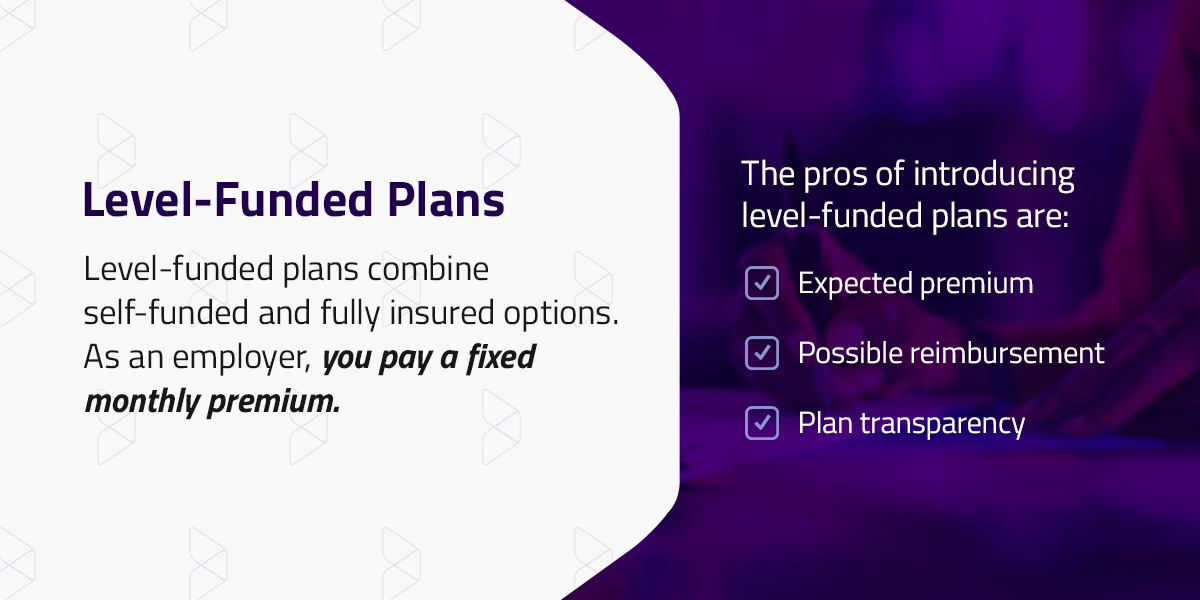

Level-funded plans combine self-funded and fully insured options. As an employer, you pay a fixed monthly premium. The monthly premium includes the necessary admin, estimated claims and stop-loss insurance, covering claims above an individual’s or employee group limit.

The pros of introducing level-funded plans are:

- Expected premium: The monthly premium cost during the plan year is likely to stay the same.

- Possible reimbursement: You may receive surplus refunds if employee claims are lower than anticipated.

- Plan transparency: Access to real-time information allows you to analyze usage and better manage budgets.

Potential downsides to offering level-funded plans include:

- Financial risk: By covering employee claims up to the stop-loss deductible amount, you can pay for employee claims that fail to meet the limit.

- Additional admin: Level-funded plans may require significant administrative effort.

- Renewal increases: Premium prices may increase at renewal, depending on claim activity from previous years.

Individual Coverage Health Reimbursement Arrangement

An individual coverage health reimbursement arrangement (ICHRA) allows you to set a tax-free monthly limit for employee healthcare expenses. Employees can choose plans from any carrier that best suits their needs.

The advantages of an ICHRA are:

- Flexibility: Employees can choose their own plans without being stuck with generic plans that may be unsuitable.

- Predictable costs: Monthly employer premium contributions are likely to remain the same. Setting monthly allowances for employees helps maintain budgets.

- Tax benefits: Reimbursements from an ICHRA are tax-deductible for the employer, and the funds reimbursed to the employee are tax-free.

Possible cons of an ICHRA include:

- Premium tax credit: If the employer’s reimbursement amount is affordable, ICHRA recipients are unable to claim the premium tax credit (PTC).

- Compliance challenges: The ACA's affordability rules and regulations require you to monitor your employer responsibilities.

- Employee decision-making: If employees are accustomed to group plans, they may find it challenging to choose a suitable individual plan.

Qualified Small Employer Health Reimbursement Arrangement

A qualified small employer HRA (QSEHRA) is similar to an ICHRA, but is available only to smaller businesses with 50 or fewer employees.

The benefits of a QSEHRA include:

- Tax advantages: Employers can deduct reimbursements from taxable income, and employees receive them tax-free.

- Employee flexibility: The employee can choose a plan that meets their healthcare needs.

- Seting contribution limits: Employers may contribute up to the IRS limits. The limit for self-coverage in 2026 is $6,450.

Potential disadvantages of a QSEHRA are:

- Reimbursement limitations: The IRS sets annual limits on employer reimbursements.

- PTC impact: Like with an ICHRA, employees with a QSEHRA can't claim a PTC if the employer's reimbursement is affordable.

What Is a MERP?

A medical expense reimbursement plan (MERP) is an IRS-approved and employer-sponsored health plan. Instead of paying for an employee's medical expenses up front, employees pay for their own qualified medical expenses first. Employees then submit claims through their employer or a third-party administrator.

Employees must submit proof of their medical expenses to reclaim the funds, and reimbursement is usually sent via their paycheck. A MERP product is available with a high-deductible group health plan (HDHP), which enables reimbursement for high-deductible expenses.

6 Benefits of MERP Products

A MERP product is particularly beneficial for small businesses and offers advantages for your employees. Introducing a MERP allows you to cover a range of expenses, including prescriptions, doctor’s appointments, and hospital visits:

1. Significant Savings

A maximum annual limit for employees helps you better manage healthcare budgets. Instead of paying a fixed monthly premium, such as with a traditional group plan, you pay for each medical expense incurred by your employee. Claims can reach the preset amount you set.

If an employee’s claims are lower than the preset amount, you retain the unspent funds.

2. Tax Benefits for Employers and Employees

According to the IRS, reimbursements made to employees for qualified medical costs are a business expense. The classification limits your liability for corporate tax, as you can deduct expenses from your company's taxable income. Reimbursements are also tax-free for employees. The deduction from taxable income allows you to avoid paying payroll taxes on Medicare and Social Security.

3. Flexibility and Customization Options

As the employer, you're responsible for deciding which medical expenses qualify for reimbursement, including dental care and hospital visits. By following IRC Section 213(d) guidance, you can tailor a MERP package based on the needs of your workforce.

4. Less Admin for Employers

For fully insured group health plans, the insurance carrier typically handles direct claims management. However, when an employer might otherwise manage direct reimbursement, or for self-funded plans, a MERP product allows a third party to take on this responsibility, freeing up time for other employer responsibilities. A designated administrator approves or declines expense claims and maintains compliance.

5. HDHP Compatibility

Offering an HDHP alongside a MERP product is advantageous for both employers and employees. As the employer, you benefit from lower HDHP premiums and offer employees a large portion of high deductible to cover out-of-pocket expenses.

Additionally, employees can open a health savings account (HSA) after enrolling in a qualifying HDHP. To maintain HSA eligibility, the MERP must be specifically designed to be HSA-compatible, such as limited-purpose or post-deductible. If an HSA doesn't cover certain expenses, an employee can use their MERP.

6. Attract New Employees

By offering a MERP product as your company's health benefit, you'll likely attract new talent to join your business. The flexibility of a MERP enables more practical health benefits for employees and provides key support for out-of-pocket expenses.

Especially beneficial for small businesses struggling to recruit suitable talent, a MERP can be a distinct advantage over competitors with restricted health plans.

MERP vs. Group Health Insurance for Small Businesses

Choosing among health insurance plans and benefits can be hard. Here are some top considerations when comparing group health insurance and a MERP:

- Business costs: Group health insurance plans can involve higher or less predictable premium costs for employers. A MERP product may offer more predictable costs for your business without compromising its benefits.

- Claim methods: Traditional plans require employees to submit claims through the carrier. For fully insured plans, the carrier handles direct claims processing, which can be a relatively straightforward process for employees. A MERP involves a third-party administrator who oversees employee claims. Employees pay for expenses up front and then submit claims for reimbursement.

- Deductible differences: Employees with a group health plan may have to pay the deductible amount. MERP recipients can claim the entire amount of a qualifying medical expense from employers, including a deductible up to a preset allowance made by the employer. Employees will have to pay the medical costs up front before submitting a reimbursement claim.

- Employer control: A group health insurance plan comes with preset conditions and limits determined by the carrier. With a MERP, you can set your reimbursement limits to align with your business costs and employee needs.

- Cash flow management: A monthly premium fee applies to group health insurance plans and is set by the carrier. The monthly commitment to employee premium payments may disrupt your cash flow. A MERP allows you to pay after an expense is submitted and approved.

- Renewal processes: Premiums may rise if a large quantity of high-value claims have been submitted. Increasing costs are a challenge for your business and the employees' premium contribution. By offering a MERP product, your business's claims experience doesn't factor into a carrier's premium costs, as you set your own reimbursement limits. However, if the MERP is paired with an underlying HDHP, the premiums for that HDHP can still be influenced by overall claims experience.

- Contribution limits: A MERP product offers more flexibility with employer contribution limits than traditional group health plans. You can choose contribution and reimbursement limits. Group health insurance imposes contribution percentages and specific enrollment criteria.

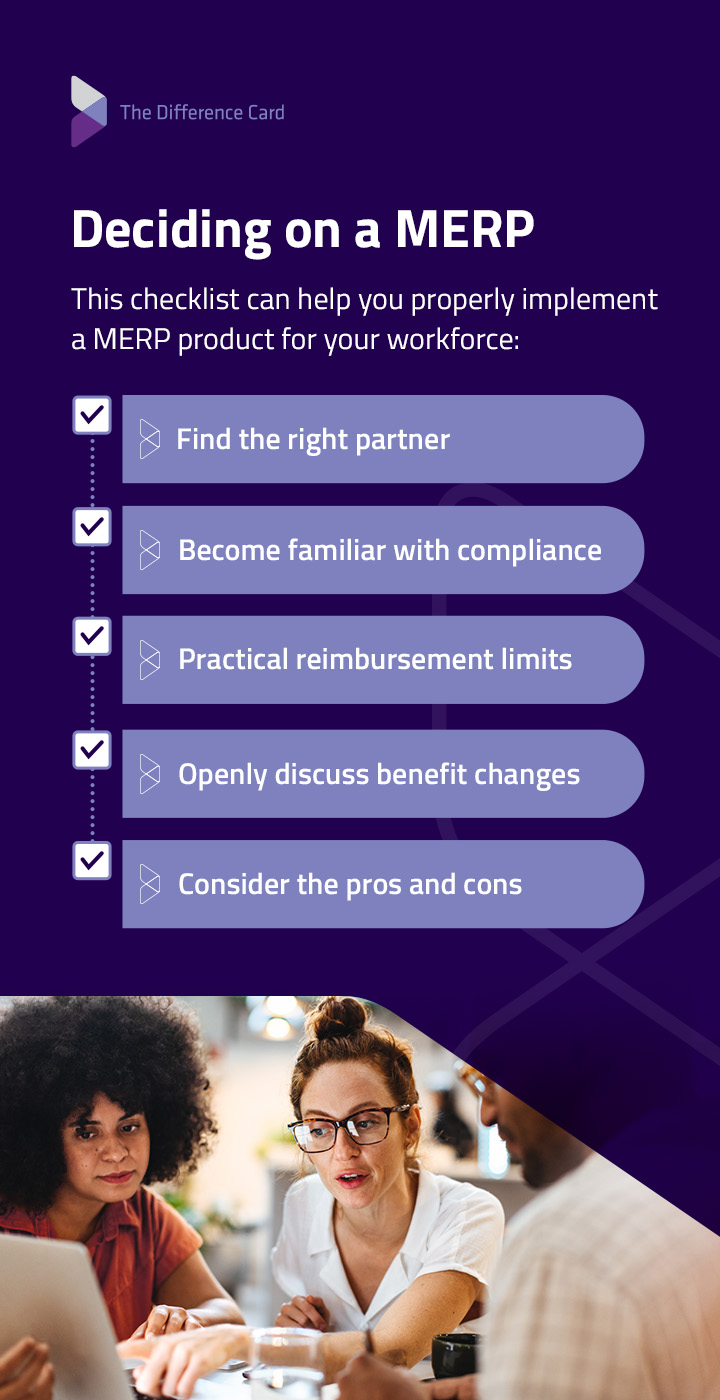

Deciding on a MERP

A MERP gives your employees access to more beneficial healthcare services while reducing out-of-pocket expenses. This checklist can help you properly implement a MERP product for your workforce:

- Find the right partner: A trustworthy partner is essential to managing all employee claims. Research MERP product partners with relevant experience and reputation. Partners with in-depth MERP knowledge can simplify set up and oversee the admin.

- Become familiar with compliance: Qualified MERP partners can navigate the relevant compliance standards. However, it's worth learning the regulations from the ACA and IRS to become confident with your decision and answer potential employee questions.

- Practical reimbursement limits: Think carefully about the reimbursement limits your business can afford and are worthwhile for employees. Pinpointing eligible medical expenses is another consideration.

- Openly discuss benefit changes: Whether you're new to offering a health benefit or transitioning from a group health plan, talk with employees about the advantages and changes. Open communication allows employees with uncertainty to feel comfortable.

- Consider the pros and cons: Although a MERP product is a financially beneficial option for your business, it's essential to look at the pros and cons compared to other plans and benefits.

MERP and Small Business Health Insurance FAQs

Learn more about the MERP product and your business's suitability with these answers to frequently asked questions:

Is a MERP Available for a Business With Fewer Than 50 Employees?

Yes. A MERP is an ideal health benefit for small businesses that want to provide coverage while keeping costs down.

Does a MERP Cover an Employee's Family Members?

A MERP can cover family members, dependents, and spouses. As an employer, you decide whether to offer a MERP benefit that covers the employee and family members.

What Happens if My Employees Have a High Claims Year?

If your employee accumulates high-value claims that exceed your preset annual limit, the employee is responsible for the remaining cost. The employee can make a claim for additional expenses through another health insurance plan.

Are Unused MERP Funds Reimbursed to Employees?

No. Employees don't receive reimbursement for unused MERP funds. The unused funds remain within the business.

Can a MERP Cover All Medical Expenses?

No. Qualifiable expenses under IRS Section 213(d) include specific exclusions, such as cosmetic procedures.

Get Your Custom MERP Proposal Today

At The Difference Card, our experienced and knowledgeable team helps you deliver a customizable MERP product to your employees for flexible and comprehensive healthcare. Our solution offers personalized support from a dedicated account manager, and you'll have access to plans via an easy-to-use mobile app.

With approximately $1 billion in healthcare savings since 2001, The Difference Card is a trustworthy partner that can make a significant difference in your business. Request your MERP proposal and start offering a cost-effective healthcare benefit.