MERP vs. Traditional Health Insurance

Table of Contents

- What Is a MERP?

- What Is Traditional Health Insurance?

- Core Differences Between MERPs and Traditional Plans

- Key Considerations When Choosing Which Type of Plan to Offer

- Risk, Compliance, and Legality of MERPS vs. Traditional Plans

- Hybrid Strategies to Combine MERP and Traditional Insurance

- Decision Matrix: Which Model Best Fits Your Company?

- Frequently Asked Questions About MERPs

- See the Difference a Smarter Health Plan Can Make With The Difference Card

Healthcare costs continue to climb. These price jumps put pressure on you, as an employer, to make difficult decisions about your benefits strategy. The traditional approach has been straightforward, with group health insurance with fixed premiums and standardized coverage being the norm. As costs rise, more organizations are exploring cost-saving strategies such as high-deductible health plans, self-funded arrangements, and medical expense reimbursement plans (MERP). A MERP offers a different approach to funding healthcare benefits than traditional insurance.

This guide breaks down the core differences between MERP and traditional health insurance, explores the key factors that influence your decision, and helps you determine which model best serves your organization's goals.

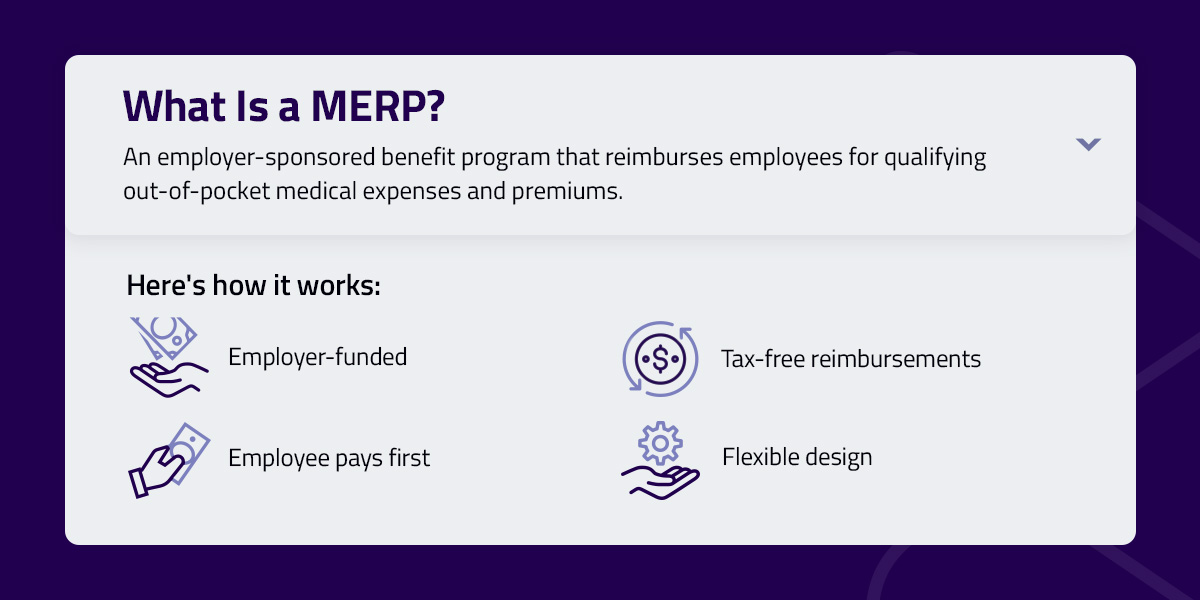

What Is a MERP?

A MERP is an employer-sponsored benefit program that reimburses employees for qualifying out-of-pocket medical expenses and premiums. Unlike traditional health insurance, a MERP doesn't provide insurance coverage. Instead, it functions as a tax-advantaged reimbursement benefit that works alongside health insurance plans.

Here's how it works:

- Employer-funded: The employer sets aside a defined amount for employee healthcare reimbursements.

- Employee pays first: Employees pay for eligible medical expenses out of pocket, then submit claims for reimbursement.

- Tax-free reimbursements: Qualified reimbursements are tax-free for both employers and employees.

- Flexible design: Employers control what expenses qualify, set reimbursement limits, and customize the plan to their budget.

Employers using a MERP pay only for submitted claims, rather than a fixed monthly premium regardless of usage. Organizations can see significant savings potential when claims run lower than projected.

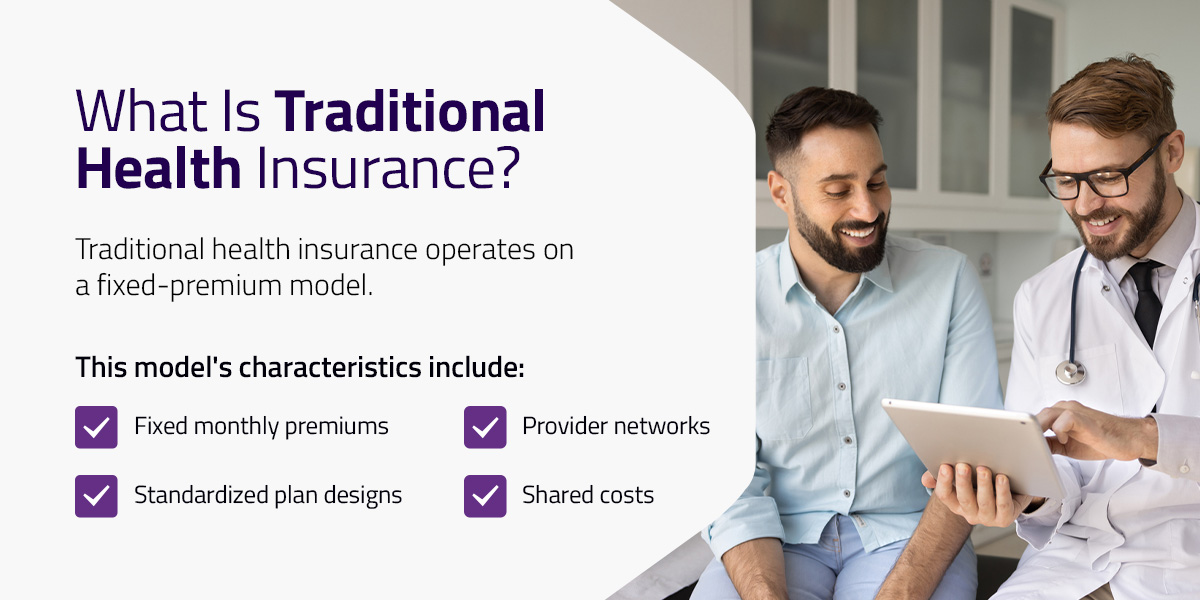

What Is Traditional Health Insurance?

Traditional health insurance operates on a fixed-premium model. Employers purchase a standardized health policy from an insurance carrier and pay a set monthly premium for each covered employee, regardless of whether the employee uses their benefits.

This model's characteristics include:

- Fixed monthly premiums: Employers pay the same amount each month.

- Standardized plan designs: Coverage typically follows preferred provider organization (PPO), health maintenance organization (HMO), or exclusive provider organization (EPO) structures with limited customization.

- Provider networks: Employees must use in-network providers to maximize benefits and minimize out-of-pocket costs.

- Shared costs: Employees typically pay deductibles, copayments, and coinsurance when they receive care.

Traditional plans transfer the financial risk from employers to insurance carriers. The carrier is responsible for all covered claims for which premium payments are due.

Core Differences Between MERPs and Traditional Plans

Understanding the differences between these two models helps you compare and decide which approach suits your organization's priorities. The table below highlights key criteria across MERP and traditional health insurance.

| Feature | MERP | Traditional Health Insurance |

|---|---|---|

| Who funds it? | Employer only | Employer and employees share costs |

| Who owns the money? | Employer retains unused funds | The insurance carrier keeps the premium payments |

| Monthly premiums? | No fixed premiums. Employer sets reimbursement budget | Fixed monthly premiums paid to the carrier |

| Tax treatment | Reimbursements are tax-deductible for employers, tax-free for employees (IRS Section 105) | Employer contributions are tax-deductible, and employee premium payments may be pre-tax |

| Flexibility | Employer customizes eligible expenses, reimbursement caps, and plan design | Standardized plan options with limited customization |

| Cost predictability | Variable. Costs fluctuate with actual claims submitted | Fixed premiums, but subject to annual renewal increases of 5%-15% |

| Network restrictions? | Employees choose individual policies, selecting their own networks | Employer-selected carrier network applies to all employees |

| Eligible expenses | Employer defines qualifying expenses (copays, deductibles, premiums, out-of-pocket costs) | Coverage defined by carrier policy (medical, preventive, emergency services) |

| Rollover rules | Employer determines rollover policy. Unused funds may revert to the employer or roll over to the next plan year | Premiums do not roll over |

| Compliance requirements | Must comply with IRS Section 105, ERISA, ACA, and nondiscrimination rules | Must comply with ACA, ERISA, HIPAA, and state insurance regulations |

| Implementation time | 4-8 weeks for plan design, employee education, and administrative setup | 6-12 weeks for carrier selection, enrollment, and implementation |

| Best use cases | Organizations seeking cost control, customization, and flexibility. Works well paired with HDHP or individual market policies | Organizations prioritizing simplicity, predictable budgeting, and comprehensive carrier-managed benefits |

This comparison highlights the MERP vs. traditional health insurance decision as a choice between flexibility and predictability. The right choice depends on your organization's size, risk tolerance, budget constraints, and workforce needs.

Key Considerations When Choosing Which Type of Plan to Offer

Both employers and employees experience these two models differently. Key factors influence which approach delivers better outcomes for your organization.

Cost Structure and Potential Savings

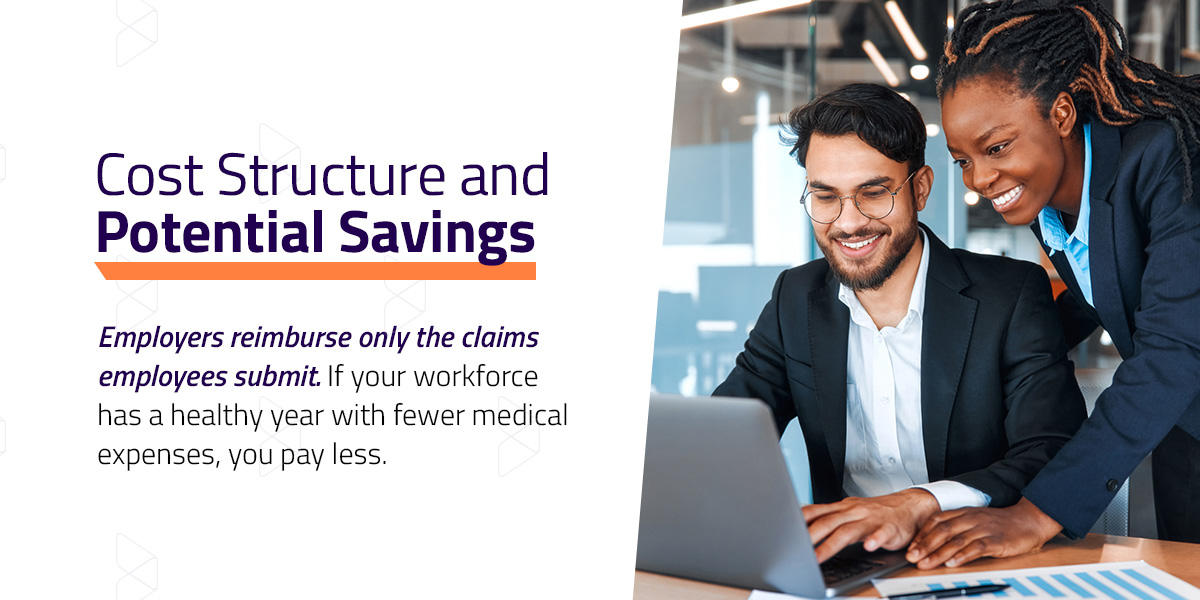

What differs most between these models is how costs are incurred and controlled. Traditional health insurance operates on a fixed-cost model. Fixed premiums offer budget certainty but eliminate the possibility of savings in low-claims years.

A MERP operates on a pay-for-what's-used model. Employers reimburse only the claims employees submit. If your workforce has a healthy year with fewer medical expenses, you pay less. Such a structure can reduce healthcare costs for employers whose actual claims run below their budgeted amounts.

Organizations that implement strategic MERP solutions often achieve substantial savings compared to traditional premium structures. Our employer case studies document how employers across various industries have leveraged this model to control costs while maintaining quality coverage.

Savings potential varies depending on your workforce demographics, historical claims patterns, and plan design. Younger, healthier employees typically file fewer claims, maximizing MERP savings. Organizations with older or higher-risk employees may see smaller differentials between MERP costs and traditional premiums.

Plan Flexibility and Customization

Traditional health insurance offers limited customization. Carriers offer a selection of standardized plan designs, and employers choose from them. While you can choose between different deductible levels or network configurations, the plan's structure remains fixed. Every employee receives the same coverage, regardless of their individual needs or preferences.

A MERP delivers greater flexibility. Employers decide which expenses qualify for reimbursement, set individual or family reimbursement limits, and adjust these parameters annually based on budget and workforce feedback. This customization allows organizations to design benefits to match their financial capacity and employee demographics.

Examples of MERP customization options:

- Set different reimbursement levels for different employee tiers.

- Choose whether to cover premiums, deductibles, copays, or all three.

- Adjust annual maximums based on budget availability.

- Add or remove covered services as priorities shift.

This flexibility makes MERP valuable if you're seeking alternatives to traditional health insurance that can evolve with your organization rather than locking you into rigid structures.

Administrative Burden for HR Teams

Managing traditional health insurance is typically simple for HR teams. Most administrative work is handled by the insurance carrier, leaving HR to focus on enrollment and premium payments. In contrast, MERP administration can seem more complex because employers oversee reimbursements and compliance.

However, this burden is minimized by using a qualified third-party administrator (TPA), who manages claims, compliance, payments, and employee communication on the employer’s behalf. Insurance brokers can help employers select a TPA that streamlines the process and ensures the plan remains fully compliant.

Employee Experience and Benefits

How your employees experience these two models affects satisfaction, retention, and the success of the benefits program. Traditional plans offer familiarity. Most employees understand how insurance works, know what to expect from their coverage, and appreciate the simplicity of having insurance cards and established networks. However, high deductibles and out-of-pocket costs can create financial stress, especially when unexpected medical expenses arise.

A well-designed MERP can improve the employee experience by reducing out-of-pocket costs and increasing flexibility. With MERP funds covering deductibles, copayments, or premium contributions, employees face smaller financial barriers to accessing care. That can lead to better health outcomes and higher satisfaction with their benefits package.

Studies support this connection between flexible benefits and employee satisfaction. Results show that 85% of organizations report improved employee satisfaction from their benefits programs, with nearly 75% noting a positive impact on recruiting and retention.

Over eight in 10 employers agree that financial wellness resources, including flexible benefits like MERP, can help drive satisfaction, retention, and productivity. This suggests that the employee experience extends beyond simple coverage to include financial accessibility and choice.

Risk, Compliance, and Legality of MERPS vs. Traditional Plans

Understanding how each model allocates risk and ensures compliance allows you to make an informed decision. Traditional plans provide budgetary predictability through fixed monthly premiums. However, this protection comes at a cost. In favorable claims years, employers don't benefit from the savings. At renewal time, carriers often impose significant premium increases reflecting industry trends or the group's claims history.

MERP plans operate differently. Because they're self-insured reimbursement arrangements rather than insurance products, the employer retains the financial risk of medical claims. However, employers also gain substantial cost control by setting fixed maximum reimbursement amounts. Setting caps on total financial exposure enables the organization to benefit when actual claims run below budget.

Key compliance considerations include:

- Legal framework: MERP must comply with the Employee Retirement Income Security Act (ERISA), the Health Insurance Portability and Accountability Act (HIPAA), and IRS regulations.

- Plan documentation: Requires formal written plan documents specifying terms, eligibility, and covered expenses.

- Nondiscrimination testing: Must not favor highly compensated employees over others.

- Tax compliance: Must follow IRS Section 105 requirements for tax-free reimbursements.

Insurance brokers evaluating options for their clients should assess risk tolerance alongside potential savings. Organizations comfortable with managed risk and variable costs often find MERP attractive. Those prioritizing absolute budget certainty may prefer traditional insurance despite higher average costs.

How MERPs Comply With IRS Section 105

MERP plans operate under Section 105 of the Internal Revenue Code, which establishes the legal framework for employer-provided health reimbursement arrangements. This long-established IRS provision lets employers reimburse employees for medical expenses on a tax-free basis when the plan meets specific requirements.

The tax advantages are substantial. Employer contributions to a compliant MERP are tax-deductible business expenses. Employee reimbursements for qualified medical expenses are excluded from gross income, meaning employees receive benefits without paying income or payroll taxes on those amounts. Both parties gain value compared to additional taxable compensation.

The IRS Revenue Ruling 03-102 provides authoritative direction on how these plans must be structured and administered. The ruling clarifies that reimbursements must be for actual medical expenses incurred by the employee, spouse, or dependents, and the plan must be established and maintained by the employer.

Compliance isn't optional. Plans that fail to meet Section 105 requirements lose their tax-advantaged status, potentially creating unexpected tax liabilities for both employers and employees. This regulatory framework is why partnering with compliance specialists is essential for organizations implementing MERP solutions.

How to Ensure MERP Compliance

While MERP offers great advantages, compliance pitfalls can undermine those benefits if not properly managed. The most common issues involve inadequate plan documentation, discriminatory plan designs, and improper reimbursement of non-qualified expenses.

Critical compliance requirements include:

- Maintaining formal, written plan documents that specify all terms and conditions.

- Conducting annual nondiscrimination testing to ensure equitable treatment.

- Reimbursing only IRS-qualified medical expenses as defined in Section 213(d).

- Providing required disclosures and notices to participants.

- Coordinating MERP with other health coverage to avoid conflicts.

These requirements create administrative complexity that few employers want to manage internally. Expert administrators ensure that plan documents meet regulatory standards, conduct required testing, process only qualified reimbursements, and maintain compliance as regulations evolve. Comprehensive compliance services make the difference.

For employers considering MERP, partnering with an experienced TPA effectively addresses compliance concerns while preserving the model's financial advantages. Insurance brokers can add value by connecting clients with qualified administrators rather than dismissing MERP due to perceived complexity.

Hybrid Strategies to Combine MERP and Traditional Insurance

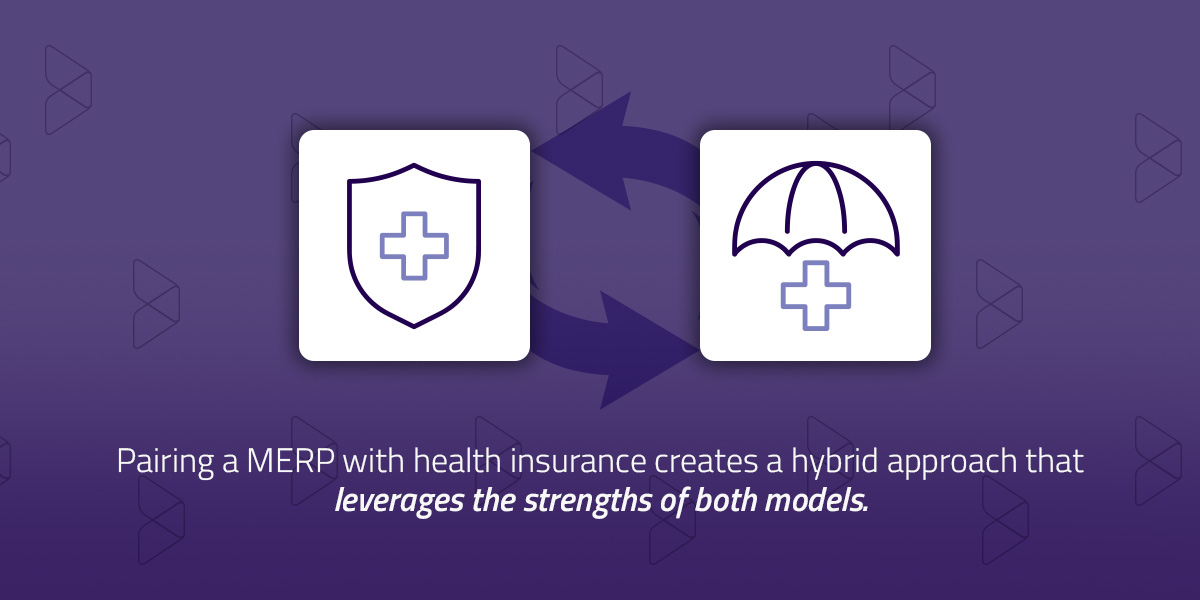

One common misconception is that employers must choose exclusively between MERP and traditional insurance. In reality, these models often work best when combined strategically. MERP programs can function as "wrap-around" benefits that enhance traditional coverage rather than replacing it.

Pairing a MERP with health insurance creates a hybrid approach that leverages the strengths of both models. The insurance plan provides the core coverage and protection employees need, while the MERP addresses gaps, reduces out-of-pocket costs, and offers customization that standard insurance cannot.

Hybrid strategies work well if you want to offer high-deductible health plans to control premium costs but worry about placing too much financial burden on employees. The MERP bridges that gap by reimbursing employees for expenses the insurance plan doesn't fully cover.

Pairing a MERP With a High-Deductible Health Plan (HDHP)

Pairing these options represents one of the most powerful and common hybrid strategies. Employers select a high-deductible health plan, which carries lower monthly premiums than traditional low-deductible options. The premium savings create budget flexibility that the employer redirects into a MERP.

MERP funds then reimburse employees for some or all of their deductible expenses. From the employees' perspective, they receive financial protection by having their deductible covered, while the employer benefits from lower fixed premium costs. Combining HDHPs with MERP support delivers both cost efficiency for employers and financial accessibility for employees.

The math often works favorably. The premium difference between a high-deductible plan and a low-deductible plan can exceed the claims employees submit in a given year. In those cases, employers save money while employees receive equal or better effective coverage.

Offering HDHPs with MERP support also gives employers more control over annual cost increases. Traditional low-deductible plans typically see larger percentage increases at renewal. High-deductible plans often experience more moderate increases, and employers retain the flexibility to adjust MERP reimbursement levels annually to match budget realities.

Using a MERP for Supplemental or Excluded Benefits

Another effective hybrid strategy uses MERP to cover benefits that traditional health insurance excludes or covers inadequately. Many standard health plans provide limited coverage for dental care, vision services, or specialty treatments. Employees value these benefits, but adding separate insurance policies for each creates administrative complexity and additional fixed costs.

MERP funding can efficiently fill these gaps. Employers define which supplemental expenses qualify for reimbursement, set annual maximums for each category, and provide employees with a more comprehensive benefits package without having to purchase multiple insurance policies.

A MERP and a health savings account (HSA) can work together or serve distinct purposes within an overall benefits strategy. Unlike an HSA, which requires pairing with an HDHP and has strict contribution limits, a MERP offers more design flexibility and can supplement any type of health coverage.

Decision Matrix: Which Model Best Fits Your Company?

Choosing between MERP and traditional health insurance requires assessing your organization's specific circumstances, priorities, and risk tolerance. This decision framework can help you and insurance brokers evaluate which approach best aligns with your business.

Consider a traditional health insurance plan if:

- Budget predictability is the highest priority, even if it means higher average costs.

- Your organization prefers to transfer all medical claims risk to a carrier.

- Limited internal resources are available for benefits administration.

- The workforce strongly prefers familiar insurance card programs.

- You want the insurance carrier to handle all claims, networks, and customer service.

Consider a MERP if:

- Cost efficiency and potential savings are higher priorities than fixed budgets.

- Managed risk and variable costs are acceptable.

- Customizing benefits to the workforce and the budget is a priority.

- There is a willingness to partner with a TPA for administration and compliance.

- The goal is to reduce costs without cutting employee benefits.

Consider a hybrid approach if you:

- Want to balance cost control with employee protection.

- Are offering an HDHP but want to shield employees from the full deductible.

- Want to provide supplemental benefits beyond standard insurance coverage.

- Value both the stability of insurance and the flexibility of reimbursement arrangements.

No single answer fits every organization. The right choice depends on your specific situation, and that choice may evolve as your organization grows or your priorities shift.

Frequently Asked Questions About MERPs

Explore the following questions and answers about providing MERPs to employees.

1. Is There a Minimum or Maximum Number of Employees for a MERP?

Yes, MERP availability can depend on minimum and maximum employee counts, with specific thresholds varying based on the type of MERP or HRA structure used. One common threshold is 50 employees, which triggers different regulatory requirements under the Affordable Care Act. Organizations considering MERP should consult with benefits advisors or TPAs to understand which options are available for their group size.

2. What Happens to Unused MERP Funds at the End of the Year?

Unused MERP funds are typically subject to a "use it or lose it" rule, meaning money that employees don't claim by the plan year deadline is forfeited. However, plan design varies. Some employers allow grace periods or limited carryovers. The specific terms depend on how the employer structures the plan document. This differs from an HSA, where unused funds roll over indefinitely and remain the employee's property.

3. Can Employees Be Taxed on MERP Reimbursements?

No, employees aren't taxed on MERP reimbursements if the plan complies with IRS Section 105 requirements. Qualified medical expense reimbursements are excluded from gross income and are not subject to income or payroll taxes. However, if the plan fails to meet compliance requirements or reimburses non-qualified expenses, those amounts could become taxable. Working with experienced compliance administrators prevents these issues.

4. Can a MERP Replace Traditional Health Insurance Entirely?

A MERP can replace traditional group insurance if you structure it to comply with the Affordable Care Act (ACA) requirements. Many organizations pair a MERP with individual market policies that provide ACA-compliant coverage, reimbursing employees for their premiums and out-of-pocket costs. This approach allows you to exit the group insurance market while ensuring employees maintain comprehensive coverage.

See the Difference a Smarter Health Plan Can Make With The Difference Card

The choice between MERP and traditional health insurance goes beyond premiums and deductibles. It's about building a benefits strategy that aligns with your organization's priorities, whether that's cost predictability, workforce flexibility, or both.

Both models have distinct advantages depending on your needs. If you're exploring a MERP solution, partnering with an experienced provider is essential. The Difference Card has helped organizations design and administer compliant MERP solutions since 2001, delivering an average of 18% in annual healthcare cost savings through custom strategies backed by The Difference Guarantee.

Ready to see what a designed health plan can do for your organization? Request a proposal for a custom savings analysis tailored to your workforce and budget. If you ever feel uncertain about the right path, our experts are here to guide you.