ICHRA vs. QSEHRA: What’s the Difference?

Table of Contents

A health reimbursement arrangement (HRA) helps employers provide employees with healthcare benefits without compromising their bottom line. While there are different HRA types, an individual coverage HRA (ICHRA) and a qualified small employer HRA (QSEHRA) are good additions or alternatives to a traditional group health plan, and can help control a company’s healthcare costs.

Both benefits offer companies tax advantages and give employees the freedom to choose their coverage. However, eligibility rules apply for successful claims. To help you offer the right benefit for your clients, this article highlights the main differences between a QSEHRA and an ICHRA.

What Is an ICHRA?

An ICHRA is a reimbursement arrangement where employers reimburse employees and eligible family members for qualified medical expenses, such as healthcare premiums, copayments, and deductibles. Employees and their families must submit documentation to claim reimbursements. These reimbursements are tax-free, and limits vary depending on the employee’s family size. Employers determine the specific rules and employee eligibility.

However, employees and eligible family members must each have minimum essential coverage (MEC), which they can get from a public or private marketplace. They can use ICHRA and pretax payroll deductions to pay for the premiums. Without an MEC, employees can’t claim reimbursements. They must also report if their coverage was terminated retroactively.

Who Is an ICHRA Best For?

An ICHRA is best for companies looking to offer competitive healthcare benefits. It lets employees choose eligible coverage that fits their needs, making it more likely that they will use it. This can be better than offering a traditional health plan that benefits some, but not all members. Unlike a QSEHRA, an ICHRA doesn’t cap company sizes, making it ideal for large businesses.

What Is a QSEHRA?

A QSEHRA is an arrangement that lets employers reimburse specific healthcare expenses, such as premiums and out-of-pocket expenses, to certain employees. However, it is only available to small businesses due to the company size requirement. Employees need an MEC to be eligible. Employers decide how much they’ll contribute up to a maximum amount annually set by the IRS.

Employees must provide proof when submitting a claim. Employers typically pay these claims monthly. Some employers may roll over unused funds from year to year. Employers own the accounts, so the funds remain with the employer even if the employee leaves the company.

An employer may refer to a QSEHRA by a different name, which they may indicate in a letter outlining the terms. Employers provide this letter to employees to inform them of their benefits.

Who Is a QSEHRA Best For?

A QSEHRA is best for small employers looking to save on group health plans. These employers may also be working with part-time or seasonal employees. However, unlike an ICHRA, employees can’t opt out of a QSEHRA if their employer offers it (though workers can choose not to use the funds). Employees can choose their healthcare coverage depending on their needs.

ICHRA vs. QSEHRA: Key Differences

Understanding the requirements and processes will help you suggest a better option. As a high-level overview, the main differences between an ICHRA and a QSEHRA include:

| ICHRA | QSEHRA | |

|---|---|---|

| Companies Eligible | Employers of all sizes | Small employers with fewer than 50 employees |

| Employees Eligible | Defined by the employer according to employee classes set by the ICHRA rules | All employees in the small company, except for potential exclusions |

| Required Insurance Coverage | MEC | MEC |

| Contribution Limits | Set by the employer | Based on the maximum limits annually set by the Internal Revenue Service (IRS), or up to $6,350 for 2025 |

| Effect on Premium Tax Credits | Affordable plans disqualify employees from premium tax credits | Can make employees eligible for some or no tax credits |

| Best For | Large companies looking to offer competitive health benefits for different employee types | Small companies on a budget for healthcare costs |

The differences between an ICHRA and a QSEHRA specifically lie in the requirements:

Company Eligibility and Requirements for an ICHRA

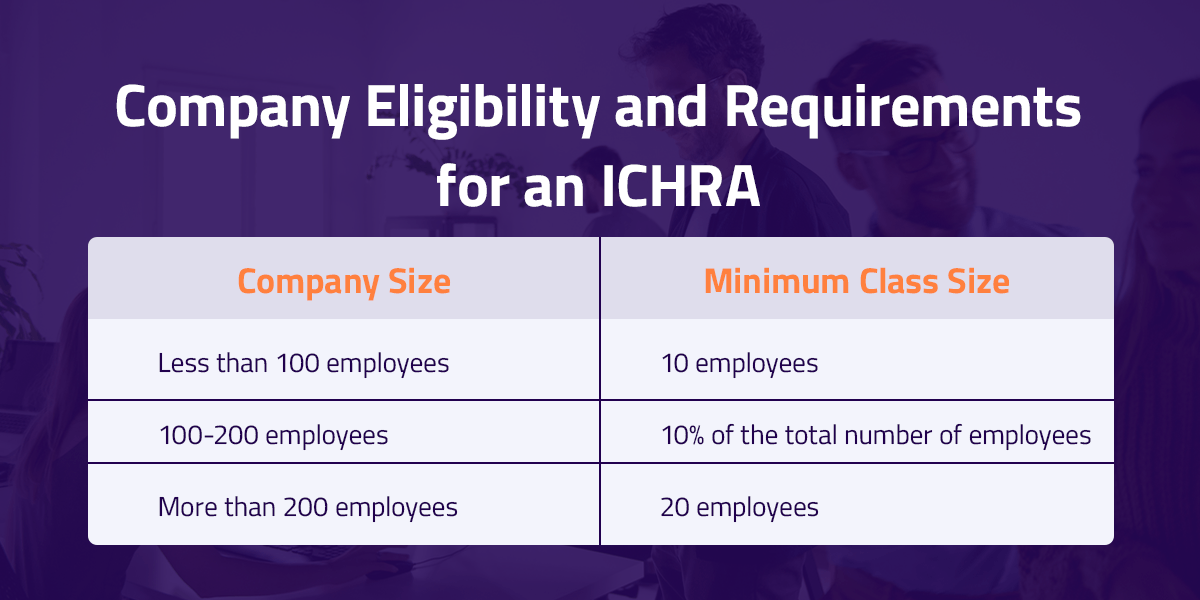

Employers of all sizes can offer an ICHRA, provided they have at least one employee who is not self-employed or is the spouse of a self-employed individual. Only employees can have an HRA. Employers can also set up the benefits anytime. However, they may want to choose a start date that works with their employees’ insurance coverage.

An ICHRA that starts on January 1 lets employees choose coverage during the Marketplace’s annual open enrollment period. State marketplaces may have their own deadlines. Midyear start dates may qualify employees for a special enrollment, which can be the case for new employees. Generally, employees need to select a plan that takes effect on the day their ICHRA starts.

Employers offering an ICHRA can still offer a traditional group health plan, provided it’s offered for a different employee class. The same employee type can’t choose between either. For instance, employers may provide a traditional group health plan to full-time employees and an ICHRA to part-time employees. Employers must adhere to the size requirements to offer both:

| Company Size | Minimum Class Size |

|---|---|

| Less than 100 employees | 10 employees |

| 100-200 employees | 10% of the total number of employees |

| More than 200 employees | 20 employees |

Employers must provide a letter indicating the ICHRA terms. New employees may receive theirs as soon as they’re eligible — no later than the first day of the ICHRA’s start date. Current employees should receive the letter 90 days before the start of each plan year. Employees can decline the ICHRA when offered. The letter indicates the coverage terms, including:

- Whether the benefit extends to family members.

- How much the employer will reimburse.

- The plan’s start and end dates.

Company Eligibility and Requirements for a QSEHRA

Small employers with fewer than 50 full-time employees, including the equivalent of full-time employees, can set up a QSEHRA anytime. Employers with 50 or more full-time employees are considered an applicable large employer (ALE). However, employers who grew their team to at least 50 in a calendar year may not necessarily be considered an ALE until the next year.

QSEHRA must be offered on the same terms to all eligible employees — amounts can vary by age and family size, as permitted by IRS rules. Employers cannot offer a group health plan, including an HRA, to any employee if they offer a QSEHRA. Endorsing a particular policy or insurer can constitute a group health plan.

The QSEHRA does not treat former employees, such as retirees, as employees. This means employers can provide a group health plan to former employees without sacrificing the employer’s eligibility. Similar to an ICHRA, employers must provide a written notice to employees.

New employees must receive theirs as soon as they’re eligible, while current employees should get the letter 90 days before each plan year starts. Employers can consider open enrollment dates when offering QSEHRA, but employees may also qualify for special enrollment periods.

Employee Eligibility and Requirements for an ICHRA

Employees must enroll in an individual health insurance plan with MEC to use an ICHRA. Short-term plans and limited benefits coverage don’t count. If employees already have MEC, they won’t need a new one. When selecting coverage, employees can choose from:

- A Marketplace plan.

- Medicare Part A and B or Part C.

- Plan from a private insurance company.

Employers can offer an ICHRA to specific employee types. The types are determined through job-based criteria, such as:

- Full-time employees.

- Part-time employees.

- Seasonal employees.

- Salaried employees.

- Nonsalaried employees.

- Employee work locations.

- Employees covered by a collective bargaining agreement.

- Nonresidents without U.S. income sources.

ICHRA rules specify the employee types — employers cannot make up their own. Employers must provide the same terms per employee type, but they can set waiting periods for new employees. Employees need to confirm their coverage when filing a claim, and employers should explain the specific steps for reimbursement.

Employee Eligibility and Requirements for a QSEHRA

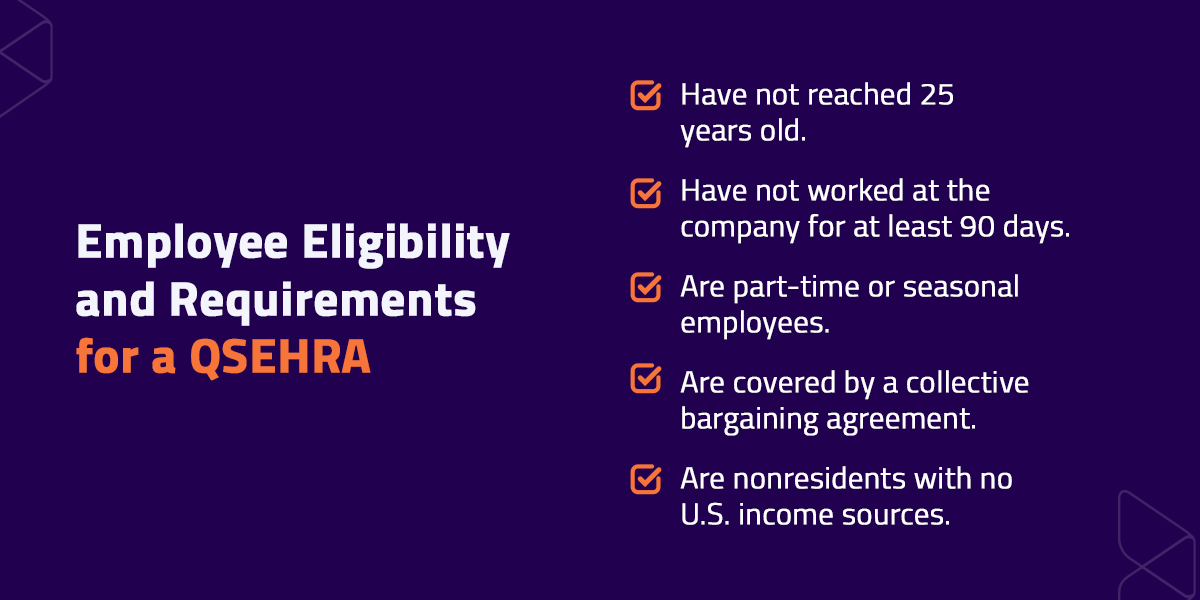

To be eligible for a QSEHRA, employees and family members must also have an MEC. Similar to an ICHRA, they must confirm their coverage when making a claim. Although eligible employees can’t opt out of a QSEHRA, employers can exclude employees who:

- Have not reached 25 years old.

- Have not worked at the company for at least 90 days.

- Are part-time or seasonal employees.

- Are covered by a collective bargaining agreement.

- Are nonresidents with no U.S. income sources.

Part-time employees can include those with less than 35 hours of work per week or those with significantly fewer hours compared to other employees. Seasonal employees can be those working in a company for less than nine months, or those with annual employment of less than seven months.

Employees can get coverage from or outside the Marketplace, or update their existing plan during enrollment periods.

ICHRA and QSEHRA Contribution Limits

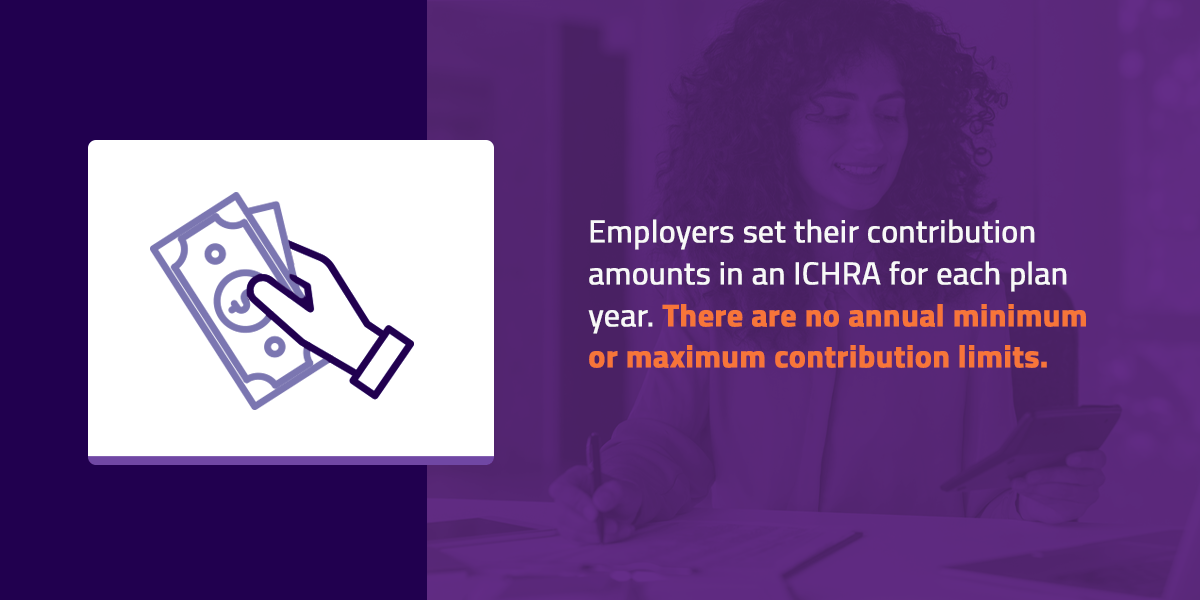

Employers set their contribution amounts in an ICHRA for each plan year. There are no annual minimum or maximum contribution limits. However, reimbursement amounts for each employee class may vary depending on the employee’s number of dependents or age. Reimbursement amounts for age differences should not exceed a 3:1 ratio.

Employers can set reimbursement amounts for QSEHRA up to the annual limit per employee set by the IRS. For 2025, employers can reimburse up to $6,350 per individual or $12,800 for family coverage.

How an ICHRA Impacts Premium Tax Credits

Premium tax credits help employees and their families pay for insurance premiums from the Marketplace. An ICHRA can impact these credits, making it essential that employees understand how they work. If employers offer an affordable ICHRA, employees can’t take advantage of the premium tax credits. This affordability depends on:

- Employer contributions.

- Employee’s household income.

- Premium cost of the self-only, lowest Silver Marketplace plan.

As of 2025, if the monthly cost of the self-only, lowest Silver Marketplace plan is less than 9.96% of 1/12 of the employee’s annual household income, then the ICHRA can be considered affordable. The employee and their eligible family members would be ineligible for the premium tax credits even if they don’t use the ICHRA funds or decline the ICHRA. If an employer offers an ICHRA not considered affordable, employees can choose between the ICHRA and the premium tax credit.

The Marketplace determines the ICHRA’s affordability. When employees apply for coverage, they must provide the ICHRA information, including the employer’s contribution amount and start date. Healthcare.gov also provides an HRA affordability tool employees can use before applying.

How a QSEHRA Impacts Premium Tax Credits

Similar to an ICHRA, a QSEHRA affects the eligibility of employees and their dependents for premium tax credits. They can be eligible for some or no tax credits. The Marketplace won’t know about the QSEHRA — the IRS determines the employee’s final eligibility. This depends on how much QSEHRA contributions the employer offers, regardless of whether the employee used them.

Since employees won’t know right off the bat how many credits they’re eligible for, they need to be careful in using them. If they use more credits than they are eligible for, they must repay the excess when filing their taxes.

ICHRA vs. QSEHRA: Benefits and Drawbacks

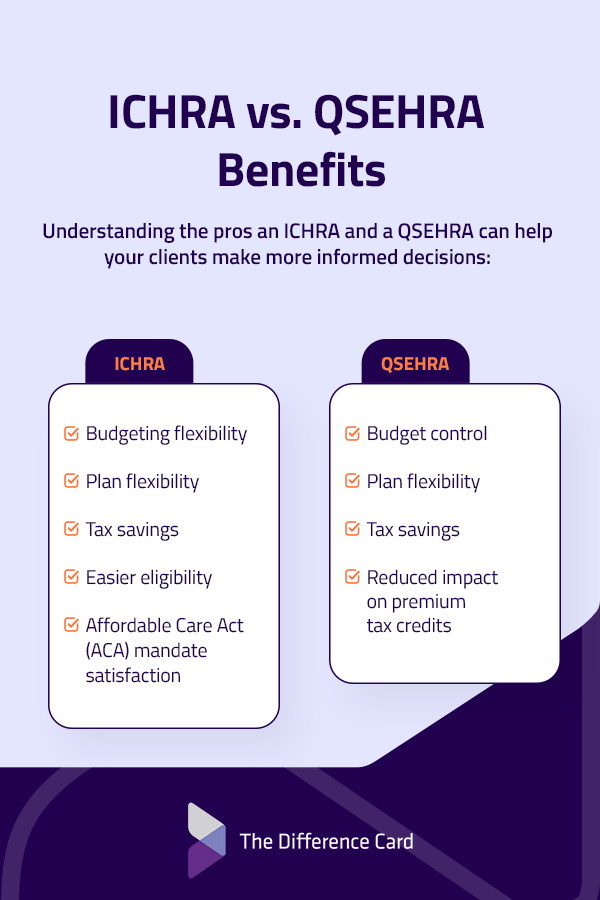

Understanding the pros and cons of an ICHRA and a QSEHRA can help your clients make more informed decisions:

ICHRA Benefits

Because of the ICHRA’s requirements, offering this benefit leads to:

- Budgeting flexibility: Companies offering an ICHRA have the freedom to allocate funds according to their budget and employees’ needs. They won’t be limited to caps, benefiting large businesses with hundreds of employees. Companies with multiple employee classes can also offer an ICHRA to save on traditional group health plans. This provides a competitive edge for companies, especially when hiring part-time or seasonal employees.

- Plan flexibility: Employees can select an MEC according to their preferred terms and healthcare needs. This flexibility can encourage them to take proactive steps in caring for their health, which also benefits the company long-term.

- Tax savings: ICHRA reimbursements are tax-deductible and free of payroll taxes. Employees won’t need to pay income tax on the reimbursements.

- Easier eligibility: ICHRA doesn’t come with participation requirements, unlike a traditional group health plan. It also doesn’t come with maximum company size limits, unlike QSEHRA. The employer’s eligibility won’t impact whether or not employees use the benefit.

- Affordable Care Act (ACA) mandate satisfaction: ICHRA can satisfy the ACA requirement that mandates an ALE to offer affordable coverage to 95% of the full-time employees and their dependents, depending on the employer’s contribution.

ICHRA Drawbacks

While ICHRA comes with multiple benefits, employers should also consider these drawbacks:

- Eligibility rules for qualified healthcare expenses: Employers must explain the reimbursement rules to employees clearly, while employees must keep their proof and confirm their coverage for every claim. This can be challenging to navigate at the beginning for companies transitioning from a traditional group health plan.

- Individual health insurance requirement: Employees and their family members must have an MEC to participate.

- Premium tax credit impact: An affordable ICHRA sacrifices an employee’s premium tax credit. The employee also cannot opt to use the credits even if they decline the ICHRA offer.

QSEHRA Benefits

A QSEHRA offers similar benefits to an ICHRA, but it’s only applicable for certain employers. Companies can consider these advantages:

- Budget control: Smaller companies can control their healthcare spending better with a QSEHRA due to the maximum contribution limits. They can also choose to reimburse healthcare premiums only or include out-of-pocket costs. Because employers can roll over unused QSEHRA funds to the next year, they can save and allocate more budget for other expenses.

- Plan flexibility: Similar to an ICHRA, a QSEHRA lets employees choose an eligible healthcare coverage they prefer.

- Tax savings: QSEHRA reimbursements are tax-free. Employers generally won’t include the payments in their gross income, provided the employee has MEC.

- Reduced impact on premium tax credits: Unlike an ICHRA, employees with a QSEHRA may still enjoy some premium tax credits. This lets them reduce the premiums they pay upfront for Marketplace coverage.

QSEHRA Drawbacks

Despite a QSEHRA’s benefits, your clients should consider the following disadvantages:

- Company size limits: QSEHRA is for small employers only. If your client’s business grows to 50 or more employees, they will become ineligible for this benefit.

- Maximum contribution caps: Depending on the number of employees and eligible dependents, as well as their healthcare needs, the contribution cap may be limited for certain companies.

- Mandatory requirement: Employees can’t say no to a QSEHRA when their employer offers the benefit.

- Uncertain premium tax credits: Unlike ICHRA, where the Marketplace determines an employee’s eligibility, employees won’t know from the IRS right away how much tax credits they’re eligible for. If employees max out the use of their tax credits regularly, and the IRS determines that they’ve used more than what they’re eligible for, employees must pay back the credits they’ve used.

How Clients Can Make the Right Choice

When pitching the benefits to your clients, you can help them make the right choice for their company. Their ideal option may depend on whether:

- They’re a startup with less than 10 employees: Startups or small businesses with less than 50 employees can offer a QSEHRA to their employees. The benefit provides similar advantages to an ICHRA while providing more budgeting control.

- They’re a business with less than 50 employees: A business with less than 50 employees can still technically offer a QSEHRA. However, they may need to prepare for an ICHRA or other benefits once they become an ALE.

- They’re a corporation with different employee types: A large company with different employee types or classes can diversify its overall offerings by providing an ICHRA for certain employees.

Frequently Asked Questions About ICHRA and QSEHRA

Your clients may also ask some common questions. Consider the following for their inquiries:

- Does ICHRA count as income? Reimbursements will not be considered taxable income for employees, provided they maintain their MEC and only reimburse qualified medical expenses.

- What is the 90-day rule for QSEHRA? There are two 90-day rules that apply to QSEHRA. When providing a QSEHRA for employees, employers must provide a written notice detailing the terms at least 90 days before the start of each plan year. However, companies can also exclude employees who have not been employed by the company for at least 90 days from this benefit.

- Can I administer my own QSEHRA? Employers can administer their own QSEHRA. However, this can be trickier to manage compared to working with an HRA administrator, like The Difference Card. It can also be time-consuming, considering small business owners already have a lot on their plates. Noncompliance with IRS rules also renders the HRA invalid, making all reimbursements taxable for both employers and employees.

Optimize Your Employee Benefits With The Difference Card

Large and small businesses operate in a competitive market. This makes it essential to optimize healthcare benefits for potential employees. By providing unique insights and solutions, you can help clients gain an advantage and satisfy their budgeting and employees’ needs.

Eligibility rules, contribution limits, and impact on premium tax credits are the main differences between ICHRA and QSEHRA. Whatever you plan to offer your clients, The Difference Card can help them by providing seamless benefits administration.

We help clients save over 18% on health insurance costs. With over 20 years of experience and $1.8 billion of savings delivered, you can trust that your clients can get the reliable services they need. We’ll work closely with you to deliver the exceptional service that makes your agency stand out from the brokerage marketplace. If you’re ready to get started, request a proposal today.